Impact Assessment of US/Israel-Iran Conflict

Impact Assessment of US/Israel-Iran Conflict

- The US crude exports reached a record high of 5.6 MBpd in May'26 due to the Middle East crisis, which increased demand from Asian and European refiners. The US and Israel's war with Iran disrupted global energy markets, causing refiners to seek alternatives to Middle Eastern supply. US crude exports surged past the previous record set in Apr'26 of 5.2 MBpd, with Asia taking 2.45 MBpd and Europe 2.4 MBpd of the barrels exported in May'26.

- According to market grapevines the Lukoil-owned Volgograd oil refinery in Russia's south has suspended oil processing since 29th May'26 due to a Ukrainian drone attack that caused fire and damages. The attack has halted the crude distillation unit CDU-1, which accounts for 40% of the plant's capacity, and stopped other units CDU-6 and CDU-5.

- The refinery processed 13.5 million metric tons of oil in 2024, accounting for 5% of total Russian refinery volume, producing 6 million tons of diesel, 1.9 million tons of gasoline, and 700,000 tons of fuel oil.

- Iran is seeking a limited interim agreement with the United States to ease economic pressure, stabilise the situation at home, and avoid major concessions on its nuclear programme. The approach reflects a familiar playbook for the Islamic Republic: absorb pressure, avoid irreversible compromises and keep negotiations alive without shifting core positions.

- India will cut its export duties on petrol, diesel, and aviation turbine fuel (ATF) for the fortnight starting 01st Jun'26, based on average international prices of crude oil, petrol, diesel, and ATF since the last review. The duty on exports of petrol has been set at 1.5 rupees per litre, while that on diesel has been set at 13.5 rupees per litre.

- Export duties on ATF have been set at 9.5 rupees per litre. There is no change in the existing excise duty rates on petrol and diesel cleared for domestic consumption.

- China's seaborne crude oil imports fell to their lowest in almost 10 years in May, dropping to 6.36 MBpd, due to the impact of the Iran war and the closure of the Strait of Hormuz.

- The collapse in China's imports is being framed as helping Asia adjust to the loss of at least 10 MBpd of crude, but it is a serendipitous side effect rather than any altruism on Beijing's part.

- The primary driver behind the collapse in China's oil imports is the conflict in the Middle East, but the real challenge is in working out the why and how of what China is doing to adapt to the loss of as much as 10% of global crude supplies from the Iran conflict.

- According to the Energy Information Administration the US crude production remained steady at 13.7 MBpd in Mar'26. Texas crude output fell to a four-month low, while New Mexico production was unchanged. The US crude production is expected to rise as operators increase output in response to high oil prices due to the Iran war.

- Venezuela's oil exports rose to 1.25 MBpd in May'26, marking the third consecutive month of increase, driven by more cargoes to the US, India, and Europe. Under the US-supported government of interim President Rodriguez, Venezuelan crude production and exports have bounced this year as Washington eased sanctions and foreign companies expanded oil and gas projects in the OPEC nation.

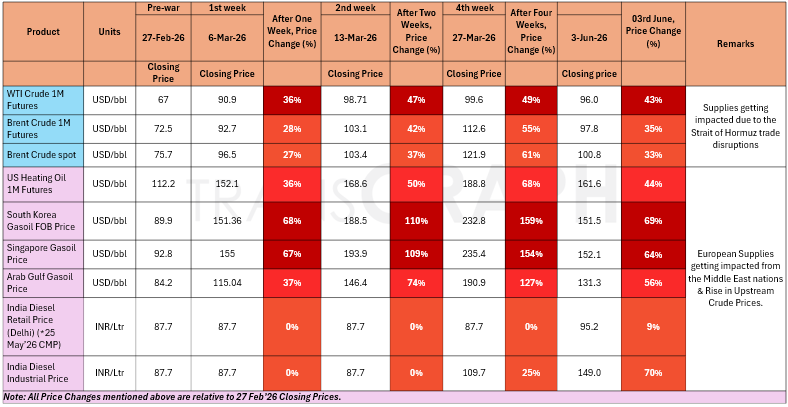

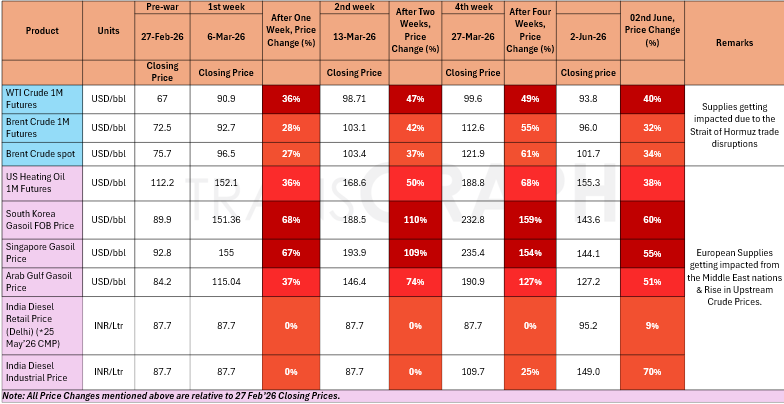

War Impact on Crude Oil & Gasoil/Diesel Prices

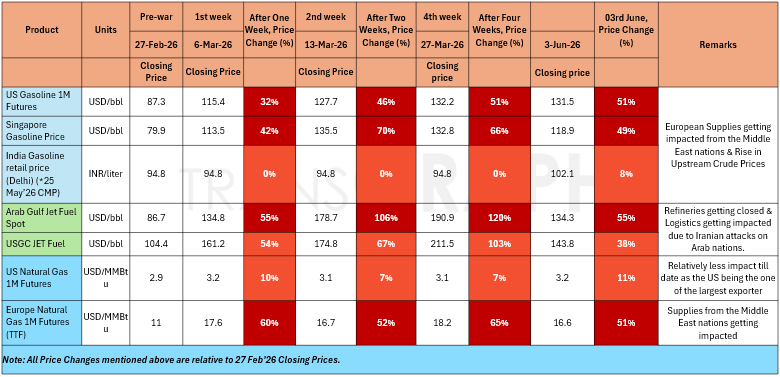

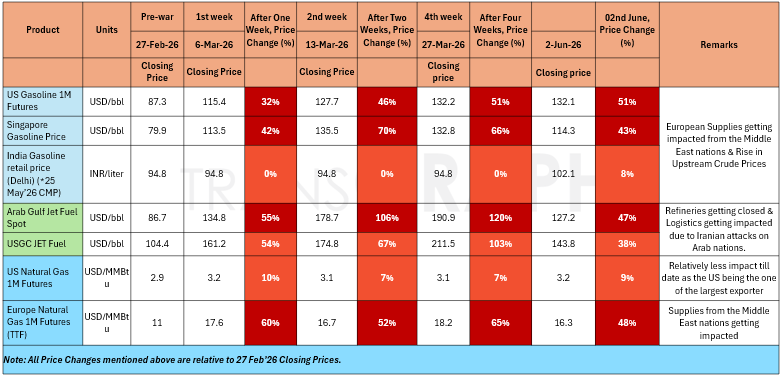

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks to remain on a progressive note and flows through the Strait of Hormuz improving over the coming weeks; however crude oil production losses will be there due to further non-availability of storage on on-shore in Iraq, Kuwait and other small Middle East nations.

- Scenario 2 (Alternate): No major deal being achieved from ceasefire talks and post completion of ceasefire talks, tensions continuing to remain in the Middle East and flows through the Strait of Hormuz continuing to remain restrained. Crude Oil Production Facilities & Refining Centers in the Middle East region getting affected and trade disruptions in Strait of Hormuz will be there for medium to long term (4 to 7 months).

Brent Crude 1M Futures are expected to trade in a range of 100 USD/bbl to 125 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

Metals & Energy Market Update – Geopolitical Context (Iran Conflict)

Geopolitical backdrop:

The ongoing conflict in the Middle East, continues to weigh on global markets and keeping inflation expectations elevated. The war-driven rise in energy prices has heightened concerns about higher transportation and manufacturing costs globally, adding further pressure to already elevated inflation. At the same time, elevated crude prices continue to weigh on emerging markets and developing economies, particularly large energy-importing nations, as higher import bills and currency pressures weaken economic stability and complicate monetary policy decisions in the nearterm.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

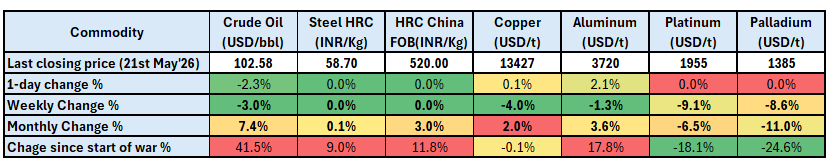

- Since, the start of war steel HRC prices are up by 9.0%.

Base metals:

- Copper ended last week up by 0.5%, primarily due to widening LME-CME spread.

- Aluminum rose by 19.4% since start of war linked to Gulf region supply disruptions. However, demand softness now driving price action.

- IMF downgraded 2026 global growth to 3.1% (from 3.3% earlier and 3.4% in 2025), highlighting war-related downside risks.

Precious metals:

- Volatility has eased, but prices face upward pressure, due to improving market sentiment in peace talks.

- However, any esclation and halt in a resolution will pressure on Precious Metals.

- Stronger U.S. yields and weak industrial offtake—especially auto—are suppressing any upside momentum.

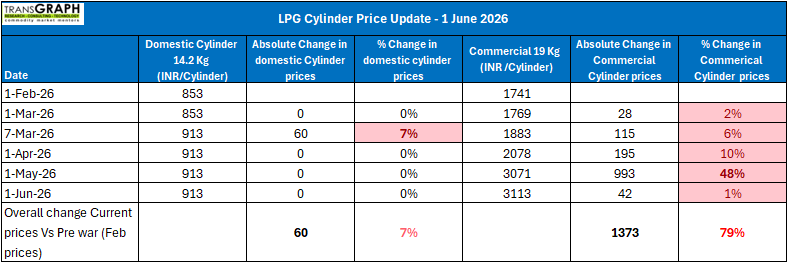

LPG Market Update - 02 June 2026

- India's LPG market saw another upward revision on 1st June 2026 , with oil marketing companies increasing commercial cylinder prices Commercial LPG prices were raised across major cities, with the 19 kg cylinder in Delhi increasing by Rs 42 to Rs 3,113.50. Similar hikes were reported nationwide, ranging from Rs 42 to Rs 53.50 per cylinder. Kolkata recorded the sharpest increase of Rs 53.50, taking prices to Rs 3,255.50, while Hyderabad and Bhubaneswar saw hikes of Rs 52 each. Mumbai's commercial LPG price rose by Rs 43.50 to Rs 3,067.50, and Chennai's rate increased by Rs 46 to Rs 3,283.00.

- In addition to commercial cylinders, oil marketing companies also increased the price of 5 kg Free Trade LPG (FTL) cylinders by Rs 11. Following the revision, the retail price of a 5 kg FTL cylinder in Delhi now stands at Rs 821.50. FTL cylinders are sold outside the subsidized domestic LPG system and are commonly used by migrant workers, temporary households, street vendors, and consumers requiring smaller LPG packs.

- For June, Saudi Aramco CPs increased further to USD 760/ton for propane and USD 820/ton for butane, reflecting continued market tightness and persistent concerns over Middle East supply security.

In contrast, Algeria's Sonatrach moved in the opposite direction, implementing substantial reductions in its June LPG benchmarks. Propane prices were cut by USD 125/ton to USD 575/ton, representing an 18% decline from May levels. Butane experienced an even sharper correction, falling by USD 270/ton to USD 610/ton, a drop of approximately 31%.

Impact Assessment of US/Israel-Iran Conflict

- The US crude exports reached a record high of 5.6 MBpd in May'26 due to the Middle East crisis, which increased demand from Asian and European refiners. The US and Israel's war with Iran disrupted global energy markets, causing refiners to seek alternatives to Middle Eastern supply. US crude exports surged past the previous record set in Apr'26 of 5.2 MBpd, with Asia taking 2.45 MBpd and Europe 2.4 MBpd of the barrels exported in May'26.

- According to market grapevines the Lukoil-owned Volgograd oil refinery in Russia's south has suspended oil processing since 29th May'26 due to a Ukrainian drone attack that caused fire and damages. The attack has halted the crude distillation unit CDU-1, which accounts for 40% of the plant's capacity, and stopped other units CDU-6 and CDU-5.

- The refinery processed 13.5 million metric tons of oil in 2024, accounting for 5% of total Russian refinery volume, producing 6 million tons of diesel, 1.9 million tons of gasoline, and 700,000 tons of fuel oil.

- Iran is seeking a limited interim agreement with the United States to ease economic pressure, stabilise the situation at home, and avoid major concessions on its nuclear programme. The approach reflects a familiar playbook for the Islamic Republic: absorb pressure, avoid irreversible compromises and keep negotiations alive without shifting core positions.

- India will cut its export duties on petrol, diesel, and aviation turbine fuel (ATF) for the fortnight starting 01st Jun'26, based on average international prices of crude oil, petrol, diesel, and ATF since the last review. The duty on exports of petrol has been set at 1.5 rupees per litre, while that on diesel has been set at 13.5 rupees per litre.

- Export duties on ATF have been set at 9.5 rupees per litre. There is no change in the existing excise duty rates on petrol and diesel cleared for domestic consumption.

- China's seaborne crude oil imports fell to their lowest in almost 10 years in May, dropping to 6.36 MBpd, due to the impact of the Iran war and the closure of the Strait of Hormuz.

- The collapse in China's imports is being framed as helping Asia adjust to the loss of at least 10 MBpd of crude, but it is a serendipitous side effect rather than any altruism on Beijing's part.

- The primary driver behind the collapse in China's oil imports is the conflict in the Middle East, but the real challenge is in working out the why and how of what China is doing to adapt to the loss of as much as 10% of global crude supplies from the Iran conflict.

- According to the Energy Information Administration the US crude production remained steady at 13.7 MBpd in Mar'26. Texas crude output fell to a four-month low, while New Mexico production was unchanged. The US crude production is expected to rise as operators increase output in response to high oil prices due to the Iran war.

- Venezuela's oil exports rose to 1.25 MBpd in May'26, marking the third consecutive month of increase, driven by more cargoes to the US, India, and Europe. Under the US-supported government of interim President Rodriguez, Venezuelan crude production and exports have bounced this year as Washington eased sanctions and foreign companies expanded oil and gas projects in the OPEC nation.

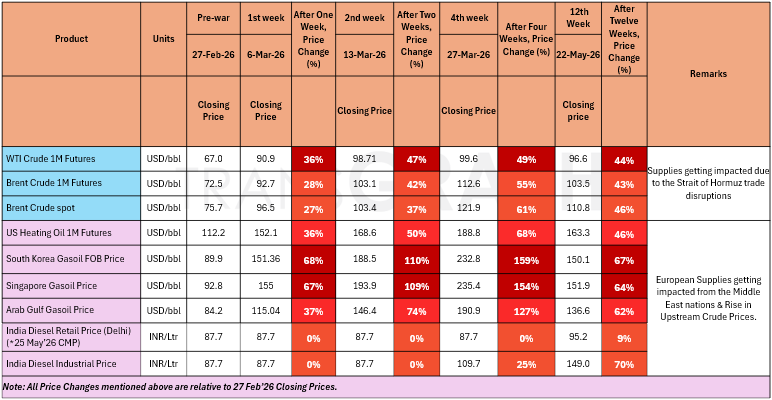

War Impact on Crude Oil & Gasoil/Diesel Prices

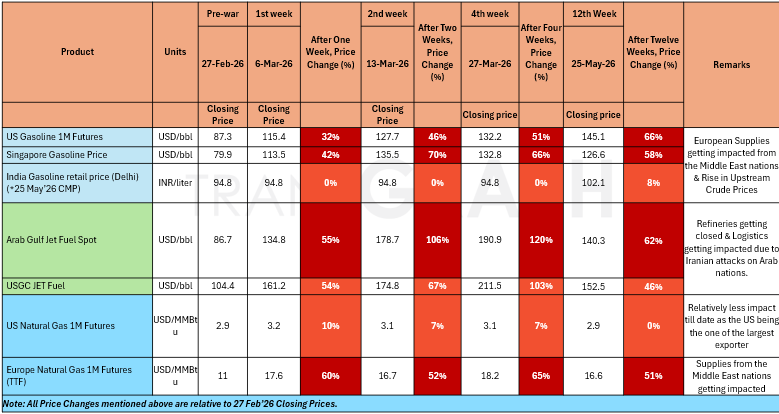

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks to remain on a progressive note and flows through the Strait of Hormuz improving over the coming weeks; however crude oil production losses will be there due to further non-availability of storage on on-shore in Iraq, Kuwait and other small Middle East nations.

- Scenario 2 (Alternate): No major deal being achieved from ceasefire talks and post completion of ceasefire talks, tensions continuing to remain in the Middle East and flows through the Strait of Hormuz continuing to remain restrained. Crude Oil Production Facilities & Refining Centers in the Middle East region getting affected and trade disruptions in Strait of Hormuz will be there for medium to long term (4 to 7 months).

Brent Crude 1M Futures are expected to trade in a range of 100 USD/bbl to 125 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

Metals & Energy Market Update – Geopolitical Context (Iran Conflict)

Geopolitical backdrop:

The ongoing conflict in the Middle East, continues to weigh on global markets and keeping inflation expectations elevated. The war-driven rise in energy prices has heightened concerns about higher transportation and manufacturing costs globally, adding further pressure to already elevated inflation. At the same time, elevated crude prices continue to weigh on emerging markets and developing economies, particularly large energy-importing nations, as higher import bills and currency pressures weaken economic stability and complicate monetary policy decisions in the nearterm.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 9.0%.

Base metals:

- Copper ended last week up by 0.5%, primarily due to widening LME-CME spread.

- Aluminum rose by 19.4% since start of war linked to Gulf region supply disruptions. However, demand softness now driving price action.

- IMF downgraded 2026 global growth to 3.1% (from 3.3% earlier and 3.4% in 2025), highlighting war-related downside risks.

Precious metals:

- Volatility has eased, but prices face upward pressure, due to improving market sentiment in peace talks.

- However, any esclation and halt in a resolution will pressure on Precious Metals.

- Stronger U.S. yields and weak industrial offtake—especially auto—are suppressing any upside momentum.

LPG Market Update - 02 June 2026

- India's LPG market saw another upward revision on 1st June 2026 , with oil marketing companies increasing commercial cylinder prices Commercial LPG prices were raised across major cities, with the 19 kg cylinder in Delhi increasing by Rs 42 to Rs 3,113.50. Similar hikes were reported nationwide, ranging from Rs 42 to Rs 53.50 per cylinder. Kolkata recorded the sharpest increase of Rs 53.50, taking prices to Rs 3,255.50, while Hyderabad and Bhubaneswar saw hikes of Rs 52 each. Mumbai's commercial LPG price rose by Rs 43.50 to Rs 3,067.50, and Chennai's rate increased by Rs 46 to Rs 3,283.00.

- In addition to commercial cylinders, oil marketing companies also increased the price of 5 kg Free Trade LPG (FTL) cylinders by Rs 11. Following the revision, the retail price of a 5 kg FTL cylinder in Delhi now stands at Rs 821.50. FTL cylinders are sold outside the subsidized domestic LPG system and are commonly used by migrant workers, temporary households, street vendors, and consumers requiring smaller LPG packs.

- For June, Saudi Aramco CPs increased further to USD 760/ton for propane and USD 820/ton for butane, reflecting continued market tightness and persistent concerns over Middle East supply security.

In contrast, Algeria's Sonatrach moved in the opposite direction, implementing substantial reductions in its June LPG benchmarks. Propane prices were cut by USD 125/ton to USD 575/ton, representing an 18% decline from May levels. Butane experienced an even sharper correction, falling by USD 270/ton to USD 610/ton, a drop of approximately 31%.

Impact Assessment of US/Israel-Iran Conflict

- The US crude exports reached a record high of 5.6 MBpd in May'26 due to the Middle East crisis, which increased demand from Asian and European refiners. The US and Israel's war with Iran disrupted global energy markets, causing refiners to seek alternatives to Middle Eastern supply. US crude exports surged past the previous record set in Apr'26 of 5.2 MBpd, with Asia taking 2.45 MBpd and Europe 2.4 MBpd of the barrels exported in May'26.

- According to market grapevines the Lukoil-owned Volgograd oil refinery in Russia's south has suspended oil processing since 29th May'26 due to a Ukrainian drone attack that caused fire and damages. The attack has halted the crude distillation unit CDU-1, which accounts for 40% of the plant's capacity, and stopped other units CDU-6 and CDU-5.

- The refinery processed 13.5 million metric tons of oil in 2024, accounting for 5% of total Russian refinery volume, producing 6 million tons of diesel, 1.9 million tons of gasoline, and 700,000 tons of fuel oil.

- Iran is seeking a limited interim agreement with the United States to ease economic pressure, stabilise the situation at home, and avoid major concessions on its nuclear programme. The approach reflects a familiar playbook for the Islamic Republic: absorb pressure, avoid irreversible compromises and keep negotiations alive without shifting core positions.

- India will cut its export duties on petrol, diesel, and aviation turbine fuel (ATF) for the fortnight starting 01st Jun'26, based on average international prices of crude oil, petrol, diesel, and ATF since the last review. The duty on exports of petrol has been set at 1.5 rupees per litre, while that on diesel has been set at 13.5 rupees per litre.

- Export duties on ATF have been set at 9.5 rupees per litre. There is no change in the existing excise duty rates on petrol and diesel cleared for domestic consumption.

- China's seaborne crude oil imports fell to their lowest in almost 10 years in May, dropping to 6.36 MBpd, due to the impact of the Iran war and the closure of the Strait of Hormuz.

- The collapse in China's imports is being framed as helping Asia adjust to the loss of at least 10 MBpd of crude, but it is a serendipitous side effect rather than any altruism on Beijing's part.

- The primary driver behind the collapse in China's oil imports is the conflict in the Middle East, but the real challenge is in working out the why and how of what China is doing to adapt to the loss of as much as 10% of global crude supplies from the Iran conflict.

- According to the Energy Information Administration the US crude production remained steady at 13.7 MBpd in Mar'26. Texas crude output fell to a four-month low, while New Mexico production was unchanged. The US crude production is expected to rise as operators increase output in response to high oil prices due to the Iran war.

- Venezuela's oil exports rose to 1.25 MBpd in May'26, marking the third consecutive month of increase, driven by more cargoes to the US, India, and Europe. Under the US-supported government of interim President Rodriguez, Venezuelan crude production and exports have bounced this year as Washington eased sanctions and foreign companies expanded oil and gas projects in the OPEC nation.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks to remain on a progressive note and flows through the Strait of Hormuz improving over the coming weeks; however crude oil production losses will be there due to further non-availability of storage on on-shore in Iraq, Kuwait and other small Middle East nations.

- Scenario 2 (Alternate): No major deal being achieved from ceasefire talks and post completion of ceasefire talks, tensions continuing to remain in the Middle East and flows through the Strait of Hormuz continuing to remain restrained. Crude Oil Production Facilities & Refining Centers in the Middle East region getting affected and trade disruptions in Strait of Hormuz will be there for medium to long term (4 to 7 months).

Brent Crude 1M Futures are expected to trade in a range of 100 USD/bbl to 125 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

Metals & Energy Market Update – Geopolitical Context (Iran Conflict)

Geopolitical backdrop:

The ongoing conflict in the Middle East, continues to weigh on global markets and keeping inflation expectations elevated. The war-driven rise in energy prices has heightened concerns about higher transportation and manufacturing costs globally, adding further pressure to already elevated inflation. At the same time, elevated crude prices continue to weigh on emerging markets and developing economies, particularly large energy-importing nations, as higher import bills and currency pressures weaken economic stability and complicate monetary policy decisions in the nearterm.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 9.0%.

Base metals:

- Copper ended last week up by 0.5%, primarily due to widening LME-CME spread.

- Aluminum rose by 19.4% since start of war linked to Gulf region supply disruptions. However, demand softness now driving price action.

- IMF downgraded 2026 global growth to 3.1% (from 3.3% earlier and 3.4% in 2025), highlighting war-related downside risks.

Precious metals:

- Volatility has eased, but prices face upward pressure, due to improving market sentiment in peace talks.

- However, any esclation and halt in a resolution will pressure on Precious Metals.

- Stronger U.S. yields and weak industrial offtake—especially auto—are suppressing any upside momentum.

LPG Market Update - 02 June 2026

- India's LPG market saw another upward revision on 1st June 2026 , with oil marketing companies increasing commercial cylinder prices Commercial LPG prices were raised across major cities, with the 19 kg cylinder in Delhi increasing by Rs 42 to Rs 3,113.50. Similar hikes were reported nationwide, ranging from Rs 42 to Rs 53.50 per cylinder. Kolkata recorded the sharpest increase of Rs 53.50, taking prices to Rs 3,255.50, while Hyderabad and Bhubaneswar saw hikes of Rs 52 each. Mumbai's commercial LPG price rose by Rs 43.50 to Rs 3,067.50, and Chennai's rate increased by Rs 46 to Rs 3,283.00.

- In addition to commercial cylinders, oil marketing companies also increased the price of 5 kg Free Trade LPG (FTL) cylinders by Rs 11. Following the revision, the retail price of a 5 kg FTL cylinder in Delhi now stands at Rs 821.50. FTL cylinders are sold outside the subsidized domestic LPG system and are commonly used by migrant workers, temporary households, street vendors, and consumers requiring smaller LPG packs.

- For June, Saudi Aramco CPs increased further to USD 760/ton for propane and USD 820/ton for butane, reflecting continued market tightness and persistent concerns over Middle East supply security.

In contrast, Algeria's Sonatrach moved in the opposite direction, implementing substantial reductions in its June LPG benchmarks. Propane prices were cut by USD 125/ton to USD 575/ton, representing an 18% decline from May levels. Butane experienced an even sharper correction, falling by USD 270/ton to USD 610/ton, a drop of approximately 31%.

Impact Assessment of US/Israel-Iran Conflict

- India will cut its export duties on petrol, diesel, and aviation turbine fuel (ATF) for the fortnight starting June 1, based on average international prices of crude oil, petrol, diesel, and ATF since the last review. The duty on exports of petrol has been set at 1.5 rupees per litre, while that on diesel has been set at 13.5 rupees per litre.

- Export duties on ATF have been set at 9.5 rupees per litre. There is no change in the existing excise duty rates on petrol and diesel cleared for domestic consumption.

- China’s seaborne crude oil imports fell to their lowest in almost 10 years in May, dropping to 6.36 MBpd, due to the impact of the Iran war and the closure of the Strait of Hormuz.

- The collapse in China’s imports is being framed as helping Asia adjust to the loss of at least 10 MBpd of crude, but it is a serendipitous side effect rather than any altruism on Beijing’s part.

- The primary driver behind the collapse in China’s oil imports is the conflict in the Middle East, but the real challenge is in working out the why and how of what China is doing to adapt to the loss of as much as 10% of global crude supplies from the Iran conflict.

- According to the Energy Information Administration the US crude production remained steady at 13.7 MBpd in Mar’26. Texas crude output fell to a four-month low, while New Mexico production was unchanged. The US crude production is expected to rise as operators increase output in response to high oil prices due to the Iran war.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia’s East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND’25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE’s Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 – 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks to remain on a progressive note and flows through the Strait of Hormuz improving over the coming weeks; however crude oil production losses will be there due to further non-availability of storage on on-shore in Iraq, Kuwait and other small Middle East nations.

- Scenario 2 (Alternate): No major deal being achieved from ceasefire talks and post completion of ceasefire talks, tensions continuing to remain in the Middle East and flows through the Strait of Hormuz continuing to remain restrained. Crude Oil Production Facilities & Refining Centers in the Middle East region getting affected and trade disruptions in Strait of Hormuz will be there for medium to long term (4 to 7 months).

Brent Crude 1M Futures are expected to trade in a range of 100 USD/bbl to 125 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

Metals & Energy Market Update – Geopolitical Context (Iran Conflict)

Geopolitical backdrop:

The ongoing conflict in the Middle East, continues to weigh on global markets and keeping inflation expectations elevated. The war-driven rise in energy prices has heightened concerns about higher transportation and manufacturing costs globally, adding further pressure to already elevated inflation. At the same time, elevated crude prices continue to weigh on emerging markets and developing economies, particularly large energy-importing nations, as higher import bills and currency pressures weaken economic stability and complicate monetary policy decisions in the nearterm.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 9.0%.

Base metals:

- Copper ended last week up by 0.5%, primarily due to widening LME-CME spread.

- Aluminum rose by 19.4% since start of war linked to Gulf region supply disruptions. However, demand softness now driving price action.

- IMF downgraded 2026 global growth to 3.1% (from 3.3% earlier and 3.4% in 2025), highlighting war-related downside risks.

Precious metals:

- Volatility has eased, but prices face upward pressure, due to improving market sentiment in peace talks.

- However, any esclation and halt in a resolution will pressure on Precious Metals.

- Stronger U.S. yields and weak industrial offtake—especially auto—are suppressing any upside momentum.

LPG Market Update – 01 June 2026

- India’s LPG market saw another upward revision on 1st June 2026 , with oil marketing companies increasing commercial cylinder prices Commercial LPG prices were raised across major cities, with the 19 kg cylinder in Delhi increasing by Rs 42 to Rs 3,113.50. Similar hikes were reported nationwide, ranging from Rs 42 to Rs 53.50 per cylinder. Kolkata recorded the sharpest increase of Rs 53.50, taking prices to Rs 3,255.50, while Hyderabad and Bhubaneswar saw hikes of Rs 52 each. Mumbai’s commercial LPG price rose by Rs 43.50 to Rs 3,067.50, and Chennai’s rate increased by Rs 46 to Rs 3,283.00.

- In addition to commercial cylinders, oil marketing companies also increased the price of 5 kg Free Trade LPG (FTL) cylinders by Rs 11. Following the revision, the retail price of a 5 kg FTL cylinder in Delhi now stands at Rs 821.50. FTL cylinders are sold outside the subsidized domestic LPG system and are commonly used by migrant workers, temporary households, street vendors, and consumers requiring smaller LPG packs.

Impact Assessment of US/Israel-Iran Conflict

- The US crude oil inventories fell for a sixth straight week last week, according to American Petroleum Institute data released on 27th May'26. Crude stocks decreased by 2.8 mln bbl, while gasoline inventories fell by 3.2 mln bbl and distillate inventories rose by 1.1 mln bbl compared to the previous week.

- On 27th May'26, the US military shot down four Iranian attack drones and struck a ground control station in Bandar Abbas, following an Iranian drone operation posing a threat to US forces and commercial shipping in the Strait of Hormuz.

- A cargo of US Strategic Petroleum Reserve oil headed to California for the first time ever, highlighting the redrawing of trade flows and shipping routes due to the Iran war. California, once a top oil-producing state, has become more dependent on crude imports, including from the Middle East.

- About 0.46 bbl of Bayou Choctaw Sweet crude went to Chevron's Richmond refinery and another 0.05 bbl to its El Segundo refinery, while a supertanker unloaded the cargo to two smaller ships that took it to the refineries in California.

- According to PPAC data, Indian refiners' crude throughput fell 8.9% month-on-month in April to 5.23 MBpd, Indian Oil Corp, Bharat Petroleum Corp Ltd, Hindustan Petroleum Corp Ltd, Mangalore Refinery and Petrochemicals Ltd, and Reliance Industries Ltd all experienced drops in production.

- CPCL's CBR refinery is decommissioned due to limitations in meeting product specifications with the existing configuration. .

- Iran accused the US of violating a ceasefire by striking targets near the Strait of Hormuz, complicating efforts to end the war. Israel continued to bomb Lebanon, further straining peace efforts.

- The war has caused an unprecedented oil supply shock, pushing up the costs of fuel, fertiliser, and food. Iran and the US have made progress on a memorandum of understanding that would lead to further negotiations over a final agreement, but key issues remain unresolved, including Iran's nuclear program and the conflict in Lebanon.

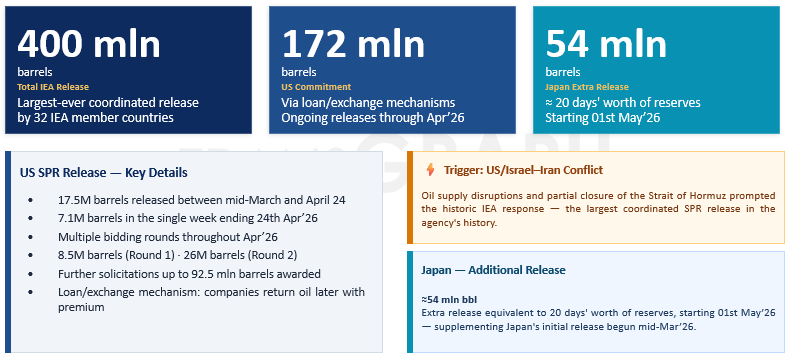

- A cargo of crude oil from the US Strategic Petroleum Reserve is heading to the Philippines, the first shipment to Asia since Nov'22. The shipment is part of a coordinated effort by the International Energy Agency to release 400 mln bbl of oil to quell rising prices, as the Iran war upends global supplies and the Strait of Hormuz remains largely closed.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks to remain on a progressive note and flows through the Strait of Hormuz improving over the coming weeks; however crude oil production losses will be there due to further non-availability of storage on on-shore in Iraq, Kuwait and other small Middle East nations.

- Scenario 2 (Alternate): No major deal being achieved from ceasefire talks and post completion of ceasefire talks, tensions continuing to remain in the Middle East and flows through the Strait of Hormuz continuing to remain restrained. Crude Oil Production Facilities & Refining Centers in the Middle East region getting affected and trade disruptions in Strait of Hormuz will be there for medium to long term (4 to 7 months).

Brent Crude 1M Futures are expected to trade in a range of 100 USD/bbl to 125 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

Metals & Energy Market Update – Geopolitical Context (Iran Conflict)

Geopolitical backdrop:

The ongoing conflict in the Middle East, continues to weigh on global markets and keeping inflation expectations elevated as crude oil prices remained above USD 100/Barrel amid persistent supply disruption concerns. The war-driven rise in energy prices has heightened concerns about higher transportation and manufacturing costs globally, adding further pressure to already elevated inflation. At the same time, elevated crude prices continue to weigh on emerging markets and developing economies, particularly large energy-importing nations, as higher import bills and currency pressures weaken economic stability and complicate monetary policy decisions in the near term.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 9.0%.

Base metals:

- Copper ended last week up by 1.1%, primarily due to widening CME-LME spread.

- Aluminum rose by 19% since start of war linked to Gulf region supply disruptions. However, demand softness now driving price action.

- IMF downgraded 2026 global growth to 3.1% (from 3.3% earlier and 3.4% in 2025), highlighting war-related downside risks.

Precious metals:

- Volatility has eased, but prices face upward pressure, due to improving market sentiment in peace talks.

- However, any esclation and halt in a resolution will pressure on Precious Metals.

- Stronger U.S. yields and weak industrial offtake—especially auto—are suppressing any upside momentum.

LPG Market Update - 26 May 2026

- Saudi Aramco increased its June 2026 CPs to USD 760/ton for propane and USD 820/ton for butane, compared to USD 750/ton and USD 800/ton in May, showing that the global LPG market remains tight. The rise mainly reflects ongoing geopolitical tensions in the Gulf, with disruptions around Hormuz and Saudi export infrastructure continuing to keep supply concerns elevated. Butane prices saw stronger support from steady Asian petrochemical demand and better gasoline blending margins. Even with softer crude prices, the latest CPs suggest that supply security remains the key factor driving LPG prices.

- On 25 May 2026, the Government of India introduced an amendment to LPG supply regulations that makes the shift from LPG to PNG more flexible for consumers. Households taking a PNG connection can either surrender their LPG connection within 30 days or retain future eligibility through a transfer voucher if they later move to a non PNG area.

Auto DraftImpact Assessment of US/Israel-Iran Conflict

- The US crude oil inventories fell for a sixth straight week last week, according to American Petroleum Institute data released on 27th May'26. Crude stocks decreased by 2.8 mln bbl, while gasoline inventories fell by 3.2 mln bbl and distillate inventories rose by 1.1 mln bbl compared to the previous week.

- On 27th May'26, the US military shot down four Iranian attack drones and struck a ground control station in Bandar Abbas, following an Iranian drone operation posing a threat to US forces and commercial shipping in the Strait of Hormuz.

- A cargo of US Strategic Petroleum Reserve oil headed to California for the first time ever, highlighting the redrawing of trade flows and shipping routes due to the Iran war. California, once a top oil-producing state, has become more dependent on crude imports, including from the Middle East.

- About 0.46 bbl of Bayou Choctaw Sweet crude went to Chevron's Richmond refinery and another 0.05 bbl to its El Segundo refinery, while a supertanker unloaded the cargo to two smaller ships that took it to the refineries in California.

- According to PPAC data, Indian refiners' crude throughput fell 8.9% month-on-month in April to 5.23 MBpd, Indian Oil Corp, Bharat Petroleum Corp Ltd, Hindustan Petroleum Corp Ltd, Mangalore Refinery and Petrochemicals Ltd, and Reliance Industries Ltd all experienced drops in production.

- CPCL's CBR refinery is decommissioned due to limitations in meeting product specifications with the existing configuration. .

- Iran accused the US of violating a ceasefire by striking targets near the Strait of Hormuz, complicating efforts to end the war. Israel continued to bomb Lebanon, further straining peace efforts.

- The war has caused an unprecedented oil supply shock, pushing up the costs of fuel, fertiliser, and food. Iran and the US have made progress on a memorandum of understanding that would lead to further negotiations over a final agreement, but key issues remain unresolved, including Iran's nuclear program and the conflict in Lebanon.

- A cargo of crude oil from the US Strategic Petroleum Reserve is heading to the Philippines, the first shipment to Asia since Nov'22. The shipment is part of a coordinated effort by the International Energy Agency to release 400 mln bbl of oil to quell rising prices, as the Iran war upends global supplies and the Strait of Hormuz remains largely closed.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks to remain on a progressive note and flows through the Strait of Hormuz improving over the coming weeks; however crude oil production losses will be there due to further non-availability of storage on on-shore in Iraq, Kuwait and other small Middle East nations.

- Scenario 2 (Alternate): No major deal being achieved from ceasefire talks and post completion of ceasefire talks, tensions continuing to remain in the Middle East and flows through the Strait of Hormuz continuing to remain restrained. Crude Oil Production Facilities & Refining Centers in the Middle East region getting affected and trade disruptions in Strait of Hormuz will be there for medium to long term (4 to 7 months).

Brent Crude 1M Futures are expected to trade in a range of 100 USD/bbl to 125 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

Metals & Energy Market Update – Geopolitical Context (Iran Conflict)

Geopolitical backdrop:

The ongoing conflict in the Middle East, continues to weigh on global markets and keeping inflation expectations elevated as crude oil prices remained above USD 100/Barrel amid persistent supply disruption concerns. The war-driven rise in energy prices has heightened concerns about higher transportation and manufacturing costs globally, adding further pressure to already elevated inflation. At the same time, elevated crude prices continue to weigh on emerging markets and developing economies, particularly large energy-importing nations, as higher import bills and currency pressures weaken economic stability and complicate monetary policy decisions in the near term.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 9.0%.

Base metals:

- Copper ended last week up by 1.1%, primarily due to widening CME-LME spread.

- Aluminum rose by 19% since start of war linked to Gulf region supply disruptions. However, demand softness now driving price action.

- IMF downgraded 2026 global growth to 3.1% (from 3.3% earlier and 3.4% in 2025), highlighting war-related downside risks.

Precious metals:

- Volatility has eased, but prices face upward pressure, due to improving market sentiment in peace talks.

- However, any esclation and halt in a resolution will pressure on Precious Metals.

- Stronger U.S. yields and weak industrial offtake—especially auto—are suppressing any upside momentum.

LPG Market Update - 26 May 2026

- Saudi Aramco increased its June 2026 CPs to USD 760/ton for propane and USD 820/ton for butane, compared to USD 750/ton and USD 800/ton in May, showing that the global LPG market remains tight. The rise mainly reflects ongoing geopolitical tensions in the Gulf, with disruptions around Hormuz and Saudi export infrastructure continuing to keep supply concerns elevated. Butane prices saw stronger support from steady Asian petrochemical demand and better gasoline blending margins. Even with softer crude prices, the latest CPs suggest that supply security remains the key factor driving LPG prices.

- On 25 May 2026, the Government of India introduced an amendment to LPG supply regulations that makes the shift from LPG to PNG more flexible for consumers. Households taking a PNG connection can either surrender their LPG connection within 30 days or retain future eligibility through a transfer voucher if they later move to a non PNG area.

Impact Assessment of US/Israel-Iran Conflict

- According to PPAC data, Indian refiners' crude throughput fell 8.9% month-on-month in April to 5.23 MBpd, Indian Oil Corp, Bharat Petroleum Corp Ltd, Hindustan Petroleum Corp Ltd, Mangalore Refinery and Petrochemicals Ltd, and Reliance Industries Ltd all experienced drops in production.

- CPCL's CBR refinery is decommissioned due to limitations in meeting product specifications with the existing configuration. .

- Iran accused the US of violating a ceasefire by striking targets near the Strait of Hormuz, complicating efforts to end the war. Israel continued to bomb Lebanon, further straining peace efforts.

- The war has caused an unprecedented oil supply shock, pushing up the costs of fuel, fertiliser, and food. Iran and the US have made progress on a memorandum of understanding that would lead to further negotiations over a final agreement, but key issues remain unresolved, including Iran's nuclear program and the conflict in Lebanon.

- A cargo of crude oil from the US Strategic Petroleum Reserve is heading to the Philippines, the first shipment to Asia since Nov'22. The shipment is part of a coordinated effort by the International Energy Agency to release 400 mln bbl of oil to quell rising prices, as the Iran war upends global supplies and the Strait of Hormuz remains largely closed

- The US Secretary of State Marco Rubio said negotiations with Iran could take a few days, quashing hopes for an immediate end to the conflict. The US forces conducted defensive strikes in southern Iran, targeting boats attempting to lay mines and missile launch sites.

- India's state-owned fuel retailers increased diesel and petrol prices by 2.71 rupees and 2.61 rupees per litre respectively, as they attempt to recoup some losses from higher crude costs due to the Iran war. The state companies have raised diesel prices by about 8.6% and petrol by about 7.8% since 15th May'26.

- The Ukrainian military said it struck Russia's Sheskharis oil terminal and Grushova oil depot, sparking a fire at the terminal. Ukraine has increased strikes on Russian oil refining and transportation facilities to reduce Russia's oil and gas export revenues.

- China continued to build its massive stockpile of crude oil in Apr'26, even though imports dropped to the lowest in nearly four years. China's surplus crude amounted to about 0.43 MBpd in Apr'26 as the 20% drop in imports was outweighed by refinery processing sliding to the lowest since Aug'22.

- The ongoing building of inventories by the world's biggest crude importer underlines that China is in quite a different situation to the rest of the world, which is burning through oil stockpiles in order to compensate for the loss of about 12 MBpd of supply to the effective closure of the Strait of Hormuz.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks to remain on a progressive note and flows through the Strait of Hormuz improving over the coming weeks; however crude oil production losses will be there due to further non-availability of storage on on-shore in Iraq, Kuwait and other small Middle East nations.

- Scenario 2 (Alternate): No major deal being achieved from ceasefire talks and post completion of ceasefire talks, tensions continuing to remain in the Middle East and flows through the Strait of Hormuz continuing to remain restrained. Crude Oil Production Facilities & Refining Centers in the Middle East region getting affected and trade disruptions in Strait of Hormuz will be there for medium to long term (4 to 7 months).

Brent Crude 1M Futures are expected to trade in a range of 100 USD/bbl to 125 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

Metals & Energy Market Update – Geopolitical Context (Iran Conflict)

Geopolitical backdrop:

The ongoing conflict in the Middle East, continues to weigh on global markets and keeping inflation expectations elevated as crude oil prices remained above USD 100/Barrel amid persistent supply disruption concerns. The war-driven rise in energy prices has heightened concerns about higher transportation and manufacturing costs globally, adding further pressure to already elevated inflation. At the same time, elevated crude prices continue to weigh on emerging markets and developing economies, particularly large energy-importing nations, as higher import bills and currency pressures weaken economic stability and complicate monetary policy decisions in the near term.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 9.0%.

Base metals:

- Copper ended last week up by 1.1%, primarily due to widening CME-LME spread.

- Aluminum rose by 19% since start of war linked to Gulf region supply disruptions. However, demand softness now driving price action.

- IMF downgraded 2026 global growth to 3.1% (from 3.3% earlier and 3.4% in 2025), highlighting war-related downside risks.

Precious metals:

- Volatility has eased, but prices face upward pressure, due to improving market sentiment in peace talks.

- However, any esclation and halt in a resolution will pressure on Precious Metals.

- Stronger U.S. yields and weak industrial offtake—especially auto—are suppressing any upside momentum.

LPG Market Update - 26 May 2026

- Saudi Aramco increased its June 2026 CPs to USD 760/ton for propane and USD 820/ton for butane, compared to USD 750/ton and USD 800/ton in May, showing that the global LPG market remains tight. The rise mainly reflects ongoing geopolitical tensions in the Gulf, with disruptions around Hormuz and Saudi export infrastructure continuing to keep supply concerns elevated. Butane prices saw stronger support from steady Asian petrochemical demand and better gasoline blending margins. Even with softer crude prices, the latest CPs suggest that supply security remains the key factor driving LPG prices.

- On 25 May 2026, the Government of India introduced an amendment to LPG supply regulations that makes the shift from LPG to PNG more flexible for consumers. Households taking a PNG connection can either surrender their LPG connection within 30 days or retain future eligibility through a transfer voucher if they later move to a non PNG area.

Coriander’s Sharp Recovery Raises a Bigger Question — More Upside Ahead?

Where Prices Stand?

Coriander followed a sharp leap this season. Eagle variety coriander prices in the Ramganj mandi have rallied sharply from Jan’26 levels of around ₹9,580.6/quintal to currently trading near ₹12,400/quintal, supported by tightening arrivals and improved demand sentiment.

In the Ramganj mandi, Eagle variety coriander prices witnessed a strong rally during Jan–Apr’26. Prices moved from a low of around ₹9,580.6/quintal in Jan’26 to a high of ₹12,414.3/quintal in Apr’26, supported by tightening arrivals and improved buying interest. The market is expected to remain firm during May’26 amid lower arrivals and steady demand.

The Arrival Story Is Shifting

Arrivals at key mandis were already running significantly below prior-year levels:

- Gondal market: Jan to April 2026 arrivals reached 22,407 MT down 39% YoY from 36,479 MT

- Ramganj market: Jan-Apr at 13,167 MT down 21% YoY

- Gondal’s Apr’26 arrivals fell 46% YoY to 7,595 MT signaling tighter supply even during peak harvest

Peak arrivals are now over. Seasonal inflows are expected to decline from here. The supply cushion that’s been suppressing prices is narrowing.

The Export Market Is Stalled — But That Could Change

Traditionally, Malaysia has been the largest export destination for Indian coriander, followed by the UAE, Saudi Arabia, Nepal, and Bangladesh.

Exports for JFM’26 fell 29% YoY, down to 9.44 thousand metric tons from 13.22 thousand metric ton in JFM’25.

Key destination breakdown:

Shipments to UAE and Saudi Arabia fell sharply by 45–46% YoY, indicating slower Gulf buying. Malaysia, the largest buyer, also declined by 15% YoY.

The Gulf market which drives the bulk of Indian coriander export demand has been in a cautious holding pattern, shaped by elevated freight costs and ongoing West Asia logistics disruptions tied to the Red Sea situation.

Here’s the risk: this demand hasn’t disappeared. It’s deferred. When freight normalizes or Gulf buying resumes, it could reactivate quickly absorbing available stock faster than the market anticipates. However, this would majorly depend on how prolonged the on-going war would going to be.

The Risks That Matter for the Next 3–6 Months

- Post-harvest supply tightening is already underway. With Gondal and Ramganj arrivals running 39-46% below last year and peak arrivals behind us, the supply pressure that’s been compressing prices is fading. Any pickup in domestic or export demand could tighten the market faster than current sentiment suggests.

- Red Sea and Gulf freight risk is not resolved. Export flows to the UAE and Saudi Arabia are down sharply not because of structural demand loss, but because elevated freight and logistical friction have made Gulf buyers cautious. A freight correction or geopolitical easing could flip this dynamic quickly.

- El Niño adds a forward supply risk. Weather conditions during the upcoming sowing window remain crucial for next-season supply, as strong El Niño conditions may reduce soil moisture and affect sowing. Coriander acreage is also highly price-driven, with farmers expanding acreage during higher price periods and reducing sowing when prices are weak.

The Bottom Line for Buyers

With arrivals tightening, export demand likely deferred rather than lost, and weather risks emerging for the next crop, the current coriander market still appears fundamentally supportive despite the sharp rally already witnessed.

The question isn’t just where prices are today. It’s whether your procurement structure is designed for the scenario where they aren’t here tomorrow.

What’s your current procurement horizon for coriander? Are you covered for Q3, or running spot? Subscribe to TransGraph Services, we work with food manufacturers and spice buyers to build procurement strategies that account for exactly these kinds of structural and seasonal risk factors.

Impact Assessment of US/Israel-Iran Conflict

- The US Secretary of State Marco Rubio said negotiations with Iran could take a few days, quashing hopes for an immediate end to the conflict. The US forces conducted defensive strikes in southern Iran, targeting boats attempting to lay mines and missile launch sites.

- India's state-owned fuel retailers increased diesel and petrol prices by 2.71 rupees and 2.61 rupees per litre respectively, as they attempt to recoup some losses from higher crude costs due to the Iran war. The state companies have raised diesel prices by about 8.6% and petrol by about 7.8% since 15th May'26.

- The Ukrainian military said it struck Russia's Sheskharis oil terminal and Grushova oil depot, sparking a fire at the terminal. Ukraine has increased strikes on Russian oil refining and transportation facilities to reduce Russia's oil and gas export revenues.

- China continued to build its massive stockpile of crude oil in Apr'26, even though imports dropped to the lowest in nearly four years. China's surplus crude amounted to about 0.43 MBpd in Apr'26 as the 20% drop in imports was outweighed by refinery processing sliding to the lowest since Aug'22.

- The ongoing building of inventories by the world's biggest crude importer underlines that China is in quite a different situation to the rest of the world, which is burning through oil stockpiles in order to compensate for the loss of about 12 MBpd of supply to the effective closure of the Strait of Hormuz.

- Two Chinese supertankers carrying 4 mln bbl of Middle East crude oil exited the Strait of Hormuz on 20th May'26 after waiting in the Gulf for over two months. The ships are among a handful of supertankers carrying Iraqi crude exiting the Gulf this month via a transit route that Iran has ordered ships to use. The vessels are expected to reach their destinations in China to discharge their cargo by 05th Jun'26.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks to remain on a progressive note and flows through the Strait of Hormuz improving over the coming weeks; however crude oil production losses will be there due to further non-availability of storage on on-shore in Iraq, Kuwait and other small Middle East nations.

- Scenario 2 (Alternate): No major deal being achieved from ceasefire talks and post completion of ceasefire talks, tensions continuing to remain in the Middle East and flows through the Strait of Hormuz continuing to remain restrained. Crude Oil Production Facilities & Refining Centers in the Middle East region getting affected and trade disruptions in Strait of Hormuz will be there for medium to long term (4 to 7 months).

Brent Crude 1M Futures are expected to trade in a range of 100 USD/bbl to 125 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

Metals & Energy Market Update – Geopolitical Context (Iran Conflict)

Geopolitical backdrop:

The ongoing conflict in the Middle East entered its 12th week, continuing to weigh on global markets and keeping inflation expectations elevated as crude oil prices remained above USD 100/Barrel amid persistent supply disruption concerns. The war-driven rise in energy prices has heightened concerns about higher transportation and manufacturing costs globally, adding further pressure to already elevated inflation. At the same time, elevated crude prices continue to weigh on emerging markets and developing economies, particularly large energy-importing nations, as higher import bills and currency pressures weaken economic stability and complicate monetary policy decisions in thenear term.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 9.0%.

Base metals:

- Copper ended last week down by 4.0%, primarily due to US treasury yields inching higher amid market expectations of interest rate hike in US.

- Aluminum rose by 17.8% since start of war linked to Gulf region supply disruptions. However, demand softness now driving price action.

- IMF downgraded 2026 global growth to 3.1% (from 3.3% earlier and 3.4% in 2025), highlighting war-related downside risks.

Precious metals:

- Volatility has eased, but prices face upward pressure, due to improving market sentiment in peace talks.

- However, any esclation and halt in a resolution will pressure on Precious Metals.

- Stronger U.S. yields and weak industrial offtake—especially auto—are suppressing any upside momentum.

LPG Market Update - 26 May 2026

- Saudi Aramco increased its June 2026 CPs to USD 760/ton for propane and USD 820/ton for butane, compared to USD 750/ton and USD 800/ton in May, showing that the global LPG market remains tight. The rise mainly reflects ongoing geopolitical tensions in the Gulf, with disruptions around Hormuz and Saudi export infrastructure continuing to keep supply concerns elevated. Butane prices saw stronger support from steady Asian petrochemical demand and better gasoline blending margins. Even with softer crude prices, the latest CPs suggest that supply security remains the key factor driving LPG prices.

- On 25 May 2026, the Government of India introduced an amendment to LPG supply regulations that makes the shift from LPG to PNG more flexible for consumers. Households taking a PNG connection can either surrender their LPG connection within 30 days or retain future eligibility through a transfer voucher if they later move to a non PNG area.

Impact Assessment of US/Israel-Iran Conflict

- The US President Donald Trump said he told his representatives not to rush into a deal with Iran, as his administration played down hopes of an imminent breakthrough in the three month old war. Trump wrote on Truth Social that the US blockade on Iranian ships in the Strait of Hormuz would remain in full force until an agreement is reached, certified, and signed.

- A senior Trump administration official said Iran had agreed in principle to open the Strait of Hormuz, in exchange for the US lifting its naval blockade and disposing of Tehran's highly enriched uranium.

- China continued to build its massive stockpile of crude oil in Apr'26, even though imports dropped to the lowest in nearly four years. China's surplus crude amounted to about 0.43 MBpd in Apr'26 as the 20% drop in imports was outweighed by refinery processing sliding to the lowest since Aug'22.

- The ongoing building of inventories by the world's biggest crude importer underlines that China is in quite a different situation to the rest of the world, which is burning through oil stockpiles in order to compensate for the loss of about 12 MBpd of supply to the effective closure of the Strait of Hormuz.

- Two Chinese supertankers carrying 4 mln bbl of Middle East crude oil exited the Strait of Hormuz on 20th May'26 after waiting in the Gulf for over two months. The ships are among a handful of supertankers carrying Iraqi crude exiting the Gulf this month via a transit route that Iran has ordered ships to use. The vessels are expected to reach their destinations in China to discharge their cargo by 05th Jun'26.

- Saudi Arabia is expected to burn more imported fuel oil for power generation this summer due to a loss of natural gas supply from oilfields shut after Iran's war curbed oil exports. The rise in fuel oil use at power plants marks a setback for the kingdom's push to switch to cleaner fuels. The burning of crude and fuel oil for power could breach 1 MBpd this summer, countering efforts to switch to more gas and renewables.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks to remain on a progressive note and flows through the Strait of Hormuz improving over the coming weeks; however crude oil production losses will be there due to further non-availability of storage on on-shore in Iraq, Kuwait and other small Middle East nations.

- Scenario 2 (Alternate): No major deal being achieved from ceasefire talks and post completion of ceasefire talks, tensions continuing to remain in the Middle East and flows through the Strait of Hormuz continuing to remain restrained. Crude Oil Production Facilities & Refining Centers in the Middle East region getting affected and trade disruptions in Strait of Hormuz will be there for medium to long term (4 to 7 months).

Brent Crude 1M Futures are expected to trade in a range of 100 USD/bbl to 125 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

Metals & Energy Market Update – Geopolitical Context (Iran Conflict)

Geopolitical backdrop:

The ongoing conflict in the Middle East entered its 12th week, continuing to weigh on global markets and keeping inflation expectations elevated as crude oil prices remained above USD 100/Barrel amid persistent supply disruption concerns. The war-driven rise in energy prices has heightened concerns about higher transportation and manufacturing costs globally, adding further pressure to already elevated inflation. At the same time, elevated crude prices continue to weigh on emerging markets and developing economies, particularly large energy-importing nations, as higher import bills and currency pressures weaken economic stability and complicate monetary policy decisions in thenear term.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 9.0%.

Base metals:

- Copper ended last week down by 4.0%, primarily due to US treasury yields inching higher amid market expectations of interest rate hike in US.

- Aluminum rose by 17.8% since start of war linked to Gulf region supply disruptions. However, demand softness now driving price action.

- IMF downgraded 2026 global growth to 3.1% (from 3.3% earlier and 3.4% in 2025), highlighting war-related downside risks.

Precious metals:

- Volatility has eased, but prices face upward pressure, due to improving market sentiment in peace talks.

- However, any esclation and halt in a resolution will pressure on Precious Metals.

- Stronger U.S. yields and weak industrial offtake—especially auto—are suppressing any upside momentum.

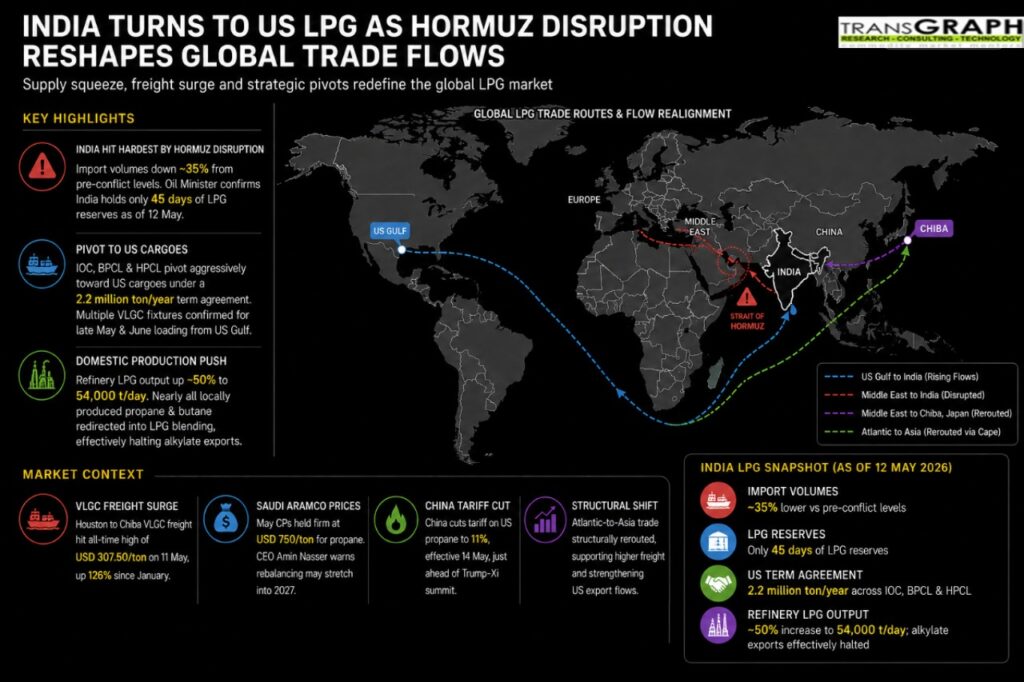

LPG Market Update - 21 May 2026

- Comments by Donald Trump indicating that US-Iran negotiations were in the “final stages” triggered a sharp correction in LPG markets. Propane at Mont Belvieu Enterprise (non-TET) declined from USD 413/ton to USD 384/ton, while butane fell from USD 625/ton to USD 543/ton.

- Despite the easing in crude and LPG prices, underlying market fundamentals remain firmly bullish. Global LPG balances continue to be constrained by severe logistical disruptions and limited vessel availability. The Strait of Hormuz remains heavily restricted, while congestion at the Panama Canal and continued security risks in the Red Sea are lengthening voyage durations and significantly increasing freight costs.

- India remains the most exposed major LPG importing market. The country is currently facing an estimated supply deficit of approximately 400,000 b/d, as import volumes remain substantially below pre-crisis levels despite domestic production operating close to capacity limits.