Impact Assessment of US/Israel-Iran Conflict

Impact Assessment of US/Israel-Iran Conflict

- Iran and Oman reported progress on a temporary shipping route through the Strait of Hormuz, although this would not mean a full reopening of the Strait.

- Vessel traffic remains low as key details are still under discussion. Meanwhile, Houthi forces claimed an attack on a Saudi tanker near Yanbu and threatened further attacks in the Red Sea and Gulf of Aden, keeping shipping risks high.

- OPEC+ is set to increase production by around 188,000 b/d, while geopolitical tensions around Hormuz and the Red Sea continue to drive crude supply and trade flows.

- The US crude inventories rose by 2.5 mln bbl to 407 mln bbl for the week ending 31st July, against expectations of a decline, adding some downward pressure on crude prices. Meanwhile, SPR stocks fell by 2.8 mln bbl to 304.8 mln bbl, keeping emergency reserves at low levels. Refinery activity remained strong at 96.5%, although crude processing declined slightly to 17.2 MBpd.

- The US crude imports increased to 6.2 MBpd, while exports reached 3.7 MBpd. At the same time, gasoline and distillate stocks declined, indicating relatively tighter fuel inventories.

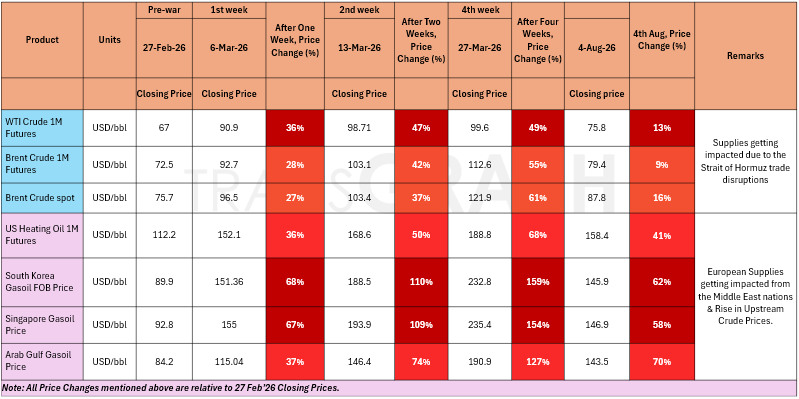

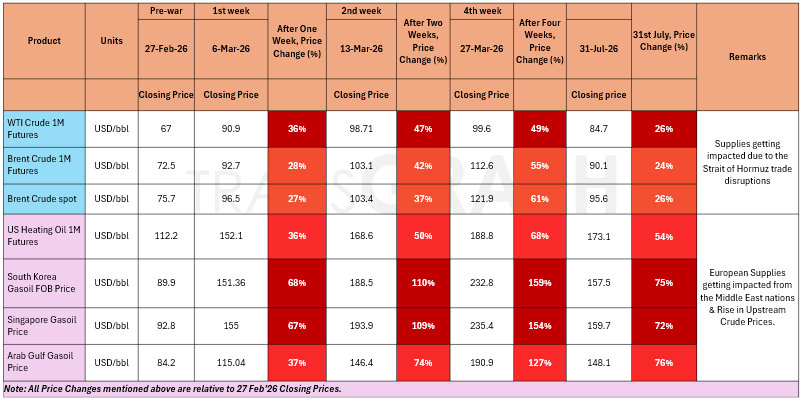

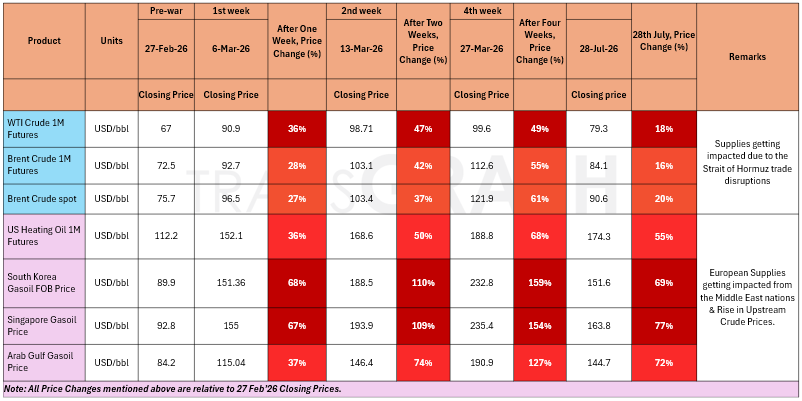

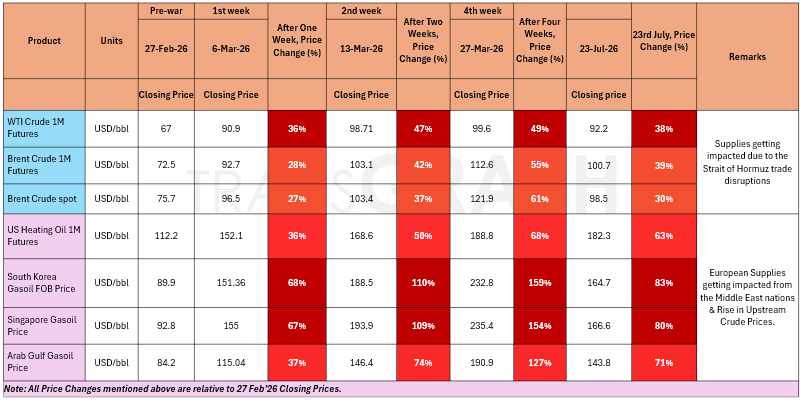

War Impact on Crude Oil & Gasoil/Diesel Prices

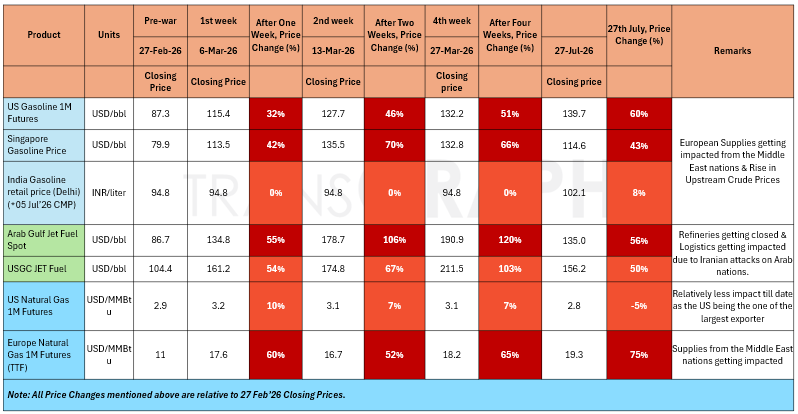

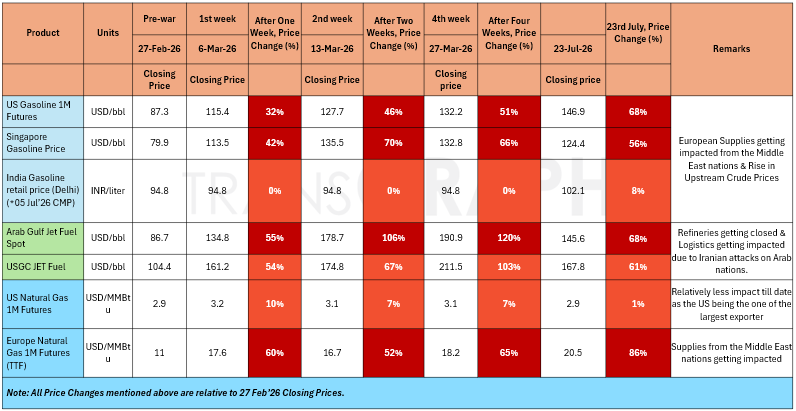

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

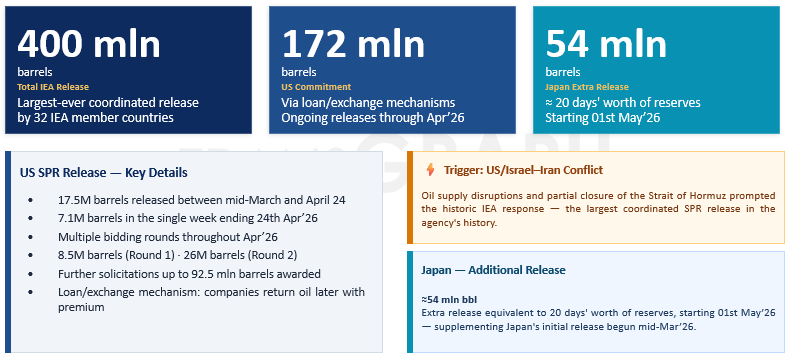

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

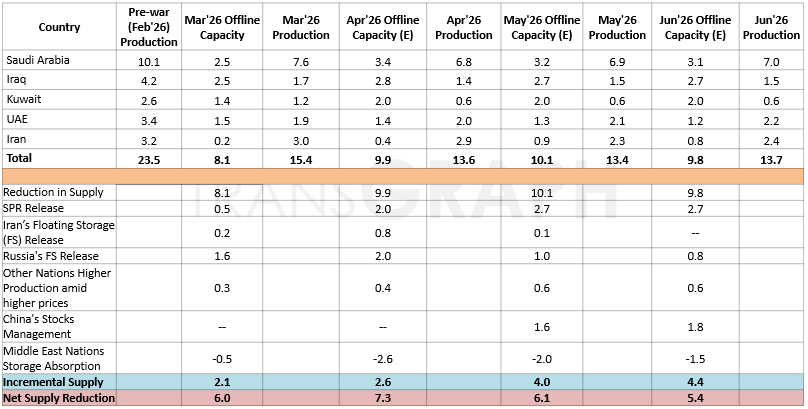

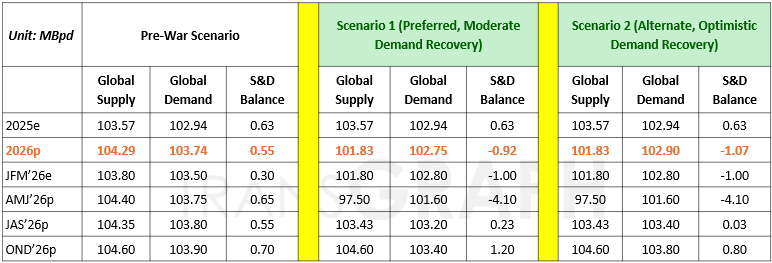

War Scenarios Point to Global Supply Deficit of 0.92–1.07 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 4.10 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks continue to progress positively, with tanker flows through the Strait of Hormuz gradually normalizing over the next 4–5 weeks. Supply recovers steadily, while demand improves at a slower pace and remains below pre-war expectations, resulting in a moderate market surplus.

- Scenario 2 (Alternate): The Strait of Hormuz normalizes over the next 4–5 weeks, supporting a gradual recovery in oil exports and supply. Demand rebounds more strongly than in Scenario 1, reducing the market surplus, although overall consumption remains below pre-war levels.

Geopolitical backdrop:

US President Donald Trump says ongoing negotiations are Iran's "last chance" for a deal to end the conflict, after he called off a planned major military strike. Meanwhile, Tehran publicly denies direct talks with Washington, stating it is only discussing a temporary safe shipping route through the Strait of Hormuz with Oman.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 7.1%.

Base metals:

- Copper prices are up 3.9% on a weekly basis, as Fed holds interest rates pressuring dollar, market remains in backwardation structure, and inflation pressures ease with softer CPI and weaker job data despite persistent geopolitical conflicts. Prices receive continued support from CME-LME arbitrage, high China copper premium, exchange inventory outflows, and persistent mine supply constraints which offset pressure from renewed tensions, hawkish Fed outlook, and elevated global inventories.

- Aluminum prices are up 0.7% on a weekly basis due to renewed tensions.

Precious metals:

- Stronger U.S. yields and weak industrial offtake, especially auto are suppressing any upside momentum.

- Stronger US Dollar due to anticipation of rate hike in US is weighing on precious metal prices.

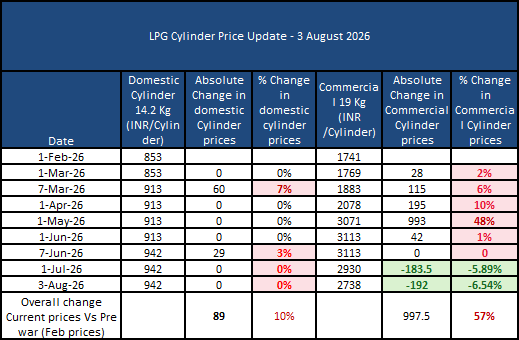

LPG Market Update

- For August 2026, Saudi Aramco Contract Prices (CPs) rebounded to USD 620/ton for propane and USD 640/ton for butane, compared with USD 580/ton and USD 600/ton, respectively, in July. This represents a 6.9% month-on-month increase in propane CPs and a 6.7% month-on-month increase in butane CPs.

- Sonatrach raised its August propane OSP by 4.2% m-o-m, from $518/ton to $540/ton, while the butane OSP was cut by 5.0%, from $600/ton to $570/ton.

- India’s commercial LPG prices eased further in August, with the 19 kg cylinder price in New Delhi declining by ₹192, from ₹2,930 in July to ₹2,738 as of 3 August 2026. Despite the recent correction, commercial LPG remains substantially above its pre-war level of ₹1,741/cylinder. In contrast, the 14.2 kg domestic LPG cylinder remained unchanged at ₹942, reflecting continued price stability for household consumers.

Impact Assessment of US/Israel-Iran Conflict

- Qatar officials stated that mediators were making progress toward ending the conflict, which weighed on oil prices by improving expectations of stable oil supplies. However, Iran rejected US President Donald Trump's claim that negotiations were underway.

- Venezuela's oil exports declined slightly to 1.16 MBpd in Jul'26 from 1.20 MBpd in Jun'26, reflecting lower inventory draw downs, although shipments to the US surged to 0.77 MBpd, the highest level since early 2019.

- Meanwhile, exports to India fell to 0.18 MBpd (from 0.28 MBpd) and to Europe declined to 0.08 MBpd (from 0.10 MBpd), while imports of 0.08 MBpd of heavy naphtha supported crude blending operations.

- The US crude oil exports fell to 3.66 MBpd in Jul'26, the lowest level in eight months, down from a record 5.7 MBpd in May'26, as a temporary US-Iran peace agreement increased Middle Eastern oil supplies and reduced demand for US crude.

- Exports to Asia declined to 40% of total shipments (from 52% in Jun'26), while shipments are expected to recover to 4.58 MBpd in Aug'26 and 4.45 MBpd in Sep'26.

- Two Saudi oil tankers carrying a combined 3 mln bbl of crude successfully transited the Bab el-Mandeb Strait despite vessel traffic dropping to 18 ships on 02nd Aug'26 from 28 on 31st Jul'26, following the Houthis' maritime embargo on Saudi Arabia.

- Meanwhile, commodity vessel transits through the Strait of Hormuz fell to 10 on 01st Aug'26 from 19 on 31st Jul'26 amid reports of tanker attacks, underscoring heightened risks to a route that normally handles about 20% of global crude oil and LNG trade.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

War Scenarios Point to Global Supply Deficit of 0.92–1.07 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 4.10 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks continue to progress positively, with tanker flows through the Strait of Hormuz gradually normalizing over the next 4–5 weeks. Supply recovers steadily, while demand improves at a slower pace and remains below pre-war expectations, resulting in a moderate market surplus.

- Scenario 2 (Alternate): The Strait of Hormuz normalizes over the next 4–5 weeks, supporting a gradual recovery in oil exports and supply. Demand rebounds more strongly than in Scenario 1, reducing the market surplus, although overall consumption remains below pre-war levels.

Geopolitical backdrop:

US President Donald Trump says ongoing negotiations are Iran's "last chance" for a deal to end the conflict, after he called off a planned major military strike. Meanwhile, Tehran publicly denies direct talks with Washington, stating it is only discussing a temporary safe shipping route through the Strait of Hormuz with Oman.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 7.1%.

Base metals:

- Copper prices are up 1% on a weekly basis, as Fed holds interest rates, China copper premium rises to 13 month high, and inflation pressures ease with softer CPI and weaker job data despite persistent geopolitical conflicts. Prices receive continued support from CME-LME arbitrage, backwardation structure, exchange inventory outflows, and persistent mine supply constraints which offset pressure from renewed tensions, hawkish Fed outlook, and elevated global inventories.

- Aluminum prices are up 2.1% on a weekly basis due to renewed tensions.

Precious metals:

- Stronger U.S. yields and weak industrial offtake, especially auto are suppressing any upside momentum.

- Stronger US Dollar due to anticipation of rate hike in US is weighing on precious metal prices.

LPG Market Update

- For August 2026, Saudi Aramco Contract Prices (CPs) rebounded to USD 620/ton for propane and USD 640/ton for butane, compared with USD 580/ton and USD 600/ton, respectively, in July. This represents a 6.9% month-on-month increase in propane CPs and a 6.7% month-on-month increase in butane CPs.

- Sonatrach raised its August propane OSP by 4.2% m-o-m, from $518/ton to $540/ton, while the butane OSP was cut by 5.0%, from $600/ton to $570/ton.

- India’s commercial LPG prices eased further in August, with the 19 kg cylinder price in New Delhi declining by ₹192, from ₹2,930 in July to ₹2,738 as of 3 August 2026. Despite the recent correction, commercial LPG remains substantially above its pre-war level of ₹1,741/cylinder. In contrast, the 14.2 kg domestic LPG cylinder remained unchanged at ₹942, reflecting continued price stability for household consumers.

Impact Assessment of US/Israel-Iran Conflict

- Venezuela's oil exports declined slightly to 1.16 MBpd in Jul'26 from 1.20 MBpd in Jun'26, reflecting lower inventory drawdowns, although shipments to the US surged to 0.77 MBpd, the highest level since early 2019.

- Meanwhile, exports to India fell to 0.18 MBpd (from 0.28 MBpd) and to Europe declined to 0.08 MBpd (from 0.10 MBpd), while imports of 0.08 MBpd of heavy naphtha supported crude blending operations.

- The US crude oil exports fell to 3.66 MBpd in Jul'26, the lowest level in eight months, down from a record 5.7 MBpd in May'26, as a temporary US-Iran peace agreement increased Middle Eastern oil supplies and reduced demand for US crude.

- Exports to Asia declined to 40% of total shipments (from 52% in Jun'26), while shipments are expected to recover to 4.58 MBpd in Aug'26 and 4.45 MBpd in Sep'26.

- Two Saudi oil tankers carrying a combined 3 mln bbl of crude successfully transited the Bab el-Mandeb Strait despite vessel traffic dropping to 18 ships on 02nd Aug'26 from 28 on 31st Jul'26, following the Houthis' maritime embargo on Saudi Arabia.

- Meanwhile, commodity vessel transits through the Strait of Hormuz fell to 10 on 01st Aug'26 from 19 on 31st Jul'26 amid reports of tanker attacks, underscoring heightened risks to a route that normally handles about 20% of global crude oil and LNG trade.

- OPEC+ group agreed to increase crude production by 0.19 MBpd in Sep'26, completing the rollback of its 1.65 MBpd voluntary supply cuts, although the move has limited near-term impact as exports remain constrained by disruptions around the Strait of Hormuz and Bab el-Mandeb.

- South Korea plans to begin importing 0.88 mln bbl of crude oil from Argentina, marking its first regular purchases from the country as part of efforts to diversify energy supplies away from the Middle East and deepen bilateral cooperation in energy and critical minerals.

- ADNOC announced that, effective 1st Nov'26, it will price the official selling prices (OSPs) of all its crude grades, including Murban, Das, Umm Lulu, and Upper Zakum, against prompt-month Platts Dubai instead of Murban crude futures, aiming to enhance pricing transparency and better align OSPs with cargo loading periods following recent market disruptions.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

War Scenarios Point to Global Supply Deficit of 0.92–1.07 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 4.10 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks continue to progress positively, with tanker flows through the Strait of Hormuz gradually normalizing over the next 4–5 weeks. Supply recovers steadily, while demand improves at a slower pace and remains below pre-war expectations, resulting in a moderate market surplus.

- Scenario 2 (Alternate): The Strait of Hormuz normalizes over the next 4–5 weeks, supporting a gradual recovery in oil exports and supply. Demand rebounds more strongly than in Scenario 1, reducing the market surplus, although overall consumption remains below pre-war levels.

Geopolitical backdrop:

US President Donald Trump says ongoing negotiations are Iran's "last chance" for a deal to end the conflict, after he called off a planned major military strike. Meanwhile, Tehran publicly denies direct talks with Washington, stating it is only discussing a temporary safe shipping route through the Strait of Hormuz with Oman.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 7.1%.

Base metals:

- Copper prices are up 1% on a weekly basis, as Fed holds interest rates, China copper premium rises to 13 month high, and inflation pressures ease with softer CPI and weaker job data despite persistent geopolitical conflicts. Prices receive continued support from CME-LME arbitrage, backwardation structure, exchange inventory outflows, and persistent mine supply constraints which offset pressure from renewed tensions, hawkish Fed outlook, and elevated global inventories.

- Aluminum prices are up 2.1% on a weekly basis due to renewed tensions.

Precious metals:

- Stronger U.S. yields and weak industrial offtake, especially auto are suppressing any upside momentum.

- Stronger US Dollar due to anticipation of rate hike in US is weighing on precious metal prices.

LPG Market Update

- For August 2026, Saudi Aramco Contract Prices (CPs) rebounded to USD 620/ton for propane and USD 640/ton for butane, compared with USD 580/ton and USD 600/ton, respectively, in July. This represents a 6.9% month-on-month increase in propane CPs and a 6.7% month-on-month increase in butane CPs.

- Sonatrach raised its August propane OSP by 4.2% m-o-m, from $518/ton to $540/ton, while the butane OSP was cut by 5.0%, from $600/ton to $570/ton.

- India’s commercial LPG prices eased further in August, with the 19 kg cylinder price in New Delhi declining by ₹192, from ₹2,930 in July to ₹2,738 as of 3 August 2026. Despite the recent correction, commercial LPG remains substantially above its pre-war level of ₹1,741/cylinder. In contrast, the 14.2 kg domestic LPG cylinder remained unchanged at ₹942, reflecting continued price stability for household consumers.

Impact Assessment of US/Israel-Iran Conflict

- Two Saudi oil tankers carrying a combined 3 mln bbl of crude successfully transited the Bab el-Mandeb Strait despite vessel traffic dropping to 18 ships on 02nd Aug'26 from 28 on 31st Jul'26, following the Houthis' maritime embargo on Saudi Arabia.

- Meanwhile, commodity vessel transits through the Strait of Hormuz fell to 10 on 01st Aug'26 from 19 on 31st Jul'26 amid reports of tanker attacks, underscoring heightened risks to a route that normally handles about 20% of global crude oil and LNG trade.

- OPEC+ group agreed to increase crude production by 0.19 MBpd in Sep'26, completing the rollback of its 1.65 MBpd voluntary supply cuts, although the move has limited near-term impact as exports remain constrained by disruptions around the Strait of Hormuz and Bab el-Mandeb.

- South Korea plans to begin importing 0.88 mln bbl of crude oil from Argentina, marking its first regular purchases from the country as part of efforts to diversify energy supplies away from the Middle East and deepen bilateral cooperation in energy and critical minerals.

- ADNOC announced that, effective 1st Nov'26, it will price the official selling prices (OSPs) of all its crude grades, including Murban, Das, Umm Lulu, and Upper Zakum, against prompt-month Platts Dubai instead of Murban crude futures, aiming to enhance pricing transparency and better align OSPs with cargo loading periods following recent market disruptions.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

War Scenarios Point to Global Supply Deficit of 0.92–1.07 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 4.10 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks continue to progress positively, with tanker flows through the Strait of Hormuz gradually normalizing over the next 4–5 weeks. Supply recovers steadily, while demand improves at a slower pace and remains below pre-war expectations, resulting in a moderate market surplus.

- Scenario 2 (Alternate): The Strait of Hormuz normalizes over the next 4–5 weeks, supporting a gradual recovery in oil exports and supply. Demand rebounds more strongly than in Scenario 1, reducing the market surplus, although overall consumption remains below pre-war levels.

Geopolitical backdrop:

US-Saudi forces carried out coordinated airstrikes on Iran-aligned PMF positions in Iraq in response to alleged IRGC-directed drone attacks, while the US intercepted Iranian ballistic missiles targeting its base in Jordan, ending a five-day lull in hostilities and signaling renewed escalation. Meanwhile, Iran rejected Oman's proposal for joint management of the Strait of Hormuz, demanding greater control over shipping routes and warning the strait could remain closed if its terms are not met, raising concerns over global energy security. Despite President Trump's renewed push for peace talks, Iran remains skeptical. Markets are likely to stay cautious as the fragile situation leaves the risk of further military escalation and renewed volatility in oil and financial markets.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 7.3%.

Base metals:

- Copper prices are up 0.4% on a weekly basis, as Fed holds interest rates, China copper premium rises to 13 month high, and inflation pressures ease with softer CPI and weaker job data despite persistent geopolitical conflicts. Prices receive continued support from CME-LME arbitrage, backwardation structure, exchange inventory outflows, and persistent mine supply constraints which offset pressure from renewed tensions, hawkish Fed outlook, and elevated global inventories.

- Aluminum prices are up 1.2% on a weekly basis due to renewed tensions and Fed outcome .

Precious metals:

- Stronger U.S. yields and weak industrial offtake, especially auto are suppressing any upside momentum.

- Stronger US Dollar due to anticipation of rate hike in US is weighing on precious metal prices.

LPG Market Update

- For August 2026, Saudi Aramco Contract Prices (CPs) rebounded to USD 620/ton for propane and USD 640/ton for butane, compared with USD 580/ton and USD 600/ton, respectively, in July. This represents a 6.9% month-on-month increase in propane CPs and a 6.7% month-on-month increase in butane CPs.

- Sonatrach raised its August propane OSP by 4.2% m-o-m, from $518/ton to $540/ton, while the butane OSP was cut by 5.0%, from $600/ton to $570/ton.

- India’s commercial LPG prices eased further in August, with the 19 kg cylinder price in New Delhi declining by ₹192, from ₹2,930 in July to ₹2,738 as of 3 August 2026. Despite the recent correction, commercial LPG remains substantially above its pre-war level of ₹1,741/cylinder. In contrast, the 14.2 kg domestic LPG cylinder remained unchanged at ₹942, reflecting continued price stability for household consumers.

Impact Assessment of US/Israel-Iran Conflict

- Saudi Arabia proposed a multinational maritime defense coalition, with support from 14 countries including Turkey, Pakistan, Egypt, Sudan, and Djibouti, to strengthen security in the Bab el-Mandeb Strait, Red Sea, and Gulf of Aden.

- Attacks on refineries in the Middle East and Russia have tightened global fuel supplies, pushing refining margins for diesel, gasoline, and jet fuel to record or multi-year highs despite crude oil prices decline.

- The disruption has boosted profits for European and US refiners, highlighting that limited refining capacity has become a bigger driver of fuel prices than crude oil availability.

- ADNOC sold at least 12 mln bbl of spot crude in its latest tender, part of more than 86 mln bbl sold across seven tenders since Jun'26 to Asian buyers at premiums of up to 4 USD/bbl over Dubai benchmarks as US-Iran tensions tightened regional oil supplies.

- Meanwhile, transit through the Strait of Hormuz remained subdued, with 7 vessels on 26th Jul'26, 3 vessels on 25th Jul'26 (all with transponders switched off), and 7 vessels on 24th Jul'26, reflecting continued caution over disruptions to key global oil trade routes.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

War Scenarios Point to Global Supply Deficit of 0.92–1.07 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 4.10 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks continue to progress positively, with tanker flows through the Strait of Hormuz gradually normalizing over the next 4–5 weeks. Supply recovers steadily, while demand improves at a slower pace and remains below pre-war expectations, resulting in a moderate market surplus.

- Scenario 2 (Alternate): The Strait of Hormuz normalizes over the next 4–5 weeks, supporting a gradual recovery in oil exports and supply. Demand rebounds more strongly than in Scenario 1, reducing the market surplus, although overall consumption remains below pre-war levels.

Geopolitical backdrop:

US-Saudi forces carried out coordinated airstrikes on Iran-aligned PMF positions in Iraq in response to alleged IRGC-directed drone attacks, while the US intercepted Iranian ballistic missiles targeting its base in Jordan, ending a five-day lull in hostilities and signaling renewed escalation. Meanwhile, Iran rejected Oman's proposal for joint management of the Strait of Hormuz, demanding greater control over shipping routes and warning the strait could remain closed if its terms are not met, raising concerns over global energy security. Despite President Trump's renewed push for peace talks, Iran remains skeptical. Markets are likely to stay cautious as the fragile situation leaves the risk of further military escalation and renewed volatility in oil and financial markets.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 7.3%.

Base metals:

- Copper prices are up 0.4% on a weekly basis, as Fed holds interest rates, China copper premium rises to 13 month high, and inflation pressures ease with softer CPI and weaker job data despite persistent geopolitical conflicts. Prices receive continued support from CME-LME arbitrage, backwardation structure, exchange inventory outflows, and persistent mine supply constraints which offset pressure from renewed tensions, hawkish Fed outlook, and elevated global inventories.

- Aluminum prices are up 1.2% on a weekly basis due to renewed tensions and Fed outcome .

Precious metals:

- Stronger U.S. yields and weak industrial offtake, especially auto are suppressing any upside momentum.

- Stronger US Dollar due to anticipation of rate hike in US is weighing on precious metal prices.

LPG Market Update

- India has significantly reduced its dependence on Gulf LPG cargoes, increasing spot purchases from the United States to compensate for lower arrivals from Qatar and other Gulf exporters. LPG sourcing has also diversified to suppliers such as Angola,Australia,Singapore, Nigeria and Oman.

- Freight rates for LPG carriers remain elevated, as longer voyage distances, higher war-risk insurance premiums and vessel scarcity continue to increase delivered LPG costs into Asia, even where cargo availability is adequate.

Impact Assessment of US/Israel-Iran Conflict

- Renewed Middle East hostilities intensified after a drone strike hit Egypt's Damietta gas port and the US and Iran exchanged fresh attacks, raising concerns over the security of key energy shipping routes through the Strait of Hormuz and Bab el-Mandeb.

- Amid the escalating tensions, China reportedly held talks with Yemen's Houthis to safeguard its oil shipments, Saudi Arabia shifted more Asia-bound crude exports via the Suez Canal.

- ADNOC sold at least 12 mln bbl of spot crude in its latest tender, part of more than 86 mln bbl sold across seven tenders since Jun'26 to Asian buyers at premiums of up to 4 USD/bbl over Dubai benchmarks as US-Iran tensions tightened regional oil supplies.

- Thirty-seven commodity ships transited the Bab el-Mandeb Strait on Tuesday (20 inbound and 17 outbound), the highest daily count since 19th Jul'26, while only five commodity ships passed through the Strait of Hormuz (three inbound and two outbound).

- Among the vessels, three laden Aframax crude tankers carried over 1.9 mln bbl of oil, while two inbound tankers transported around 0.35 mln bbl of MTBE (methyl tertiary butyl ether) and nearly 0.09 mln bbl of chemicals, even as Houthi attacks and geopolitical tensions continued to disrupt regional shipping.

- Meanwhile, transit through the Strait of Hormuz remained subdued, with 7 vessels on 26th Jul'26, 3 vessels on 25th Jul'26 (all with transponders switched off), and 7 vessels on 24th Jul'26, reflecting continued caution over disruptions to key global oil trade routes.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

War Scenarios Point to Global Supply Deficit of 0.92–1.07 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 4.10 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks continue to progress positively, with tanker flows through the Strait of Hormuz gradually normalizing over the next 4–5 weeks. Supply recovers steadily, while demand improves at a slower pace and remains below pre-war expectations, resulting in a moderate market surplus.

- Scenario 2 (Alternate): The Strait of Hormuz normalizes over the next 4–5 weeks, supporting a gradual recovery in oil exports and supply. Demand rebounds more strongly than in Scenario 1, reducing the market surplus, although overall consumption remains below pre-war levels.

Geopolitical backdrop:

US-Saudi forces carried out coordinated airstrikes on Iran-aligned PMF positions in Iraq in response to alleged IRGC-directed drone attacks, while the US intercepted Iranian ballistic missiles targeting its base in Jordan, ending a five-day lull in hostilities and signaling renewed escalation. Meanwhile, Iran rejected Oman's proposal for joint management of the Strait of Hormuz, demanding greater control over shipping routes and warning the strait could remain closed if its terms are not met, raising concerns over global energy security. Despite President Trump's renewed push for peace talks, Iran remains skeptical. Markets are likely to stay cautious as the fragile situation leaves the risk of further military escalation and renewed volatility in oil and financial markets.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 7.4%.

Base metals:

- Copper prices are down 1.5% on a weekly basis, ahead of FOMC meeting tonight. However, downside remains capped as China copper premium rises to 13 month high and inflation pressures ease with softer CPI and weaker job data despite persistent geopolitical conflicts. Prices receive continued support from CME-LME arbitrage, backwardation structure, exchange inventory outflows, and persistent mine supply constraints which offset pressure from renewed tensions, hawkish Fed outlook, and elevated global inventories.

- Aluminum prices are down 0.8% on a weekly basis due to expectations of a hawkish signal by Fed during the latest FOMC meeting.

Precious metals:

- Stronger U.S. yields and weak industrial offtake, especially auto are suppressing any upside momentum.

- Stronger US Dollar due to anticipation of rate hike in US is weighing on precious metal prices.

LPG Market Update

- India has significantly reduced its dependence on Gulf LPG cargoes, increasing spot purchases from the United States to compensate for lower arrivals from Qatar and other Gulf exporters. LPG sourcing has also diversified to suppliers such as Angola,Australia,Singapore, Nigeria and Oman.

- Freight rates for LPG carriers remain elevated, as longer voyage distances, higher war-risk insurance premiums and vessel scarcity continue to increase delivered LPG costs into Asia, even where cargo availability is adequate.

Impact Assessment of US/Israel-Iran Conflict

- API data showed a larger than expected 3.3 mln bbl draw in crude stocks, alongside increases of 0.92 mln bbl in gasoline and 0.36 mln bbl in distillate inventories ahead of the EIA's official report.

- Trump stated that the US is engaged in constructive talks with Iran and expressed optimism about the prospects for a potential agreement, while warning that the US is prepared to take strong military action if diplomatic efforts fail.

- Thirty-seven commodity ships transited the Bab el-Mandeb Strait on Tuesday (20 inbound and 17 outbound), the highest daily count since 19th Jul'26, while only five commodity ships passed through the Strait of Hormuz (three inbound and two outbound).

- Among the vessels, three laden Aframax crude tankers carried over 1.9 mln bbl of oil, while two inbound tankers transported around 0.35 mln bbl of MTBE (methyl tertiary butyl ether) and nearly 0.09 mln bbl of chemicals, even as Houthi attacks and geopolitical tensions continued to disrupt regional shipping.

- Meanwhile, transit through the Strait of Hormuz remained subdued, with 7 vessels on 26th Jul'26, 3 vessels on 25th Jul'26 (all with transponders switched off), and 7 vessels on 24th Jul'26, reflecting continued caution over disruptions to key global oil trade routes.

- Market grapevine indicates that China is negotiating directly with Yemen's Houthi movement to ensure its oil tankers can safely transit the Red Sea despite the group's maritime blockade targeting Saudi-linked shipping.

- The discussions underscore Beijing's efforts to protect crude supplies from Saudi Arabia as escalating regional tensions continue to disrupt global shipping routes.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

War Scenarios Point to Global Supply Deficit of 0.92–1.07 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 4.10 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks continue to progress positively, with tanker flows through the Strait of Hormuz gradually normalizing over the next 4–5 weeks. Supply recovers steadily, while demand improves at a slower pace and remains below pre-war expectations, resulting in a moderate market surplus.

- Scenario 2 (Alternate): The Strait of Hormuz normalizes over the next 4–5 weeks, supporting a gradual recovery in oil exports and supply. Demand rebounds more strongly than in Scenario 1, reducing the market surplus, although overall consumption remains below pre-war levels.

Geopolitical backdrop:

US-Saudi forces carried out coordinated airstrikes on Iran-aligned PMF positions in Iraq in response to alleged IRGC-directed drone attacks, while the US intercepted Iranian ballistic missiles targeting its base in Jordan, ending a five-day lull in hostilities and signaling renewed escalation. Meanwhile, Iran rejected Oman's proposal for joint management of the Strait of Hormuz, demanding greater control over shipping routes and warning the strait could remain closed if its terms are not met, raising concerns over global energy security. Despite President Trump's renewed push for peace talks, Iran remains skeptical. Markets are likely to stay cautious as the fragile situation leaves the risk of further military escalation and renewed volatility in oil and financial markets.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 7.4%.

Base metals:

- Copper prices are down 1.5% on a weekly basis, ahead of FOMC meeting tonight. However, downside remains capped as China copper premium rises to 13 month high and inflation pressures ease with softer CPI and weaker job data despite persistent geopolitical conflicts. Prices receive continued support from CME-LME arbitrage, backwardation structure, exchange inventory outflows, and persistent mine supply constraints which offset pressure from renewed tensions, hawkish Fed outlook, and elevated global inventories.

- Aluminum prices are down 0.8% on a weekly basis due to expectations of a hawkish signal by Fed during the latest FOMC meeting.

Precious metals:

- Stronger U.S. yields and weak industrial offtake, especially auto are suppressing any upside momentum.

- Stronger US Dollar due to anticipation of rate hike in US is weighing on precious metal prices.

LPG Market Update

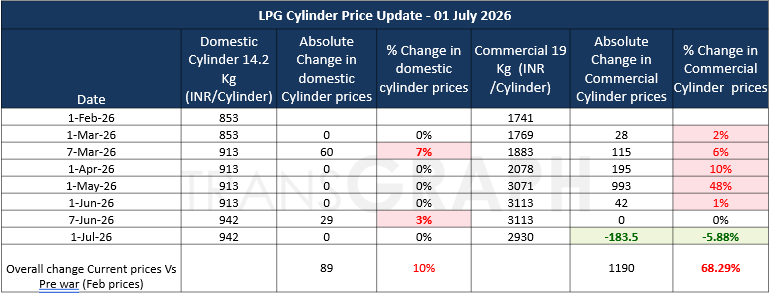

- As of 1 July 2026, India has reduced the price of the 19 kg commercial LPG cylinder by INR 183.5 per cylinder, lowering it from INR 3,113 to INR 2,930. The reduction reflects the recent easing in international LPG prices and freight rates following the de-escalation of geopolitical tensions in the Middle East, which has improved global supply conditions and reduced import costs.

- In response to the improving supply outlook, the Government has also begun rolling back several emergency measures implemented during the recent LPG supply disruption. Supplies of non-domestic packed LPG have been fully restored, while bulk LPG allocations to commercial and industrial consumers have been increased to 50% of pre-crisis consumption levels. These measures are expected to provide significant relief to LPG-dependent sectors, including manufacturing industries, hotels, restaurants, catering services, and other commercial establishments, while supporting a gradual normalization of the domestic LPG market.

Impact Assessment of US/Israel-Iran Conflict

- Trump stated that the US is engaged in constructive talks with Iran and expressed optimism about the prospects for a potential agreement, while warning that the US is prepared to take strong military action if diplomatic efforts fail.

- Pakistan, backed by China, is exploring the resumption of stalled US-Iran peace talks amid escalating Middle East tensions, although progress remains challenging as continued Houthi attacks, the near-closure of the Strait of Hormuz, and disruptions in the Red Sea have heightened geopolitical risks, with Islamabad emphasizing that a halt to attacks on Saudi Arabia and other Gulf states is a prerequisite for renewed negotiations.

- Ship traffic through the Bab el-Mandeb Strait fell to 11 commodity vessels on 26th Jul'26, the lowest level in months, including 7 oil tankers, after Houthi attacks on Saudi oil facilities intensified concerns over Red Sea shipping, driving physical crude prices in the Middle East, Europe, and Africa to two-month highs.

- Meanwhile, transit through the Strait of Hormuz remained subdued, with 7 vessels on 26th Jul'26, 3 vessels on 25th Jul'26 (all with transponders switched off), and 7 vessels on 24th Jul'26, reflecting continued caution over disruptions to key global oil trade routes.

- The EU sanctioned Georgia's Kulevi refinery in its 21st sanctions package for processing Russian crude, imposing a transaction ban effective in six months, despite the refinery's commitment to stop refining Russian oil by Aug'26–Sep'26 after processing over 650,000 metric tons in the first half of 2026 and exporting products worth 811 mln Euro to the EU and US between Feb'23 and Feb'26.

- Kuwait's sale of a 49% stake in its oil pipeline network mirrors similar Gulf infrastructure deals, but heightened geopolitical risks from the Iran conflict and potential disruptions to oil exports make this transaction significantly riskier for both investors and the government.

- India's MRPL has, for the first time, instructed crude suppliers to avoid transit through the Red Sea and the Strait of Hormuz in its spot import tenders, reflecting growing concerns over supply disruptions amid escalating Middle East tensions.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

War Scenarios Point to Global Supply Deficit of 0.92–1.07 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 4.10 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks continue to progress positively, with tanker flows through the Strait of Hormuz gradually normalizing over the next 4–5 weeks. Supply recovers steadily, while demand improves at a slower pace and remains below pre-war expectations, resulting in a moderate market surplus.

- Scenario 2 (Alternate): The Strait of Hormuz normalizes over the next 4–5 weeks, supporting a gradual recovery in oil exports and supply. Demand rebounds more strongly than in Scenario 1, reducing the market surplus, although overall consumption remains below pre-war levels.

Geopolitical backdrop:

The United States paused its airstrike campaign against Iran after 13 consecutive nights of attacks, while Iran announced it would also halt retaliatory strikes as long as Washington maintains the pause, reaffirming its "attack-for-attack" policy. According to U.S. officials, President Donald Trump temporarily suspended the bombing campaign to create space for diplomacy after military advisers warned that most pre-selected targets had been exhausted and prolonged operations could further deplete U.S. munitions.

Despite the temporary lull, Iranian officials remain skeptical, viewing the pause as a tactical move rather than a genuine shift in U.S. policy. The de-escalation has eased immediate concerns over disruptions to the Strait of Hormuz, reducing the geopolitical risk premium in crude oil prices. However, markets are expected to remain cautious as the situation remains fragile and any renewed military action could quickly reignite volatility in energy and financial markets.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 7.4%.

Base metals:

- Copper prices are up 1.3% on a weekly basis, as China copper premium rises to 13 month high and inflation pressures ease with softer CPI and weaker job data despite persistent geopolitical conflicts. Prices receive continued support from CME-LME arbitrage, backwardation structure, exchange inventory outflows, and persistent mine supply constraints which offset pressure from renewed tensions, hawkish Fed outlook, and elevated global inventories.

- Renewed tensions and weaker US CPI release is supporting aluminum prices. Prices are up 1.1% on a weekly basis.

Precious metals:

- Stronger U.S. yields and weak industrial offtake, especially auto are suppressing any upside momentum.

- Stronger US Dollar due to anticipation of rate hike in US is weighing on precious metal prices.

LPG Market Update

- As of 1 July 2026, India has reduced the price of the 19 kg commercial LPG cylinder by INR 183.5 per cylinder, lowering it from INR 3,113 to INR 2,930. The reduction reflects the recent easing in international LPG prices and freight rates following the de-escalation of geopolitical tensions in the Middle East, which has improved global supply conditions and reduced import costs.

- In response to the improving supply outlook, the Government has also begun rolling back several emergency measures implemented during the recent LPG supply disruption. Supplies of non-domestic packed LPG have been fully restored, while bulk LPG allocations to commercial and industrial consumers have been increased to 50% of pre-crisis consumption levels. These measures are expected to provide significant relief to LPG-dependent sectors, including manufacturing industries, hotels, restaurants, catering services, and other commercial establishments, while supporting a gradual normalization of the domestic LPG market.

Impact Assessment of US/Israel-Iran Conflict

- Pakistan, backed by China, is exploring the resumption of stalled US-Iran peace talks amid escalating Middle East tensions, although progress remains challenging as continued Houthi attacks, the near-closure of the Strait of Hormuz, and disruptions in the Red Sea have heightened geopolitical risks, with Islamabad emphasizing that a halt to attacks on Saudi Arabia and other Gulf states is a prerequisite for renewed negotiations.

- Ship traffic through the Bab el-Mandeb Strait fell to 11 commodity vessels on 26th Jul'26, the lowest level in months, including 7 oil tankers, after Houthi attacks on Saudi oil facilities intensified concerns over Red Sea shipping, driving physical crude prices in the Middle East, Europe, and Africa to two-month highs.

- Meanwhile, transit through the Strait of Hormuz remained subdued, with 7 vessels on 26th Jul'26, 3 vessels on 25th Jul'26 (all with transponders switched off), and 7 vessels on 24th Jul'26, reflecting continued caution over disruptions to key global oil trade routes.

- Iran-aligned Houthi rebels attacked two Saudi oil tankers in the Red Sea, raising fears of disruptions to the Bab el-Mandeb and Strait of Hormuz, while U.S.-Iran tensions escalated with continued airstrikes, missile exchanges, and threats of further military action.

- As the conflict widened across the Middle East, shipping costs increased, oil exports were disrupted, and concerns grew over inflation, global economic stability, and mounting political pressure on the Trump administration despite congressional efforts to limit US military involvement.

- Tanker traffic through the Strait of Hormuz fell to just one outbound vessel and zero inbound vessels on 23rd Jul'26 (down from three crossings the previous day), while 32 tankers transited the Bab el-Mandeb Strait (up from 26), highlighting significant shipping disruptions that have driven oil prices back to around 100 USD/bbl and prompted rerouting of cargoes via the Suez Canal.

- Chinese refiners have increased purchases of Russian ESPO crude despite narrower discounts (1–3 USD/bbl vs. 4 USD/bbl previously) and resumed negotiations for Iranian crude (Pars at 8 USD/bbl discount and Iran Light at 3–4 USD/bbl discount to ICE Brent) as Middle East supply disruptions and shipping risks intensified amid the Iran conflict.

- China's crude oil imports plunged 41.3% YoY to 7.12 MBpd in Jun'26, the lowest since Oct'16, while refinery throughput fell 17.7% to 12.47 MBpd, reflecting weaker demand and reliance on stockpiles during the Iran conflict.

- Although China drew about 0.94 MBpd from inventories in Jun'26 and still added around 0.53 MBpd to reserves in the first half of the year, it may increase refinery runs and fuel exports as Asian refining margins have widened.

- The EU sanctioned Georgia's Kulevi refinery in its 21st sanctions package for processing Russian crude, imposing a transaction ban effective in six months, despite the refinery's commitment to stop refining Russian oil by Aug'26–Sep'26 after processing over 650,000 metric tons in the first half of 2026 and exporting products worth 811 mln Euro to the EU and US between Feb'23 and Feb'26.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

War Scenarios Point to Global Supply Deficit of 0.92–1.07 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 4.10 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks continue to progress positively, with tanker flows through the Strait of Hormuz gradually normalizing over the next 4–5 weeks. Supply recovers steadily, while demand improves at a slower pace and remains below pre-war expectations, resulting in a moderate market surplus.

- Scenario 2 (Alternate): The Strait of Hormuz normalizes over the next 4–5 weeks, supporting a gradual recovery in oil exports and supply. Demand rebounds more strongly than in Scenario 1, reducing the market surplus, although overall consumption remains below pre-war levels.

Geopolitical backdrop:

The United States paused its airstrike campaign against Iran after 13 consecutive nights of attacks, while Iran announced it would also halt retaliatory strikes as long as Washington maintains the pause, reaffirming its "attack-for-attack" policy. According to U.S. officials, President Donald Trump temporarily suspended the bombing campaign to create space for diplomacy after military advisers warned that most pre-selected targets had been exhausted and prolonged operations could further deplete U.S. munitions.

Despite the temporary lull, Iranian officials remain sceptical, viewing the pause as a tactical move rather than a genuine shift in U.S. policy. The de-escalation has eased immediate concerns over disruptions to the Strait of Hormuz, reducing the geopolitical risk premium in crude oil prices. However, markets are expected to remain cautious as the situation remains fragile and any renewed military action could quickly reignite volatility in energy and financial markets.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 7.4%.

Base metals:

- Copper prices are up 1.8% on a weekly basis, as China copper premium rises to 13 month high and inflation pressures ease with softer CPI and weaker job data despite persistent geopolitical conflicts. Prices receive continued support from CME-LME arbitrage, backwardation structure, exchange inventory outflows, and persistent mine supply constraints which offset pressure from renewed tensions, hawkish Fed outlook, and elevated global inventories.

- Renewed tensions and weaker US CPI release is supporting aluminum prices. Prices are up 0.7% on a weekly basis.

Precious metals:

- Stronger U.S. yields and weak industrial offtake, especially auto are suppressing any upside momentum.

- Stronger US Dollar due to anticipation of rate hike in US is weighing on precious metal prices.

LPG Market Update

- As of 1 July 2026, India has reduced the price of the 19 kg commercial LPG cylinder by INR 183.5 per cylinder, lowering it from INR 3,113 to INR 2,930. The reduction reflects the recent easing in international LPG prices and freight rates following the de-escalation of geopolitical tensions in the Middle East, which has improved global supply conditions and reduced import costs.

- In response to the improving supply outlook, the Government has also begun rolling back several emergency measures implemented during the recent LPG supply disruption. Supplies of non-domestic packed LPG have been fully restored, while bulk LPG allocations to commercial and industrial consumers have been increased to 50% of pre-crisis consumption levels. These measures are expected to provide significant relief to LPG-dependent sectors, including manufacturing industries, hotels, restaurants, catering services, and other commercial establishments, while supporting a gradual normalization of the domestic LPG market.

Impact Assessment of US/Israel-Iran Conflict

- Iran-aligned Houthi rebels attacked two Saudi oil tankers in the Red Sea, raising fears of disruptions to the Bab el-Mandeb and Strait of Hormuz, while U.S.-Iran tensions escalated with continued airstrikes, missile exchanges, and threats of further military action.

- As the conflict widened across the Middle East, shipping costs increased, oil exports were disrupted, and concerns grew over inflation, global economic stability, and mounting political pressure on the Trump administration despite congressional efforts to limit U.S. military involvement.

- Tanker traffic through the Strait of Hormuz fell to just one outbound vessel and zero inbound vessels on 23rd Jul'26 (down from three crossings the previous day), while 32 tankers transited the Bab el-Mandeb Strait (up from 26), highlighting significant shipping disruptions that have driven oil prices back to around 100 USD/bbl and prompted rerouting of cargoes via the Suez Canal.

- Chinese refiners have increased purchases of Russian ESPO crude despite narrower discounts (1–3 USD/bbl vs. 4 USD/bbl previously) and resumed negotiations for Iranian crude (Pars at 8 USD/bbl discount and Iran Light at 3–4 USD/bbl discount to ICE Brent) as Middle East supply disruptions and shipping risks intensified amid the Iran conflict.

- China's crude oil imports plunged 41.3% YoY to 7.12 MBpd in Jun'26, the lowest since Oct'16, while refinery throughput fell 17.7% to 12.47 MBpd, reflecting weaker demand and reliance on stockpiles during the Iran conflict.

- Although China drew about 0.94 MBpd from inventories in Jun'26 and still added around 0.53 MBpd to reserves in the first half of the year, it may increase refinery runs and fuel exports as Asian refining margins have widened.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

War Scenarios Point to Global Supply Deficit of 0.92–1.07 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 4.10 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks continue to progress positively, with tanker flows through the Strait of Hormuz gradually normalizing over the next 4–5 weeks. Supply recovers steadily, while demand improves at a slower pace and remains below pre-war expectations, resulting in a moderate market surplus.

- Scenario 2 (Alternate): The Strait of Hormuz normalizes over the next 4–5 weeks, supporting a gradual recovery in oil exports and supply. Demand rebounds more strongly than in Scenario 1, reducing the market surplus, although overall consumption remains below pre-war levels.

Geopolitical backdrop:

The United States paused its airstrike campaign against Iran after 13 consecutive nights of attacks, while Iran announced it would also halt retaliatory strikes as long as Washington maintains the pause, reaffirming its "attack-for-attack" policy. According to U.S. officials, President Donald Trump temporarily suspended the bombing campaign to create space for diplomacy after military advisers warned that most pre-selected targets had been exhausted and prolonged operations could further deplete U.S. munitions.

Despite the temporary lull, Iranian officials remain sceptical, viewing the pause as a tactical move rather than a genuine shift in U.S. policy. The de-escalation has eased immediate concerns over disruptions to the Strait of Hormuz, reducing the geopolitical risk premium in crude oil prices. However, markets are expected to remain cautious as the situation remains fragile and any renewed military action could quickly reignite volatility in energy and financial markets.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 7.4%.

Base metals:

- Copper prices are up 1.8% on a weekly basis, as China copper premium rises to 13 month high and inflation pressures ease with softer CPI and weaker job data despite persistent geopolitical conflicts. Prices receive continued support from CME-LME arbitrage, backwardation structure, exchange inventory outflows, and persistent mine supply constraints which offset pressure from renewed tensions, hawkish Fed outlook, and elevated global inventories.

- Renewed tensions and weaker US CPI release is supporting aluminum prices. Prices are up 0.7% on a weekly basis.

Precious metals:

- Stronger U.S. yields and weak industrial offtake, especially auto are suppressing any upside momentum.

- Stronger US Dollar due to anticipation of rate hike in US is weighing on precious metal prices.

LPG Market Update

- As of 1 July 2026, India has reduced the price of the 19 kg commercial LPG cylinder by INR 183.5 per cylinder, lowering it from INR 3,113 to INR 2,930. The reduction reflects the recent easing in international LPG prices and freight rates following the de-escalation of geopolitical tensions in the Middle East, which has improved global supply conditions and reduced import costs.

- In response to the improving supply outlook, the Government has also begun rolling back several emergency measures implemented during the recent LPG supply disruption. Supplies of non-domestic packed LPG have been fully restored, while bulk LPG allocations to commercial and industrial consumers have been increased to 50% of pre-crisis consumption levels. These measures are expected to provide significant relief to LPG-dependent sectors, including manufacturing industries, hotels, restaurants, catering services, and other commercial establishments, while supporting a gradual normalization of the domestic LPG market.