- The US is seeking to loan energy companies up to 92.5 mln bbl of crude from the Strategic Petroleum Reserve as part of a global agreement aimed at calming oil markets rattled by the US-Israeli war on Iran.

- The 92.5 mln bbl are part of the 172 mln bbl from the SPR that the US agreed in Mar'26 to loan as part of a pact with more than 30 countries in the International Energy Agency (IEA) to release about 400 mln bbl to help relieve markets. The new offer, if all of it is taken by oil companies, would fulfill the US goal to loan 172 mln bbl, bids are due on 04th May'26.

- Market grapevine indicates that the OPEC+ group is expected to agree on a small increase in oil output quotas on 03rd May'26, despite the loss of most of its exports due to the US-Israeli war with Iran and the exit of a key member, the United Arab Emirates.

- The group will likely agree to an increase of around 0.19 MBpd, similar to last month's hike, minus the UAE's share. This decision would signal that OPEC+ is continuing with a business-as-usual approach.

- The UAE decision to leave OPEC will significantly reduce the 65-year-old producer group's influence over the oil market, potentially triggering a price war among Gulf producers to regain market share after the Iran war.

- The UAE's exit may also weaken the OPEC+ alliance and encourage other members to question the value of limiting output, raising the risk of further defections and years of turbulence in the oil market.

- The US government imposed sanctions on 35 entities and individuals for their roles in Iran's shadow banking sector, and warned banks against doing business with Chinese "teapot" refineries that pay tolls for shipments through the Strait of Hormuz.

- The Treasury Department's Office of Foreign Assets Control (OFAC) said the designated individuals and firms had facilitated the movement of tens of bln of dollars tied to sanctions evasion and Iran's sponsorship of terrorism.

IEA member nations have agreed to a coordinated release of 400 mln bbl — the largest emergency SPR release since the IEA was founded after the 1973 Oil Crisis. The US, under the Trump administration, is contributing 172 mln bbl structured as loans to companies with repayment including a premium.

Deliveries are expected to begin reaching the market by the end of next week and will continue over approximately 120 days. The first batch of 86 mln bbl has already been opened for bidding. Japan will released 80 mln bbl beginning 16th Mar'26.

IEA Region-wise Release Breakdown

Key Supply Infrastructure

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Exchange of attacks between US/Israel and Iran continuing, leading to severe/significant/complete disruptions of crude oil and its products trade through the Strait of Hormuz, severely impacting Iraq's and Kuwait's crude oil production over the next 3 to 6 months. Full-year 2026 deficit: −1.90 MBpd. AMJ quarter most acute at −4.50 MBpd.

- Scenario 2 (Alternate): Partial disruptions of crude oil trade through the Strait of Hormuz, with Iran not targeting ships and oil tankers moving toward China, India, and select Asian nations outside the Western alliance. Full-year 2026 deficit: −1.35 MBpd. Balance returns to flat by OND '26.

- On the US front, US retail sales recorded a solid rebound in Feb'26, rising 0.6% MoM and 3.7% on YoY, marking the strongest gain in seven months, supported by a recovery in motor vehicle purchases and seasonal factors. Core retail sales also came in firm at 0.5% MoM, indicating underlying consumption strength, with higher tax refunds playing a key role in sustaining household spending during the period.

- The US manufacturing activity continued to expand, with ISM PMI rising to 52.7 in March, its highest level since Aug'22. That said, the improvement was partly driven by slower supplier deliveries, reflecting supply chain disruptions rather than demand strength, particularly amid shipping constraints and trade frictions. This has also led to a sharp rise in input cost pressures, with the prices paid index jumping significantly, signaling building inflation at the producer level.

Brent Crude 1M Futures are expected to trade in a range of 90 USD/bbl to 110 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

LPG Market Update

08th Indian-flagged LPG vessel has transited the Strait of Hormuz and reached India

India’s LPG import slump in March'26 signals Gulf disruption impact, triggers strategic shift toward US supply

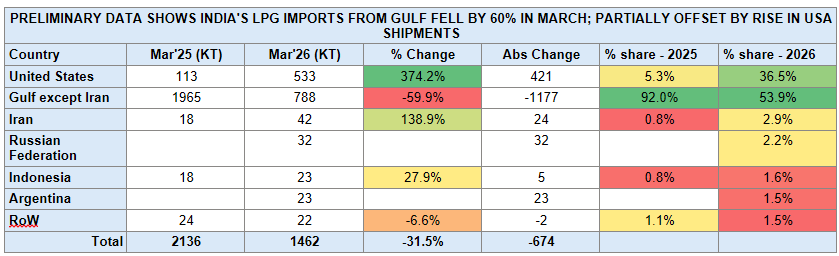

- India’s LPG import profile shifted sharply in March, with total volumes declining 31.5% MoM to 1,462 KT (down 674 KT), driven by a steep 59.9% drop in Gulf supplies (ex-Iran) to 788 KT (-1,177 KT), reducing their share from 92.0% to 53.9% amid disruptions around the Strait of Hormuz.

- This was partially offset by a surge in imports from the United States, which rose 374% MoM to 533 KT (+421 KT), lifting its share to 36.5%, alongside incremental volumes from Iran (42 KT, +139%), the Russian Federation (32 KT), Indonesia (23 KT, +27.9%), and Argentina (23 KT).

- Despite this rebalancing, the shift toward long-haul cargoes implies higher freight intensity and longer supply chains, reinforcing near-term tightness and upward pressure on delivered LPG costs.

IOCL Price Update — 1 May 2026

- Unchanged: Retail Petrol, Diesel, Domestic LPG (14.2 kg @ Rs 913 in Delhi), ATF for domestic airlines, and PDS Kerosene — covering -80% of petroleum products.

Revised upward:

• 19 kg Commercial LPG: +Rs 993 (Delhi: Rs 2,078.50 → Rs 3,071.50; Mumbai: Rs 2,031 → Rs 3,024)

• 5 kg Free Trade LPG (FTL): +Rs 261 per cylinder.