- On 08th Jun'26, Iran backed militant group Houthis indicates that they would ban Israeli maritime navigation through the red sea, adding pressure on global shipment flows through the key transit routes.

- Russia's crude exports from its western ports (Primorsk, Ust-Luga, and Novorossiysk) are expected to fall sharply to 1.7 MBpd in Jun'26 from 2.5 MBpd in May'26, as the country diverts more crude to domestic refineries and seeks to increase refinery runs by 0.25–0.40 MBpd to address seasonal fuel shortages.

- Russian oil production has been declining due to refinery maintenance and Ukrainian drone attacks, with output estimated to have fallen 0.30–0.40 MBpd in Apr'26 (the largest drop since 2020) and a further 0.10 MBpd in May'26, while recovery is expected to take time.

- Abu Dhabi National Oil Company has issued its second crude oil tender within a week, offering up to 2 mln bbl of Upper Zakum, Umm Lulu, and Das crude for Jun'26–Aug'26 loading.

- The move highlights ADNOC's efforts to maintain exports despite disruptions around the Strait of Hormuz, with some shipments reportedly transported using tankers with tracking systems turned off and completed via ship-to-ship transfers or direct deliveries to buyers.

- Israel said it struck military targets in western and central Iran on 08th Jun'26 after Iran launched missiles at Israeli targets, despite reports that US President Trump had urged Israeli Prime Minister Benjamin Netanyahu to avoid further attacks while US-Iran peace talks continue.

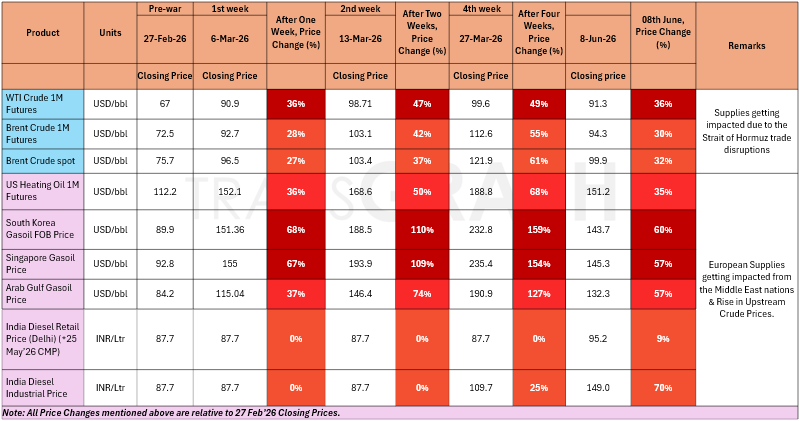

- Saudi Aramco cut its July crude oil official selling prices (OSPs) to Asia for a second consecutive month, lowering the premium for Arab Light crude by 6.0 USD/bbl to 9.5 USD/bbl above the Dubai/Oman benchmark, reflecting weaker spot market premiums and sluggish demand, particularly from China.

- Despite the reduction, OSPs remain elevated compared to pre-war levels due to ongoing disruptions to energy flows through the Strait of Hormuz caused by the Iran conflict, while prices to other regions were also reduced.

War Impact on Crude Oil & Gasoil/Diesel Prices

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

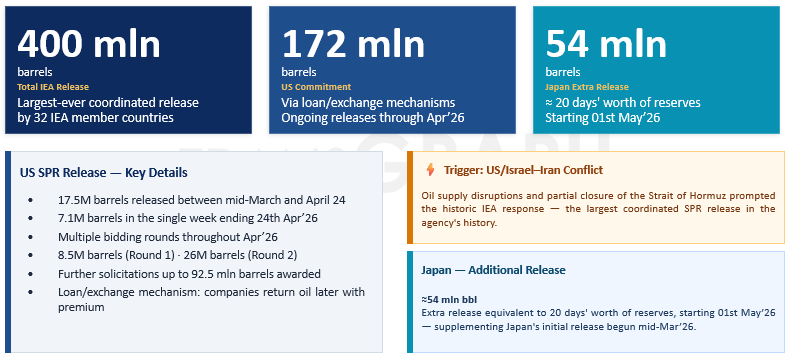

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks to remain on a progressive note and flows through the Strait of Hormuz improving over the coming weeks; however crude oil production losses will be there due to further non-availability of storage on on-shore in Iraq, Kuwait and other small Middle East nations.

- Scenario 2 (Alternate): No major deal being achieved from ceasefire talks and post completion of ceasefire talks, tensions continuing to remain in the Middle East and flows through the Strait of Hormuz continuing to remain restrained. Crude Oil Production Facilities & Refining Centers in the Middle East region getting affected and trade disruptions in Strait of Hormuz will be there for medium to long term (4 to 7 months).

Brent Crude 1M Futures are expected to trade in a range of 100 USD/bbl to 125 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

Metals & Energy Market Update – Geopolitical Context (Iran Conflict)

Geopolitical backdrop:

Israel and Iran traded the worst exchange of fire since the April truce, with Iran firing missiles at Israeli targets and Israel carrying out strikes on western and central Iran. Brent bounced back strongly as renewed tensions stoked fresh supply fears and Hormuz near-closure continues to put a structural floor under prices. Equities saw sharp selloff in Asia at the open as well, with Kospi down by 14%, Nikkei down by 1.31% and Nifty down by 1.2%, S&P down by 2.64%, and Nasdaq registered a heavy sell-off and marked a 4.18% loss. Higher energy, slower growth, and limited room for rate cuts keep yields elevated. Safe-haven flows are rotating into money markets and short-duration paper.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 8.7%.

Base metals:

- Copper ended last week down by 1%, primarily due to stronger dollar and weak demand.

- Aluminum rose by 18.3% since start of war linked to Gulf region supply disruptions. However, demand softness now driving price action.

- IMF downgraded 2026 global growth to 3.1% (from 3.3% earlier and 3.4% in 2025), highlighting war-related downside risks.

Precious metals:

- Volatility has eased, but prices face upward pressure, due to improving market sentiment in peace talks.

- However, any esclation and halt in a resolution will pressure on Precious Metals.

- Stronger U.S. yields and weak industrial offtake—especially auto—are suppressing any upside momentum.

LPG Market Update - 09 June 2026

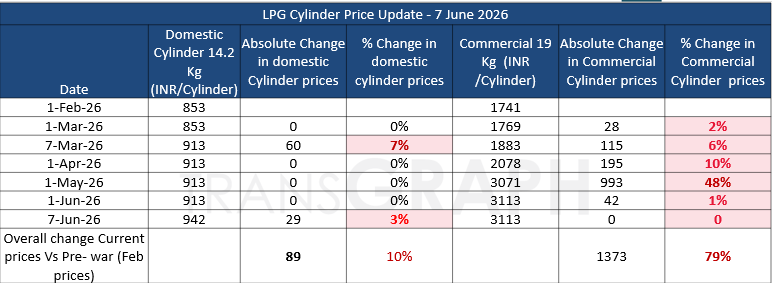

- India’s LPG market saw another upward revision on 1st June 2026 , with oil marketing companies increasing commercial cylinder prices. Commercial LPG prices were raised across major cities, with the 19 kg cylinder in Delhi increasing by Rs 42 to Rs 3,113.50. Similar hikes were reported nationwide, ranging from Rs 42 to Rs 53.50 per cylinder.

India’s domestic LPG market witnessed a price revision on 7 June 2026, with Oil Marketing Companies (OMCs) increasing the price of the 14.2 kg domestic LPG cylinder by ₹29 per cylinder across the country. - In addition to commercial cylinders, oil marketing companies also increased the price of 5 kg Free Trade LPG (FTL) cylinders by Rs 11. Following the revision, the retail price of a 5 kg FTL cylinder in Delhi now stands at Rs 821.50. FTL cylinders are sold outside the subsidized domestic LPG system and are commonly used by migrant workers, temporary households, street vendors, and consumers requiring smaller LPG packs.