Impact Assessment of US/Israel-Iran Conflict

Impact Assessment of US/Israel-Iran Conflict

- The first day of the ceasefire showed limited progress, particularly in terms of tanker movement through the Strait of Hormuzon, on day 1 (08th Apr'26), with shipping intelligence firms reporting that 4 vessels crossed, all dry cargo carriers (including the Greek-owned bulk carrier NJ Earth and the Liberia-flagged Daytona Beach), and no oil tankers transiting the strait. Vessel traffic remained largely unchanged, which is not surprising given ongoing safety concerns. Shipowners are hesitant to resume operations due to continued threatening statements from the IRGC, along with the release of navigational advisories and maps warning about potential sea mines in the channel.

- Even if some of these threats are uncertain, the process of clearing mines and ensuring safe passage is time-consuming, even under stable conditions. As a result, the only viable short-term solution appears to be a potential arrangement where the US informally allows Iran to control passage, possibly through a toll-based system. Even under such a scenario, it is expected that Hormuz flows will remain significantly reduced for at least the next four weeks, with a risk of further prolonged disruption. Additionally, logistical challenges such as repositioning vessels, clearing storage, and restarting upstream and refining operations will take some time.

- Shipowners are also likely to remain cautious due to the risk of renewed conflict, especially depending on developments over the next couple of weeks. There are also concerns about the implications of making payments to sanctioned entities, which could increase pressure to relax sanctions on Iran, at least temporarily for maritime transit.

- At the same time, there are unconfirmed reports of fires near Saudi Arabia’s Abqaiq processing facility, along with confirmed attacks on the East–West pipeline, which was operating at emergency capacity of up to 7 MBpd before the attack. This raises concerns about the reliability of alternative export routes, particularly the Red Sea route via Yanbu, which is currently a key fallback option.

- Meanwhile, physical crude markets continue to strengthen, and paper markets are rebounding toward pre-ceasefire levels. There are also early signs of resource nationalism emerging in Europe, with companies like Galp reportedly considering limiting diesel exports to safeguard domestic supply are expected to support Diesel prices in near term.

Ten Negotiation terms set by Iran for ceasefire:

- US commitment to non-aggression — A guarantee of no further acts of aggression or attacks against Iran.

- Continued Iranian control over the Strait of Hormuz — Iran retains oversight and the ability to regulate passage (including potential fees or coordination with its armed forces).

- Acceptance of Iran's uranium enrichment rights — Formal recognition of Iran's nuclear enrichment program.

- Lifting of all primary US sanctions against Iran.

- Lifting of all secondary sanctions (affecting third countries dealing with Iran).

- Termination of all UN Security Council resolutions against Iran.

- Termination of all IAEA Board of Governors resolutions against Iran.

- Payment of compensation/damages to Iran for war losses and reconstruction.

- Withdrawal of US combat forces from the region (all bases and points of deployment).

- Cessation of the war on all fronts, including an end to attacks on Iran and its allies (such as in Lebanon against Hezbollah/"Islamic resistance").

- The government is considering releasing an additional 20 days’ worth of oil reserves as early as May'26 due to continued uncertainty around safe navigation through the Strait of Hormuz, even after the US–Iran ceasefire. Initial releases began in mid-Mar'26, totaling around 50 days’ worth of oil, with ongoing distribution from national reserves through Apr'26.

- Alongside stock releases, efforts are underway to secure alternative crude supplies from the US and via routes bypassing Hormuz. However, concerns remain, prompting discussions on possible fuel demand control measures.

- Iraq's state-run Basra Oil Company head, said that if the Iran war ends and the Strait of Hormuz reopens, Iraq could restore crude oil exports to around 3.4 MBpd within a week. However, Iraq has not received formal documents from Iran regarding permission for Iraqi tankers to pass through the Strait.

- Crude oil exports from Russia's Sheskharis terminal in Novorossiysk were suspended due to a drone attack and fire. The terminal typically loads 0.7 MBpd, adding strain to Russian infrastructure.

IEA member nations have agreed to a coordinated release of 400 mln bbl — the largest emergency SPR release since the IEA was founded after the 1973 Oil Crisis. The US, under the Trump administration, is contributing 172 mln bbl structured as loans to companies with repayment including a premium.

Deliveries are expected to begin reaching the market by the end of next week and will continue over approximately 120 days. The first batch of 86 mln bbl has already been opened for bidding. Japan will released 80 mln bbl beginning 16th Mar'26.

IEA Region-wise Release Breakdown

Key Supply Infrastructure

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Exchange of attacks between US/Israel and Iran continuing, leading to severe/significant/complete disruptions of crude oil and its products trade through the Strait of Hormuz, severely impacting Iraq's and Kuwait's crude oil production over the next 3 to 6 months. Full-year 2026 deficit: −1.90 MBpd. AMJ quarter most acute at −4.50 MBpd.

- Scenario 2 (Alternate): Partial disruptions of crude oil trade through the Strait of Hormuz, with Iran not targeting ships and oil tankers moving toward China, India, and select Asian nations outside the Western alliance. Full-year 2026 deficit: −1.35 MBpd. Balance returns to flat by OND '26.

- On the US front, US retail sales recorded a solid rebound in Feb'26, rising 0.6% MoM and 3.7% on YoY, marking the strongest gain in seven months, supported by a recovery in motor vehicle purchases and seasonal factors. Core retail sales also came in firm at 0.5% MoM, indicating underlying consumption strength, with higher tax refunds playing a key role in sustaining household spending during the period.

- The US manufacturing activity continued to expand, with ISM PMI rising to 52.7 in March, its highest level since Aug'22. That said, the improvement was partly driven by slower supplier deliveries, reflecting supply chain disruptions rather than demand strength, particularly amid shipping constraints and trade frictions. This has also led to a sharp rise in input cost pressures, with the prices paid index jumping significantly, signaling building inflation at the producer level.

Brent Crude 1M Futures are expected to trade in a range of 90 USD/bbl to 110 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

LPG Market Update

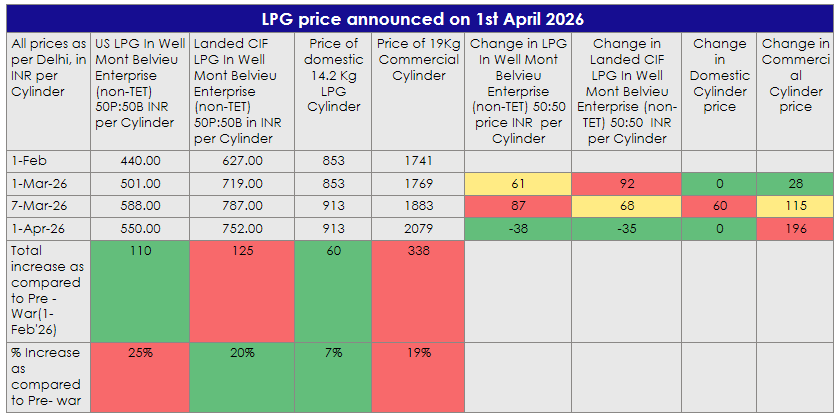

Commercial LPG Price Hike — 1st April 2026 (Delhi)

- Commercial LPG prices increased by ₹195.50 per 19-kg cylinder on April 1, 2026. A 19-kg cylinder now costs ₹2,078.50 in Delhi — up from ₹1,883 earlier.

- This is the second monthly increase, following a ₹114.50 rise in March. The hike affects restaurants, hotels, and small businesses. The adjustment indicates that prior increases in international prices, along with possible margin realignments, are still being passed through in the domestic market.

- In comparison, the 14.2 kg domestic LPG cylinder price has increased by only ₹60 (7%), with no change in the latest revision. This indicates a relatively controlled and stable pricing approach for household consumers, in contrast to the continued upward adjustments in the commercial segment.

- International LPG benchmarks have also seen increases over the period, with Mont Belvieu prices rising by ₹110 (25%) and Landed CIF prices by ₹125 (20%) on 1st Apr'26 as compared to 1st Feb'26. However, the magnitude of increase in commercial LPG prices, particularly in absolute terms, remains notably higher than that of domestic cylinders.

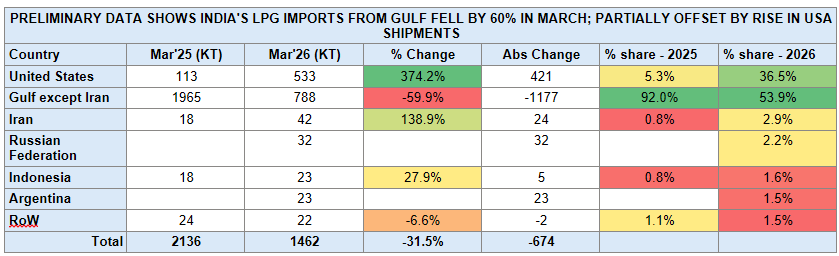

India’s LPG import slump in March'26 signals Gulf disruption impact, triggers strategic shift toward US supply

- India’s LPG import profile shifted sharply in March, with total volumes declining 31.5% MoM to 1,462 KT (down 674 KT), driven by a steep 59.9% drop in Gulf supplies (ex-Iran) to 788 KT (-1,177 KT), reducing their share from 92.0% to 53.9% amid disruptions around the Strait of Hormuz.

- This was partially offset by a surge in imports from the United States, which rose 374% MoM to 533 KT (+421 KT), lifting its share to 36.5%, alongside incremental volumes from Iran (42 KT, +139%), the Russian Federation (32 KT), Indonesia (23 KT, +27.9%), and Argentina (23 KT).

- Despite this rebalancing, the shift toward long-haul cargoes implies higher freight intensity and longer supply chains, reinforcing near-term tightness and upward pressure on delivered LPG costs.

India’s LPG balance under pressure as Hormuz disruptions persist, with vessel arrivals providing short-term supply relief

- India’s LPG supply–demand balance remains under near-term pressure amid geopolitical disruptions, with domestic demand estimated at 92.6–95.0 KT/day (~33 MMT annually), of which 55–60 KT/day (60–65%) is met through imports and ~35 KT/day from domestic production; notably, ~90% of imports transit through the Strait of Hormuz, creating significant exposure to ongoing disruptions.

- Recent vessel inflows have provided partial relief, with Hellas Gladiator (24 KT, Netherlands) and Gas Jupiter (24 KT, United States) having arrived on March 30 at Ennore Port and Visakhapatnam Port respectively, followed by BW TYR reaching Mumbai on March 31; BW ELM is expected to arrive at Mangaluru on April 1 after successfully transiting the Strait of Hormuz under Indian Navy escort as part of Operation Urja Suraksha.

- Earlier arrivals of Jag Vasant and Pine Gas (combined 92.6 KT; March 26–27) added roughly one day of national demand cover, along with the previously discharged Shivalik and Nanda Devi cargoes (92.5 KT; March 15–16) offering temporary relief despite persistent structural supply risks.

Impact Assessment of US/Israel-Iran Conflict

- WTI Crude May'26 futures and Brent Crude Jun'26 futures prices both fall by around 15% in early trade on 08th Apr'26 (Today) after the US President Trump announced a temporary ceasefire.

- A temporary ceasefire in the Iran war, agreed by US President Donald Trump, will provide relief to economies affected by the world's worst energy crisis. However, the deal's effectiveness remains uncertain, as Iran continued attacks on Israel and Gulf countries after the announcement.

- Around 187 laden tankers carrying nearly 172 mln bbl of crude oil and petroleum products are currently stranded in the Gulf since the war began, awaiting clearance through the Strait of Hormuz.

- Iran reportedly struck Saudi Arabia’s Jubail Industrial City, a major petrochemical hub with an estimated production capacity of approx. 60 mln tons per year, producing key downstream products such as plastics, fertilizers, industrial chemicals, and synthetic materials.

- The attack caused fires at parts of the complex, including facilities linked to major producers like SABIC, though the full extent of damage and operational disruption remains unclear.

- While Jubail is critical to Saudi Arabia’s industrial base and exports, there is no confirmation of large-scale destruction or immediate global supply disruption, with the situation still evolving.

- European and Asian refiners are paying record high prices of near 150 USD/bbl for some crude oil grades due to the US-Israel war with Iran, which has forced the shutdown of about 12% of world supply.

- Spot premiums for US West Texas Intermediate crude have surged to record highs (30 - 40 USD/bbl) due to increased competition between Asian and European refiners vying to replace Middle Eastern oil flows disrupted by the Iran war.

- Iraq's state-run Basra Oil Company head, said that if the Iran war ends and the Strait of Hormuz reopens, Iraq could restore crude oil exports to around 3.4 MBpd within a week. However, Iraq has not received formal documents from Iran regarding permission for Iraqi tankers to pass through the Strait.

- Crude oil exports from Russia's Sheskharis terminal in Novorossiysk were suspended due to a drone attack and fire. The terminal typically loads 0.7 MBpd, adding strain to Russian infrastructure.

- OPEC+ agreed to raise its oil output quotas by 0.21 MBpd for May'26, but the increase is largely symbolic as key members are unable to raise production due to the US-Israeli war with Iran.

IEA member nations have agreed to a coordinated release of 400 mln bbl — the largest emergency SPR release since the IEA was founded after the 1973 Oil Crisis. The US, under the Trump administration, is contributing 172 mln bbl structured as loans to companies with repayment including a premium.

Deliveries are expected to begin reaching the market by the end of next week and will continue over approximately 120 days. The first batch of 86 mln bbl has already been opened for bidding. Japan will released 80 mln bbl beginning 16th Mar'26.

IEA Region-wise Release Breakdown

Key Supply Infrastructure

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Exchange of attacks between US/Israel and Iran continuing, leading to severe/significant/complete disruptions of crude oil and its products trade through the Strait of Hormuz, severely impacting Iraq's and Kuwait's crude oil production over the next 3 to 6 months. Full-year 2026 deficit: −1.90 MBpd. AMJ quarter most acute at −4.50 MBpd.

- Scenario 2 (Alternate): Partial disruptions of crude oil trade through the Strait of Hormuz, with Iran not targeting ships and oil tankers moving toward China, India, and select Asian nations outside the Western alliance. Full-year 2026 deficit: −1.35 MBpd. Balance returns to flat by OND '26.

- On the US front, US retail sales recorded a solid rebound in Feb'26, rising 0.6% MoM and 3.7% on YoY, marking the strongest gain in seven months, supported by a recovery in motor vehicle purchases and seasonal factors. Core retail sales also came in firm at 0.5% MoM, indicating underlying consumption strength, with higher tax refunds playing a key role in sustaining household spending during the period.

- The US manufacturing activity continued to expand, with ISM PMI rising to 52.7 in March, its highest level since Aug'22. That said, the improvement was partly driven by slower supplier deliveries, reflecting supply chain disruptions rather than demand strength, particularly amid shipping constraints and trade frictions. This has also led to a sharp rise in input cost pressures, with the prices paid index jumping significantly, signaling building inflation at the producer level.

Brent Crude 1M Futures are expected to trade in a range of 90 USD/bbl to 120 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

LPG Market Update

Commercial LPG Price Hike — 1st April 2026 (Delhi)

- Commercial LPG prices increased by ₹195.50 per 19-kg cylinder on April 1, 2026. A 19-kg cylinder now costs ₹2,078.50 in Delhi — up from ₹1,883 earlier.

- This is the second monthly increase, following a ₹114.50 rise in March. The hike affects restaurants, hotels, and small businesses. The adjustment indicates that prior increases in international prices, along with possible margin realignments, are still being passed through in the domestic market.

- In comparison, the 14.2 kg domestic LPG cylinder price has increased by only ₹60 (7%), with no change in the latest revision. This indicates a relatively controlled and stable pricing approach for household consumers, in contrast to the continued upward adjustments in the commercial segment.

- International LPG benchmarks have also seen increases over the period, with Mont Belvieu prices rising by ₹110 (25%) and Landed CIF prices by ₹125 (20%) on 1st Apr'26 as compared to 1st Feb'26. However, the magnitude of increase in commercial LPG prices, particularly in absolute terms, remains notably higher than that of domestic cylinders.

India’s LPG import slump in March'26 signals Gulf disruption impact, triggers strategic shift toward US supply

- India’s LPG import profile shifted sharply in March, with total volumes declining 31.5% MoM to 1,462 KT (down 674 KT), driven by a steep 59.9% drop in Gulf supplies (ex-Iran) to 788 KT (-1,177 KT), reducing their share from 92.0% to 53.9% amid disruptions around the Strait of Hormuz.

- This was partially offset by a surge in imports from the United States, which rose 374% MoM to 533 KT (+421 KT), lifting its share to 36.5%, alongside incremental volumes from Iran (42 KT, +139%), the Russian Federation (32 KT), Indonesia (23 KT, +27.9%), and Argentina (23 KT).

- Despite this rebalancing, the shift toward long-haul cargoes implies higher freight intensity and longer supply chains, reinforcing near-term tightness and upward pressure on delivered LPG costs.

India’s LPG balance under pressure as Hormuz disruptions persist, with vessel arrivals providing short-term supply relief

- India’s LPG supply–demand balance remains under near-term pressure amid geopolitical disruptions, with domestic demand estimated at 92.6–95.0 KT/day (~33 MMT annually), of which 55–60 KT/day (60–65%) is met through imports and ~35 KT/day from domestic production; notably, ~90% of imports transit through the Strait of Hormuz, creating significant exposure to ongoing disruptions.

- Recent vessel inflows have provided partial relief, with Hellas Gladiator (24 KT, Netherlands) and Gas Jupiter (24 KT, United States) having arrived on March 30 at Ennore Port and Visakhapatnam Port respectively, followed by BW TYR reaching Mumbai on March 31; BW ELM is expected to arrive at Mangaluru on April 1 after successfully transiting the Strait of Hormuz under Indian Navy escort as part of Operation Urja Suraksha.

- Earlier arrivals of Jag Vasant and Pine Gas (combined 92.6 KT; March 26–27) added roughly one day of national demand cover, along with the previously discharged Shivalik and Nanda Devi cargoes (92.5 KT; March 15–16) offering temporary relief despite persistent structural supply risks.

Impact Assessment of US/Israel-Iran Conflict

- Iran rejected a US proposal for an immediate ceasefire and the lifting of its effective blockade of the Strait of Hormuz, followed by talks on a broader peace settlement within 15 to 20 days.

- Trump vowed to destroy Iranian power plants and infrastructure if Tehran refused to agree before the deadline.

- Saudi Arabia intercepted ballistic missiles towards its eastern region with debris falling near energy facilities.

- Iraq's state-run Basra Oil Company head, said that if the Iran war ends and the Strait of Hormuz reopens, Iraq could restore crude oil exports to around 3.4 MBpd within a week. However, Iraq has not received formal documents from Iran regarding permission for Iraqi tankers to pass through the Strait.

- Spot premiums for US West Texas Intermediate crude have surged to record highs (30 - 40 USD/bbl) due to increased competition between Asian and European refiners vying to replace Middle Eastern oil flows disrupted by the Iran war.

- Russia accused Ukraine of attacking the Caspian Pipeline Consortium's Black Sea terminal, which handles 1.5% of global oil supply, damaging the single point mooring, loading infrastructure and four vast storage tanks.

- Russian oil output cuts are imminent due to Ukraine's strikes on port infrastructure, pipelines, and refineries, reducing export capability by 1 MBpd. This would add to global supply strain, as Ukraine targets Russia's oil export infrastructure. At least 20% of Russia's export capacity is out of order, impacting Russian oil production.

- OPEC+ agreed to raise its oil output quotas by 0.21 MBpd for May'26, but the increase is largely symbolic as key members are unable to raise production due to the US-Israeli war with Iran.

IEA member nations have agreed to a coordinated release of 400 mln bbl — the largest emergency SPR release since the IEA was founded after the 1973 Oil Crisis. The US, under the Trump administration, is contributing 172 mln bbl structured as loans to companies with repayment including a premium.

Deliveries are expected to begin reaching the market by the end of next week and will continue over approximately 120 days. The first batch of 86 mln bbl has already been opened for bidding. Japan will released 80 mln bbl beginning 16th Mar'26.

IEA Region-wise Release Breakdown

Key Supply Infrastructure

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Exchange of attacks between US/Israel and Iran continuing, leading to severe/significant/complete disruptions of crude oil and its products trade through the Strait of Hormuz, severely impacting Iraq's and Kuwait's crude oil production over the next 3 to 6 months. Full-year 2026 deficit: −1.90 MBpd. AMJ quarter most acute at −4.50 MBpd.

- Scenario 2 (Alternate): Partial disruptions of crude oil trade through the Strait of Hormuz, with Iran not targeting ships and oil tankers moving toward China, India, and select Asian nations outside the Western alliance. Full-year 2026 deficit: −1.35 MBpd. Balance returns to flat by OND '26.

- The US Dollar Index edged lower in Wednesday’s session, declining from 99.96 to 99.65 level, retreating recently from its 10-month high. The index registered a daily loss of 0.31%, while holding a flat on a weekly basis.

- The pullback was primarily driven by weaker than expected JOLTS data, which signaled cooling labor demand, along with a decline in U S Treasury yields, reducing support for the dollar and prompting mild unwinding of long positions.

- On the US front, US retail sales recorded a solid rebound in Feb'26, rising 0.6% MoM and 3.7% on YoY, marking the strongest gain in seven months, supported by a recovery in motor vehicle purchases and seasonal factors. Core retail sales also came in firm at 0.5% MoM, indicating underlying consumption strength, with higher tax refunds playing a key role in sustaining household spending during the period.

- The US manufacturing activity continued to expand, with ISM PMI rising to 52.7 in March, its highest level since Aug'22. That said, the improvement was partly driven by slower supplier deliveries, reflecting supply chain disruptions rather than demand strength, particularly amid shipping constraints and trade frictions. This has also led to a sharp rise in input cost pressures, with the prices paid index jumping significantly, signaling building inflation at the producer level.

Brent Crude 1M Futures are expected to trade in a range of 90 USD/bbl to 120 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

LPG Market Update

Commercial LPG Price Hike — 1st April 2026 (Delhi)

- Commercial LPG prices increased by ₹195.50 per 19-kg cylinder on April 1, 2026. A 19-kg cylinder now costs ₹2,078.50 in Delhi — up from ₹1,883 earlier.

- This is the second monthly increase, following a ₹114.50 rise in March. The hike affects restaurants, hotels, and small businesses. The adjustment indicates that prior increases in international prices, along with possible margin realignments, are still being passed through in the domestic market.

- In comparison, the 14.2 kg domestic LPG cylinder price has increased by only ₹60 (7%), with no change in the latest revision. This indicates a relatively controlled and stable pricing approach for household consumers, in contrast to the continued upward adjustments in the commercial segment.

- International LPG benchmarks have also seen increases over the period, with Mont Belvieu prices rising by ₹110 (25%) and Landed CIF prices by ₹125 (20%) on 1st Apr'26 as compared to 1st Feb'26. However, the magnitude of increase in commercial LPG prices, particularly in absolute terms, remains notably higher than that of domestic cylinders.

India’s LPG import slump in March'26 signals Gulf disruption impact, triggers strategic shift toward US supply

- India’s LPG import profile shifted sharply in March, with total volumes declining 31.5% MoM to 1,462 KT (down 674 KT), driven by a steep 59.9% drop in Gulf supplies (ex-Iran) to 788 KT (-1,177 KT), reducing their share from 92.0% to 53.9% amid disruptions around the Strait of Hormuz.

- This was partially offset by a surge in imports from the United States, which rose 374% MoM to 533 KT (+421 KT), lifting its share to 36.5%, alongside incremental volumes from Iran (42 KT, +139%), the Russian Federation (32 KT), Indonesia (23 KT, +27.9%), and Argentina (23 KT).

- Despite this rebalancing, the shift toward long-haul cargoes implies higher freight intensity and longer supply chains, reinforcing near-term tightness and upward pressure on delivered LPG costs.

India’s LPG balance under pressure as Hormuz disruptions persist, with vessel arrivals providing short-term supply relief

- India’s LPG supply–demand balance remains under near-term pressure amid geopolitical disruptions, with domestic demand estimated at 92.6–95.0 KT/day (~33 MMT annually), of which 55–60 KT/day (60–65%) is met through imports and ~35 KT/day from domestic production; notably, ~90% of imports transit through the Strait of Hormuz, creating significant exposure to ongoing disruptions.

- Recent vessel inflows have provided partial relief, with Hellas Gladiator (24 KT, Netherlands) and Gas Jupiter (24 KT, United States) having arrived on March 30 at Ennore Port and Visakhapatnam Port respectively, followed by BW TYR reaching Mumbai on March 31; BW ELM is expected to arrive at Mangaluru on April 1 after successfully transiting the Strait of Hormuz under Indian Navy escort as part of Operation Urja Suraksha.

- Earlier arrivals of Jag Vasant and Pine Gas (combined 92.6 KT; March 26–27) added roughly one day of national demand cover, along with the previously discharged Shivalik and Nanda Devi cargoes (92.5 KT; March 15–16) offering temporary relief despite persistent structural supply risks.

Impact Assessment of US/Israel-Iran Conflict

- OPEC+ agreed to raise its oil output quotas by 0.21 MBpd for May'26, but the increase is largely symbolic as key members are unable to raise production due to the US-Israeli war with Iran.

- Iraq's state oil marketer SOMO asked customers to submit crude oil lifting schedules within 24 hours, following media reports that Iran has exempted Iraq from any restrictions on transit through the Strait of Hormuz.

- Russian oil output cuts are imminent due to Ukraine's strikes on port infrastructure, pipelines, and refineries, reducing export capability by 1 MBpd. This would add to global supply strain, as Ukraine targets Russia's oil export infrastructure. At least 20% of Russia's export capacity is out of order, impacting Russian oil production.

- The US President Trump defended his handling of the US/Israeli-Iran war on Iran in a prime time address, saying the US military was nearing completion of its mission while also reinforcing his threats to bomb the Islamic Republic back to the Stone Age.

- Trump stopped short of offering a firm timeline for an end to hostilities and suggested the war could escalate if Iranian leaders did not capitulate to US terms during negotiations.

- The US oil rig counts (Baker Hughes), a key indicator of future production, increased by two to 411 rigs this week. Higher forward oil prices are encouraging producers to consider adding more rigs.

IEA member nations have agreed to a coordinated release of 400 mln bbl — the largest emergency SPR release since the IEA was founded after the 1973 Oil Crisis. The US, under the Trump administration, is contributing 172 mln bbl structured as loans to companies with repayment including a premium.

Deliveries are expected to begin reaching the market by the end of next week and will continue over approximately 120 days. The first batch of 86 mln bbl has already been opened for bidding. Japan will released 80 mln bbl beginning 16th Mar'26.

IEA Region-wise Release Breakdown

Key Supply Infrastructure

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Exchange of attacks between US/Israel and Iran continuing, leading to severe/significant/complete disruptions of crude oil and its products trade through the Strait of Hormuz, severely impacting Iraq's and Kuwait's crude oil production over the next 3 to 6 months. Full-year 2026 deficit: −1.90 MBpd. AMJ quarter most acute at −4.50 MBpd.

- Scenario 2 (Alternate): Partial disruptions of crude oil trade through the Strait of Hormuz, with Iran not targeting ships and oil tankers moving toward China, India, and select Asian nations outside the Western alliance. Full-year 2026 deficit: −1.35 MBpd. Balance returns to flat by OND '26.

- The US Dollar Index edged lower in Wednesday’s session, declining from 99.96 to 99.65 level, retreating recently from its 10-month high. The index registered a daily loss of 0.31%, while holding a flat on a weekly basis.

- The pullback was primarily driven by weaker than expected JOLTS data, which signaled cooling labor demand, along with a decline in U S Treasury yields, reducing support for the dollar and prompting mild unwinding of long positions.

- On the US front, US retail sales recorded a solid rebound in Feb'26, rising 0.6% MoM and 3.7% on YoY, marking the strongest gain in seven months, supported by a recovery in motor vehicle purchases and seasonal factors. Core retail sales also came in firm at 0.5% MoM, indicating underlying consumption strength, with higher tax refunds playing a key role in sustaining household spending during the period.

- The US manufacturing activity continued to expand, with ISM PMI rising to 52.7 in March, its highest level since Aug'22. That said, the improvement was partly driven by slower supplier deliveries, reflecting supply chain disruptions rather than demand strength, particularly amid shipping constraints and trade frictions. This has also led to a sharp rise in input cost pressures, with the prices paid index jumping significantly, signaling building inflation at the producer level.

Brent Crude 1M Futures are expected to trade in a range of 90 USD/bbl to 120 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

LPG Market Update

Commercial LPG Price Hike — 1st April 2026 (Delhi)

- Commercial LPG prices increased by ₹195.50 per 19-kg cylinder on April 1, 2026. A 19-kg cylinder now costs ₹2,078.50 in Delhi — up from ₹1,883 earlier.

- This is the second monthly increase, following a ₹114.50 rise in March. The hike affects restaurants, hotels, and small businesses. The adjustment indicates that prior increases in international prices, along with possible margin realignments, are still being passed through in the domestic market.

- In comparison, the 14.2 kg domestic LPG cylinder price has increased by only ₹60 (7%), with no change in the latest revision. This indicates a relatively controlled and stable pricing approach for household consumers, in contrast to the continued upward adjustments in the commercial segment.

- International LPG benchmarks have also seen increases over the period, with Mont Belvieu prices rising by ₹110 (25%) and Landed CIF prices by ₹125 (20%) on 1st Apr'26 as compared to 1st Feb'26. However, the magnitude of increase in commercial LPG prices, particularly in absolute terms, remains notably higher than that of domestic cylinders.

India’s LPG import slump in March'26 signals Gulf disruption impact, triggers strategic shift toward US supply

- India’s LPG import profile shifted sharply in March, with total volumes declining 31.5% MoM to 1,462 KT (down 674 KT), driven by a steep 59.9% drop in Gulf supplies (ex-Iran) to 788 KT (-1,177 KT), reducing their share from 92.0% to 53.9% amid disruptions around the Strait of Hormuz.

- This was partially offset by a surge in imports from the United States, which rose 374% MoM to 533 KT (+421 KT), lifting its share to 36.5%, alongside incremental volumes from Iran (42 KT, +139%), the Russian Federation (32 KT), Indonesia (23 KT, +27.9%), and Argentina (23 KT).

- Despite this rebalancing, the shift toward long-haul cargoes implies higher freight intensity and longer supply chains, reinforcing near-term tightness and upward pressure on delivered LPG costs.

India’s LPG balance under pressure as Hormuz disruptions persist, with vessel arrivals providing short-term supply relief

- India’s LPG supply–demand balance remains under near-term pressure amid geopolitical disruptions, with domestic demand estimated at 92.6–95.0 KT/day (~33 MMT annually), of which 55–60 KT/day (60–65%) is met through imports and ~35 KT/day from domestic production; notably, ~90% of imports transit through the Strait of Hormuz, creating significant exposure to ongoing disruptions.

- Recent vessel inflows have provided partial relief, with Hellas Gladiator (24 KT, Netherlands) and Gas Jupiter (24 KT, United States) having arrived on March 30 at Ennore Port and Visakhapatnam Port respectively, followed by BW TYR reaching Mumbai on March 31; BW ELM is expected to arrive at Mangaluru on April 1 after successfully transiting the Strait of Hormuz under Indian Navy escort as part of Operation Urja Suraksha.

- Earlier arrivals of Jag Vasant and Pine Gas (combined 92.6 KT; March 26–27) added roughly one day of national demand cover, along with the previously discharged Shivalik and Nanda Devi cargoes (92.5 KT; March 15–16) offering temporary relief despite persistent structural supply risks.

Impact Assessment of US/Israel-Iran Conflict

- WTI Crude May'26 futures and Brent Crude Jun'26 futures prices rose by 11.4% and 7.8% to 111.54 USD/bbl and 109.03 USD/bbl respectively on yesterday's session on the account of concerns over prolonged disruptions to oil supply following President Donald Trump's announcement of continued US attacks on Iran.

- Russian oil output cuts are imminent due to Ukraine's strikes on port infrastructure, pipelines, and refineries, reducing export capability by 1 MBpd. This would add to global supply strain, as Ukraine targets Russia's oil export infrastructure. At least 20% of Russia's export capacity is out of order, impacting Russian oil production.

- The US President Trump defended his handling of the US/Israeli-Iran war on Iran in a prime time address, saying the US military was nearing completion of its mission while also reinforcing his threats to bomb the Islamic Republic back to the Stone Age.

- Trump stopped short of offering a firm timeline for an end to hostilities and suggested the war could escalate if Iranian leaders did not capitulate to US terms during negotiations.

- The US crude oil output fell by 0.41 MBpd in Jan'26, the most in two years, due to a severe winter storm that disrupted production. Gasoline demand fell sharply during January's winter storms, while distillate fuel consumption surged as unusually low temperatures increased consumption for power generation and space heating.

- The US Gulf Coast refiners imported the most crude oil from Venezuela since Mar'25 in Jan'26. Moreover, the total US imports rising to 6.2 MBpd from 3.8 MBpd in Dec'25.

- Venezuela's oil exports surpassed 1 MBpd in Mar'26 for the first time since Sep'25, driven by sales to refiners in India and shipments by trading houses to the Caribbean for storage.

- Oil tanker availability along the US Gulf Coast has dropped sharply due to Asian and European refiners, who are unable to access Middle Eastern supply, buying vessels to import oil and fuel from the US.

IEA member nations have agreed to a coordinated release of 400 mln bbl — the largest emergency SPR release since the IEA was founded after the 1973 Oil Crisis. The US, under the Trump administration, is contributing 172 mln bbl structured as loans to companies with repayment including a premium.

Deliveries are expected to begin reaching the market by the end of next week and will continue over approximately 120 days. The first batch of 86 mln bbl has already been opened for bidding. Japan will released 80 mln bbl beginning 16th Mar'26.

IEA Region-wise Release Breakdown

Key Supply Infrastructure

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Exchange of attacks between US/Israel and Iran continuing, leading to severe/significant/complete disruptions of crude oil and its products trade through the Strait of Hormuz, severely impacting Iraq's and Kuwait's crude oil production over the next 3 to 6 months. Full-year 2026 deficit: −1.90 MBpd. AMJ quarter most acute at −4.50 MBpd.

- Scenario 2 (Alternate): Partial disruptions of crude oil trade through the Strait of Hormuz, with Iran not targeting ships and oil tankers moving toward China, India, and select Asian nations outside the Western alliance. Full-year 2026 deficit: −1.35 MBpd. Balance returns to flat by OND '26.

- The US Dollar Index edged lower in Wednesday’s session, declining from 99.96 to 99.65 level, retreating recently from its 10-month high. The index registered a daily loss of 0.31%, while holding a flat on a weekly basis.

- The pullback was primarily driven by weaker than expected JOLTS data, which signaled cooling labor demand, along with a decline in U S Treasury yields, reducing support for the dollar and prompting mild unwinding of long positions.

- On the US front, US retail sales recorded a solid rebound in Feb'26, rising 0.6% MoM and 3.7% on YoY, marking the strongest gain in seven months, supported by a recovery in motor vehicle purchases and seasonal factors. Core retail sales also came in firm at 0.5% MoM, indicating underlying consumption strength, with higher tax refunds playing a key role in sustaining household spending during the period.

- The US manufacturing activity continued to expand, with ISM PMI rising to 52.7 in March, its highest level since Aug'22. That said, the improvement was partly driven by slower supplier deliveries, reflecting supply chain disruptions rather than demand strength, particularly amid shipping constraints and trade frictions. This has also led to a sharp rise in input cost pressures, with the prices paid index jumping significantly, signaling building inflation at the producer level.

Brent Expected to Trade 90–120 USD/bbl

Brent Crude 1M Futures are expected to trade in a range of 90 USD/bbl to 120 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

LPG Market Update

Commercial LPG Price Hike — 1st April 2026 (Delhi)

- Commercial LPG prices increased by ₹195.50 per 19-kg cylinder on April 1, 2026. A 19-kg cylinder now costs ₹2,078.50 in Delhi — up from ₹1,883 earlier.

- This is the second monthly increase, following a ₹114.50 rise in March. The hike affects restaurants, hotels, and small businesses. The adjustment indicates that prior increases in international prices, along with possible margin realignments, are still being passed through in the domestic market.

- In comparison, the 14.2 kg domestic LPG cylinder price has increased by only ₹60 (7%), with no change in the latest revision. This indicates a relatively controlled and stable pricing approach for household consumers, in contrast to the continued upward adjustments in the commercial segment.

- International LPG benchmarks have also seen increases over the period, with Mont Belvieu prices rising by ₹110 (25%) and Landed CIF prices by ₹125 (20%) on 1st Apr'26 as compared to 1st Feb'26. However, the magnitude of increase in commercial LPG prices, particularly in absolute terms, remains notably higher than that of domestic cylinders.

India’s LPG import slump in March'26 signals Gulf disruption impact, triggers strategic shift toward US supply

- India’s LPG import profile shifted sharply in March, with total volumes declining 31.5% MoM to 1,462 KT (down 674 KT), driven by a steep 59.9% drop in Gulf supplies (ex-Iran) to 788 KT (-1,177 KT), reducing their share from 92.0% to 53.9% amid disruptions around the Strait of Hormuz.

- This was partially offset by a surge in imports from the United States, which rose 374% MoM to 533 KT (+421 KT), lifting its share to 36.5%, alongside incremental volumes from Iran (42 KT, +139%), the Russian Federation (32 KT), Indonesia (23 KT, +27.9%), and Argentina (23 KT).

- Despite this rebalancing, the shift toward long-haul cargoes implies higher freight intensity and longer supply chains, reinforcing near-term tightness and upward pressure on delivered LPG costs.

India’s LPG balance under pressure as Hormuz disruptions persist, with vessel arrivals providing short-term supply relief

- India’s LPG supply–demand balance remains under near-term pressure amid geopolitical disruptions, with domestic demand estimated at 92.6–95.0 KT/day (~33 MMT annually), of which 55–60 KT/day (60–65%) is met through imports and ~35 KT/day from domestic production; notably, ~90% of imports transit through the Strait of Hormuz, creating significant exposure to ongoing disruptions.

- Recent vessel inflows have provided partial relief, with Hellas Gladiator (24 KT, Netherlands) and Gas Jupiter (24 KT, United States) having arrived on March 30 at Ennore Port and Visakhapatnam Port respectively, followed by BW TYR reaching Mumbai on March 31; BW ELM is expected to arrive at Mangaluru on April 1 after successfully transiting the Strait of Hormuz under Indian Navy escort as part of Operation Urja Suraksha.

- Earlier arrivals of Jag Vasant and Pine Gas (combined 92.6 KT; March 26–27) added roughly one day of national demand cover, along with the previously discharged Shivalik and Nanda Devi cargoes (92.5 KT; March 15–16) offering temporary relief despite persistent structural supply risks.

Impact Assessment of US/Israel-Iran Conflict

- On 02nd Apr'26 (today) Brent and WTI 1M futures rose by 6.5% and 5.3% to 107.49 USD/bbl and 105.40 USD/bbl in intraday session on account after the US President Trump said the US would continue attacks on Iran without committing to a specific timeline to end the war.

- The US President Trump defended his handling of the US/Israeli-Iran war on Iran in a prime time address, saying the US military was nearing completion of its mission while also reinforcing his threats to bomb the Islamic Republic back to the Stone Age.

- Trump stopped short of offering a firm timeline for an end to hostilities and suggested the war could escalate if Iranian leaders did not capitulate to US terms during negotiations.

- The US crude oil output fell by 0.41 MBpd in Jan'26, the most in two years, due to a severe winter storm that disrupted production. Gasoline demand fell sharply during January's winter storms, while distillate fuel consumption surged as unusually low temperatures increased consumption for power generation and space heating.

- The US Gulf Coast refiners imported the most crude oil from Venezuela since Mar'25 in Jan'26, with imports rising to 6.2 MBpd from 3.8 MBpd in Dec'25.

- Market grapevine indicates that OPEC oil output plummeted in Mar'26 to its lowest level since Jun'20 due to the US/Israeli-Iran war, which effectively closed the Strait of Hormuz and forced export cuts.

- Crude output by OPEC members fell by 7.3 MBpd to 21.57 MBpd, led by cuts in Kuwait, Iraq, Saudi Arabia, and UAE.

- Venezuela's oil exports surpassed 1 MBpd in Mar'26 for the first time since Sep'25, driven by sales to refiners in India and shipments by trading houses to the Caribbean for storage.

- Oil tanker availability along the US Gulf Coast has dropped sharply due to Asian and European refiners, who are unable to access Middle Eastern supply, buying vessels to import oil and fuel from the US.

IEA member nations have agreed to a coordinated release of 400 mln bbl — the largest emergency SPR release since the IEA was founded after the 1973 Oil Crisis. The US, under the Trump administration, is contributing 172 mln bbl structured as loans to companies with repayment including a premium.

Deliveries are expected to begin reaching the market by the end of next week and will continue over approximately 120 days. The first batch of 86 mln bbl has already been opened for bidding. Japan will released 80 mln bbl beginning 16th Mar'26.

IEA Region-wise Release Breakdown

Key Supply Infrastructure

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Exchange of attacks between US/Israel and Iran continuing, leading to severe/significant/complete disruptions of crude oil and its products trade through the Strait of Hormuz, severely impacting Iraq's and Kuwait's crude oil production over the next 3 to 6 months. Full-year 2026 deficit: −1.90 MBpd. AMJ quarter most acute at −4.50 MBpd.

- Scenario 2 (Alternate): Partial disruptions of crude oil trade through the Strait of Hormuz, with Iran not targeting ships and oil tankers moving toward China, India, and select Asian nations outside the Western alliance. Full-year 2026 deficit: −1.35 MBpd. Balance returns to flat by OND '26.

- The US Dollar Index edged lower in Wednesday’s session, declining from 99.96 to 99.65 level, retreating recently from its 10-month high. The index registered a daily loss of 0.31%, while holding a flat on a weekly basis.

- The pullback was primarily driven by weaker than expected JOLTS data, which signaled cooling labor demand, along with a decline in U S Treasury yields, reducing support for the dollar and prompting mild unwinding of long positions.

- On the US front, US retail sales recorded a solid rebound in Feb'26, rising 0.6% MoM and 3.7% on YoY, marking the strongest gain in seven months, supported by a recovery in motor vehicle purchases and seasonal factors. Core retail sales also came in firm at 0.5% MoM, indicating underlying consumption strength, with higher tax refunds playing a key role in sustaining household spending during the period.

- The US manufacturing activity continued to expand, with ISM PMI rising to 52.7 in March, its highest level since Aug'22. That said, the improvement was partly driven by slower supplier deliveries, reflecting supply chain disruptions rather than demand strength, particularly amid shipping constraints and trade frictions. This has also led to a sharp rise in input cost pressures, with the prices paid index jumping significantly, signaling building inflation at the producer level.

Brent Expected to Trade 90–120 USD/bbl

Brent Crude 1M Futures are expected to trade in a range of 90 USD/bbl to 120 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

LPG Market Update

Commercial LPG Price Hike — 1st April 2026 (Delhi)

- Commercial LPG prices increased by ₹195.50 per 19-kg cylinder on April 1, 2026. A 19-kg cylinder now costs ₹2,078.50 in Delhi — up from ₹1,883 earlier.

- This is the second monthly increase, following a ₹114.50 rise in March. The hike affects restaurants, hotels, and small businesses. The adjustment indicates that prior increases in international prices, along with possible margin realignments, are still being passed through in the domestic market.

- In comparison, the 14.2 kg domestic LPG cylinder price has increased by only ₹60 (7%), with no change in the latest revision. This indicates a relatively controlled and stable pricing approach for household consumers, in contrast to the continued upward adjustments in the commercial segment.

- International LPG benchmarks have also seen increases over the period, with Mont Belvieu prices rising by ₹110 (25%) and Landed CIF prices by ₹125 (20%) on 1st Apr'26 as compared to 1st Feb'26. However, the magnitude of increase in commercial LPG prices, particularly in absolute terms, remains notably higher than that of domestic cylinders.

India’s LPG import slump in March'26 signals Gulf disruption impact, triggers strategic shift toward US supply

- India’s LPG import profile shifted sharply in March, with total volumes declining 31.5% MoM to 1,462 KT (down 674 KT), driven by a steep 59.9% drop in Gulf supplies (ex-Iran) to 788 KT (-1,177 KT), reducing their share from 92.0% to 53.9% amid disruptions around the Strait of Hormuz.

- This was partially offset by a surge in imports from the United States, which rose 374% MoM to 533 KT (+421 KT), lifting its share to 36.5%, alongside incremental volumes from Iran (42 KT, +139%), the Russian Federation (32 KT), Indonesia (23 KT, +27.9%), and Argentina (23 KT).

- Despite this rebalancing, the shift toward long-haul cargoes implies higher freight intensity and longer supply chains, reinforcing near-term tightness and upward pressure on delivered LPG costs.

India’s LPG balance under pressure as Hormuz disruptions persist, with vessel arrivals providing short-term supply relief

- India’s LPG supply–demand balance remains under near-term pressure amid geopolitical disruptions, with domestic demand estimated at 92.6–95.0 KT/day (~33 MMT annually), of which 55–60 KT/day (60–65%) is met through imports and ~35 KT/day from domestic production; notably, ~90% of imports transit through the Strait of Hormuz, creating significant exposure to ongoing disruptions.

- Recent vessel inflows have provided partial relief, with Hellas Gladiator (24 KT, Netherlands) and Gas Jupiter (24 KT, United States) having arrived on March 30 at Ennore Port and Visakhapatnam Port respectively, followed by BW TYR reaching Mumbai on March 31; BW ELM is expected to arrive at Mangaluru on April 1 after successfully transiting the Strait of Hormuz under Indian Navy escort as part of Operation Urja Suraksha.

- Earlier arrivals of Jag Vasant and Pine Gas (combined 92.6 KT; March 26–27) added roughly one day of national demand cover, along with the previously discharged Shivalik and Nanda Devi cargoes (92.5 KT; March 15–16) offering temporary relief despite persistent structural supply risks.

Impact Assessment of US/Israel-Iran Conflict

- The US crude oil output fell by 0.41 MBpd in Jan'26, the most in two years, due to a severe winter storm that disrupted production. Gasoline demand fell sharply during January's winter storms, while distillate fuel consumption surged as unusually low temperatures increased consumption for power generation and space heating.

- The US Gulf Coast refiners imported the most crude oil from Venezuela since Mar'25 in Jan'26, with imports rising to 6.2 MBpd from 3.8 MBpd in Dec'25.

- Market grapevine indicates that OPEC oil output plummeted in Mar'26 to its lowest level since Jun'20 due to the US/Israeli-Iran war, which effectively closed the Strait of Hormuz and forced export cuts.

- Crude output by OPEC members fell by 7.3 MBpd to 21.57 MBpd, led by cuts in Kuwait, Iraq, Saudi Arabia, and UAE.

- Ukrainian drones have targeted Russia's Baltic Sea port of Ust-Luga five times in the past 10 days, with industry sources telling Reuters that an oil loading terminal was hit.

- This follows a series of attacks on Russia's oil export infrastructure, with at least 40% of its export capacity halted due to drone strikes and other disruptions.

- Crude oil production resumed at Libya's Sharara and El Feel oilfields after completing maintenance on a crude export pipeline. The fields had been shut down due to pipeline damage and a suspension in operations.

- Sharara is one of Libya's largest production areas, with a capacity of between 0.30and 0.32 MBpd.

IEA member nations have agreed to a coordinated release of 400 mln bbl — the largest emergency SPR release since the IEA was founded after the 1973 Oil Crisis. The US, under the Trump administration, is contributing 172 mln bbl structured as loans to companies with repayment including a premium.

Deliveries are expected to begin reaching the market by the end of next week and will continue over approximately 120 days. The first batch of 86 mln bbl has already been opened for bidding. Japan will release 80 mln bbl beginning 16th Mar'26.

IEA Region-wise Release Breakdown — As of 15 Mar 2026

Key Supply Infrastructure

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026; AMJ Quarter Most Severe

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Exchange of attacks between US/Israel and Iran continuing, leading to severe/significant/complete disruptions of crude oil and its products trade through the Strait of Hormuz, severely impacting Iraq's and Kuwait's crude oil production over the next 3 to 6 months. Full-year 2026 deficit: −1.90 MBpd. AMJ quarter most acute at −4.50 MBpd.

- Scenario 2 (Alternate): Partial disruptions of crude oil trade through the Strait of Hormuz, with Iran not targeting ships and oil tankers moving toward China, India, and select Asian nations outside the Western alliance. Full-year 2026 deficit: −1.35 MBpd. Balance returns to flat by OND '26.

- The US Dollar Index edged higher in yesterday's session, rising from 100.15 to 100.50 level, trading near a 10-month high. The index recorded a daily gain of 0.36% and advanced 1.58% on a weekly basis.

- The upward move was primarily supported by safe-haven demand amid escalating geopolitical tensions in the Middle East, particularly the ongoing Iran–Israel conflict, which weighed on global risk sentiment and drove capital flows toward the dollar.

- On the US front, US weekly jobless claims show a stable labor market with limited layoffs, despite macro risks from Middle East tensions and trade uncertainty. Initial claims rose modestly by 5K to 210K, in line with expectations, while continuing claims fell 32K to 1.819M, the lowest in nearly two years, indicating steady absorption of unemployed workers.

- The labor market remains in a “low-hire, low-fire” phase, though rising oil prices, tariff uncertainty, and tightening labor supply are starting to weigh on job growth, keeping the Fed cautious and supportive of a wait-and-watch approach amid inflation risks.

Brent Expected to Trade 90–120 USD/bbl

Brent Crude 1M Futures are expected to trade in a range of 90 USD/bbl to 120 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

LPG Market Update

India’s LPG import slump in March'26 signals Gulf disruption impact, triggers strategic shift toward US supply

- India’s LPG import profile shifted sharply in March, with total volumes declining 31.5% MoM to 1,462 KT (down 674 KT), driven by a steep 59.9% drop in Gulf supplies (ex-Iran) to 788 KT (-1,177 KT), reducing their share from 92.0% to 53.9% amid disruptions around the Strait of Hormuz.

- This was partially offset by a surge in imports from the United States, which rose 374% MoM to 533 KT (+421 KT), lifting its share to 36.5%, alongside incremental volumes from Iran (42 KT, +139%), the Russian Federation (32 KT), Indonesia (23 KT, +27.9%), and Argentina (23 KT).

- Despite this rebalancing, the shift toward long-haul cargoes implies higher freight intensity and longer supply chains, reinforcing near-term tightness and upward pressure on delivered LPG costs.

India’s LPG balance under pressure as Hormuz disruptions persist, with vessel arrivals providing short-term supply relief

- India’s LPG supply–demand balance remains under near-term pressure amid geopolitical disruptions, with domestic demand estimated at 92.6–95.0 KT/day (~33 MMT annually), of which 55–60 KT/day (60–65%) is met through imports and ~35 KT/day from domestic production; notably, ~90% of imports transit through the Strait of Hormuz, creating significant exposure to ongoing disruptions.

- Recent vessel inflows have provided partial relief, with Hellas Gladiator (24 KT, Netherlands) and Gas Jupiter (24 KT, United States) having arrived on March 30 at Ennore Port and Visakhapatnam Port respectively, followed by BW TYR reaching Mumbai on March 31; BW ELM is expected to arrive at Mangaluru on April 1 after successfully transiting the Strait of Hormuz under Indian Navy escort as part of Operation Urja Suraksha.

- Earlier arrivals of Jag Vasant and Pine Gas (combined 92.6 KT; March 26–27) added roughly one day of national demand cover, along with the previously discharged Shivalik and Nanda Devi cargoes (92.5 KT; March 15–16) offering temporary relief despite persistent structural supply risks.

Impact Assessment of US/Israel-Iran Conflict

Nayara Energy Refinery Maintenance Update:

- Based on multiple sources, Nayara Energy is planning to go for a maintenance for a period of around 35 days from early Apr’26. Already, earlier in Dec’25, Nayara Energy postponed it’s refinery maintenance due to some vendor related constraints related to Catalysts (because of EU Sanctions related to Russian Crude oil buying). To ensure the safety & efficiency of Refinery, Nayara is planning to go for this maintenance from early Apr’26.

- Nayara has a Refinery capacity of 20 million tons per Annum and PP Production capacity of 450 thousand tons per Annum. Despite possible buffer stocks of Petroleum Products & PP Resin availability during the maintenance, amid ongoing crisis of LPG & Polymers Shortage in domestic market, this plant maintenance during Apr’26 is going to further tighten LPG & PP Resin supplies in the domestic market providing support to PP Resin prices.

- Multiple PP production plants in India got affected over the last 3 months, RIL Jamnagar. Amid current government restrictions over diversion of Propane to LPG rather than for PP production, more plants like MRPL, GAIL, RIL, OPaL production are also expected to get impacted.

- A fire on a fully loaded Kuwaiti oil tanker hit by an Iranian attack at Dubai Port was extinguished, raising concerns about a possible oil spill. The tanker was loaded with 2 mln bbl of crude oil from Kuwait and Saudi Arabia, with a destination of Qingdao, China.

- Crude oil production resumed at Libya's Sharara and El Feel oilfields after completing maintenance on a crude export pipeline. The fields had been shut down due to pipeline damage and a suspension in operations.

- Sharara is one of Libya's largest production areas, with a capacity of between 0.30and 0.32 MBpd.

- The risk of an expanded Iran war grew on Saturday as Yemen's Iran-aligned Houthis launched their first attacks on Israel since the start of the conflict, even as additional US forces reached the Middle East.

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Russian Deputy Prime Minister instructed the energy ministry to draft a resolution banning gasoline exports from 01st Apr'26. The ban will remain in place until 31st Jul'26 due to global oil market turmoil caused by the Middle East crisis.

- Russia has imposed export curbs on gasoline and diesel to control rising fuel prices and tackle shortages. Last year, Russia exported nearly 0.12 MBpd of gasoline.

- The US President Trump extended a pause on attacks against Iran’s energy infrastructure until 06th Apr'26, amid ongoing but disputed talks, as the prolonged conflict continues to strain global markets and raise inflation concerns.

IEA member nations have agreed to a coordinated release of 400 mln bbl — the largest emergency SPR release since the IEA was founded after the 1973 Oil Crisis. The US, under the Trump administration, is contributing 172 mln bbl structured as loans to companies with repayment including a premium.

Deliveries are expected to begin reaching the market by the end of next week and will continue over approximately 120 days. The first batch of 86 mln bbl has already been opened for bidding. Japan will release 80 mln bbl beginning 16th Mar'26.

IEA Region-wise Release Breakdown — As of 15 Mar 2026

Key Supply Infrastructure

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026; AMJ Quarter Most Severe

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Exchange of attacks between US/Israel and Iran continuing, leading to severe/significant/complete disruptions of crude oil and its products trade through the Strait of Hormuz, severely impacting Iraq's and Kuwait's crude oil production over the next 3 to 6 months. Full-year 2026 deficit: −1.90 MBpd. AMJ quarter most acute at −4.50 MBpd.

- Scenario 2 (Alternate): Partial disruptions of crude oil trade through the Strait of Hormuz, with Iran not targeting ships and oil tankers moving toward China, India, and select Asian nations outside the Western alliance. Full-year 2026 deficit: −1.35 MBpd. Balance returns to flat by OND '26.

- The US Dollar Index edged higher in yesterday's session, rising from 100.15 to 100.50 level, trading near a 10-month high. The index recorded a daily gain of 0.36% and advanced 1.58% on a weekly basis.

- The upward move was primarily supported by safe-haven demand amid escalating geopolitical tensions in the Middle East, particularly the ongoing Iran–Israel conflict, which weighed on global risk sentiment and drove capital flows toward the dollar.

- On the US front, US weekly jobless claims show a stable labor market with limited layoffs, despite macro risks from Middle East tensions and trade uncertainty. Initial claims rose modestly by 5K to 210K, in line with expectations, while continuing claims fell 32K to 1.819M, the lowest in nearly two years, indicating steady absorption of unemployed workers.

- The labor market remains in a “low-hire, low-fire” phase, though rising oil prices, tariff uncertainty, and tightening labor supply are starting to weigh on job growth, keeping the Fed cautious and supportive of a wait-and-watch approach amid inflation risks.

Brent Expected to Trade 90–120 USD/bbl

Brent Crude 1M Futures are expected to trade in a range of 90 USD/bbl to 120 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

Impact Assessment of US/Israel-Iran Conflict

Nayara Energy Refinery Maintenance Update:

- Based on multiple sources, Nayara Energy is planning to go for a maintenance for a period of around 35 days from early Apr’26. Already, earlier in Dec’25, Nayara Energy postponed it’s refinery maintenance due to some vendor related constraints related to Catalysts (because of EU Sanctions related to Russian Crude oil buying). To ensure the safety & efficiency of Refinery, Nayara is planning to go for this maintenance from early Apr’26.

- Nayara has a Refinery capacity of 20 million tons per Annum and PP Production capacity of 450 thousand tons per Annum. Despite possible buffer stocks of Petroleum Products & PP Resin availability during the maintenance, amid ongoing crisis of LPG & Polymers Shortage in domestic market, this plant maintenance during Apr’26 is going to further tighten LPG & PP Resin supplies in the domestic market providing support to PP Resin prices.

- Multiple PP production plants in India got affected over the last 3 months, RIL Jamnagar. Amid current government restrictions over diversion of Propane to LPG rather than for PP production, more plants like MRPL, GAIL, RIL, OPaL production are also expected to get impacted.

- The risk of an expanded Iran war grew on Saturday as Yemen's Iran-aligned Houthis launched their first attacks on Israel since the start of the conflict, even as additional US forces reached the Middle East.

- Russian Deputy Prime Minister instructed the energy ministry to draft a resolution banning gasoline exports from 01st Apr'26. The ban will remain in place until 31st Jul'26 due to global oil market turmoil caused by the Middle East crisis.

- Russia has imposed export curbs on gasoline and diesel to control rising fuel prices and tackle shortages. Last year, Russia exported nearly 0.12 MBpd of gasoline.

- The US President Trump extended a pause on attacks against Iran’s energy infrastructure until 06th Apr'26, amid ongoing but disputed talks, as the prolonged conflict continues to strain global markets and raise inflation concerns.

- Russia’s Kirishinefteorgsintez refinery, one of the country’s largest, halted operations after Ukrainian drone attacks sparked fires, further straining oil supply as significant export capacity is already disrupted.

- The attacks also impacted key Baltic export routes, with loadings at Primorsk and Ust-Luga suspended, worsening Russia’s ongoing supply challenges.

- At least 40% of Russia's oil export capacity has halted due to Ukrainian drone attacks, a disputed attack on a major pipeline, and the seizure of tankers. This is the most severe oil supply disruption in modern Russian history, hitting Moscow as oil prices exceed 100 USD/bbl.

- Russia's major oil export terminals Primorsk and Ust-Luga suspended crude oil and oil products loadings on 25th Mar'26 after Ukrainian drone attacks sparked fires, with smoke visible from Finland.

- The US energy firms cut oil and natural gas rigs for the first time since mid-Jan'26, with the total rig count falling to 543 in the week to 27th Mar'26. The decline puts the total rig count down 49 rigs, or 8.3% below this time last year, with oil rigs falling to 409 and gas rigs falling to 127.

IEA member nations have agreed to a coordinated release of 400 mln bbl — the largest emergency SPR release since the IEA was founded after the 1973 Oil Crisis. The US, under the Trump administration, is contributing 172 mln bbl structured as loans to companies with repayment including a premium.

Deliveries are expected to begin reaching the market by the end of next week and will continue over approximately 120 days. The first batch of 86 mln bbl has already been opened for bidding. Japan will release 80 mln bbl beginning 16th Mar'26.

IEA Region-wise Release Breakdown — As of 15 Mar 2026

Key Supply Infrastructure

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.