The Middle East conflict introduced significant volatility into global sugar markets. In sugar’s case, the linkage with energy markets initially proved supportive for prices. NY #11 raw sugar futures rose from 13.89 c/lb at the end of February to 15.87 c/lb by 26 March, representing an increase of nearly 15%.

However, the first half of April saw a sharp correction, pushing NY #11 back to pre-Iran conflict levels, as the market continued to face a short-term oversupply environment. Strong supply prospects from key producers, including Pakistan, China, and Thailand, coupled with balanced trade flows supported by strong Brazilian exports, continued to weigh on sentiment and cap upside momentum.

From late April through early May, sugar prices regained momentum, with NY #11 frequently trading in the 14.5–15.0 c/lb range. The move was primarily driven by crude oil prices and broader macro sentiment rather than sugar-specific catalysts.

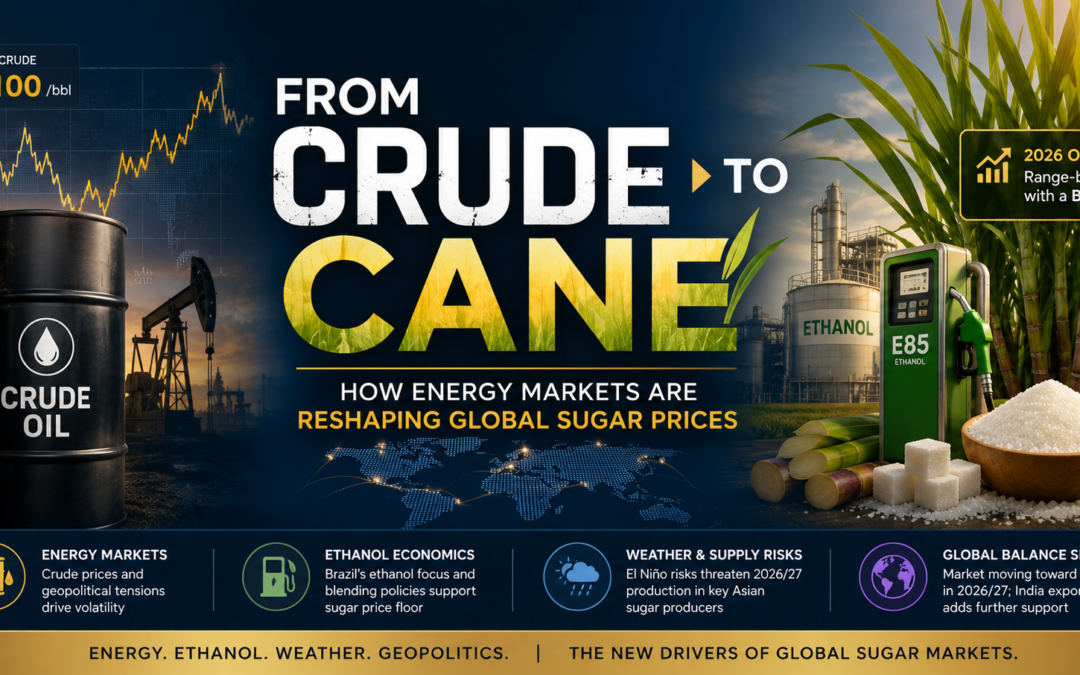

At the same time, a more constructive outlook emerged from Brazil, where the harvest began with a strong ethanol focus. Since October last year, hydrous ethanol economics have consistently outperformed sugar returns, encouraging mills to allocate a greater share of cane toward ethanol production.

Previously, sugar had traded more as a leveraged expression of crude oil movements, with geopolitical developments exerting an outsized influence on price direction. While tensions in the Middle East have eased somewhat, uncertainty remains elevated and continues to support energy markets. Brent crude prices are near USD 100 per barrel and persistent geopolitical risk continue to improve the relative attractiveness of biofuels.

As long as uncertainty surrounding middle east remains unresolved, downside price corrections may remain relatively shallow, supporting a pattern of higher lows and limiting aggressive downside moves.

Additional support could emerge from Brazil’s proposed increase in the ethanol blending mandate from 30% to 32% during June–July, which would further strengthen domestic ethanol demand.

Fuel market indicators also remain supportive. Pump prices in Sao Paulo averaged BRL 6.50/liter for gasoline and BRL 4.07/liter for ethanol, resulting in a parity of 62.6%, a level that remains highly favorable for biofuel consumption and ethanol competitiveness.

However, several developments continue to limit the market’s bullish potential. The Brazilian government issued a Provisional Measure introducing a subsidy mechanism for gasoline producers and importers. The proposed subsidy could reach as high as BRL 0.89/liter on sales of Gasoline to the distributors.

The measure aims to offset a potential increase in gasoline prices at Petrobras refineries amid elevated global crude prices. Currently, the gap between international gasoline prices and Petrobras pricing exceeds BRL 2.0/liter.

At the same time, Petrobras indicated that refinery gasoline prices could rise by approximately 15%.

If Petrobras proceeds with refinery price increases, a portion of the subsidy could be absorbed within the supply chain rather than being fully transferred to consumers. Consequently, retail gasoline prices may not decline significantly, implying limited changes to ethanol competitiveness.

The market is now awaiting further clarity regarding the final subsidy structure, implementation timing, and Petrobras’ pricing decisions. Until greater visibility emerges, ethanol economics are likely to remain relatively supportive versus sugar production.

Meanwhile, weather conditions in Center-South Brazil remain broadly favorable for sugarcane development, while stronger-than-expected sugar production in Pakistan, China, and Thailand has reinforced near-term supply availability.

Further, attention is increasingly shifting toward 2026/27 supply risks. The probability of El Nino exceeds 80% from July onward, posing risks to crop prospects across major Asian producers including India, Thailand, Pakistan, and Indonesia. Reduced cane acreage in Thailand and lower beet area in the EU also present downside risks to future production.

India’s ban on sugar exports is another bullish factor for the global sugar market.

Most balance sheet models indicate that the global sugar market is moving toward a deficit in 2026/27, with TransGraph projecting -0.97 MMT, while market estimates range between -0.26 MMT and -3.2 MMT.

Conclusion:

Looking ahead to 2026, the sugar market is likely to trade within a broad range, before potentially entering sustained bullish cycle. Strong global supply, particularly from Brazil, could limit significant upside moves, while sugar-versus-ethanol economics, El Nino-related risks and their potential impact on production in India and Thailand, alongside energy market volatility, may continue to provide periodic support. As a result, the market could remain range-bound with a bullish bias, where macro developments and weather disruptions trigger rallies, while strong supply fundamentals cap gains.