- The US crude exports reached a record high of 5.6 MBpd in May'26 due to the Middle East crisis, which increased demand from Asian and European refiners. The US and Israel's war with Iran disrupted global energy markets, causing refiners to seek alternatives to Middle Eastern supply. US crude exports surged past the previous record set in Apr'26 of 5.2 MBpd, with Asia taking 2.45 MBpd and Europe 2.4 MBpd of the barrels exported in May'26.

- According to market grapevines the Lukoil-owned Volgograd oil refinery in Russia's south has suspended oil processing since 29th May'26 due to a Ukrainian drone attack that caused fire and damages. The attack has halted the crude distillation unit CDU-1, which accounts for 40% of the plant's capacity, and stopped other units CDU-6 and CDU-5.

- The refinery processed 13.5 million metric tons of oil in 2024, accounting for 5% of total Russian refinery volume, producing 6 million tons of diesel, 1.9 million tons of gasoline, and 700,000 tons of fuel oil.

- Iran is seeking a limited interim agreement with the United States to ease economic pressure, stabilise the situation at home, and avoid major concessions on its nuclear programme. The approach reflects a familiar playbook for the Islamic Republic: absorb pressure, avoid irreversible compromises and keep negotiations alive without shifting core positions.

- India will cut its export duties on petrol, diesel, and aviation turbine fuel (ATF) for the fortnight starting 01st Jun'26, based on average international prices of crude oil, petrol, diesel, and ATF since the last review. The duty on exports of petrol has been set at 1.5 rupees per litre, while that on diesel has been set at 13.5 rupees per litre.

- Export duties on ATF have been set at 9.5 rupees per litre. There is no change in the existing excise duty rates on petrol and diesel cleared for domestic consumption.

- China's seaborne crude oil imports fell to their lowest in almost 10 years in May, dropping to 6.36 MBpd, due to the impact of the Iran war and the closure of the Strait of Hormuz.

- The collapse in China's imports is being framed as helping Asia adjust to the loss of at least 10 MBpd of crude, but it is a serendipitous side effect rather than any altruism on Beijing's part.

- The primary driver behind the collapse in China's oil imports is the conflict in the Middle East, but the real challenge is in working out the why and how of what China is doing to adapt to the loss of as much as 10% of global crude supplies from the Iran conflict.

- According to the Energy Information Administration the US crude production remained steady at 13.7 MBpd in Mar'26. Texas crude output fell to a four-month low, while New Mexico production was unchanged. The US crude production is expected to rise as operators increase output in response to high oil prices due to the Iran war.

- Venezuela's oil exports rose to 1.25 MBpd in May'26, marking the third consecutive month of increase, driven by more cargoes to the US, India, and Europe. Under the US-supported government of interim President Rodriguez, Venezuelan crude production and exports have bounced this year as Washington eased sanctions and foreign companies expanded oil and gas projects in the OPEC nation.

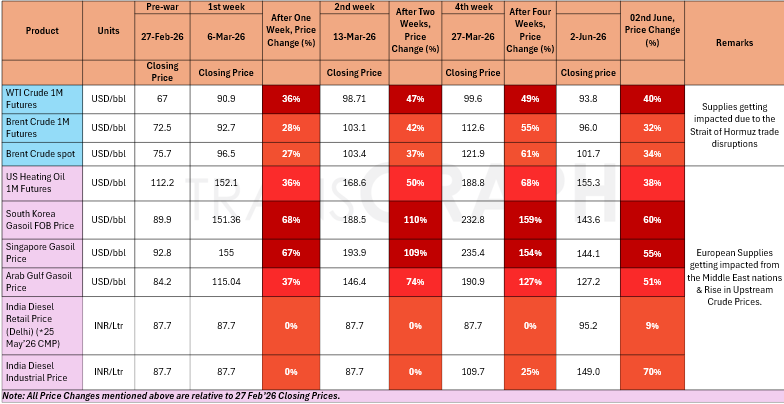

War Impact on Crude Oil & Gasoil/Diesel Prices

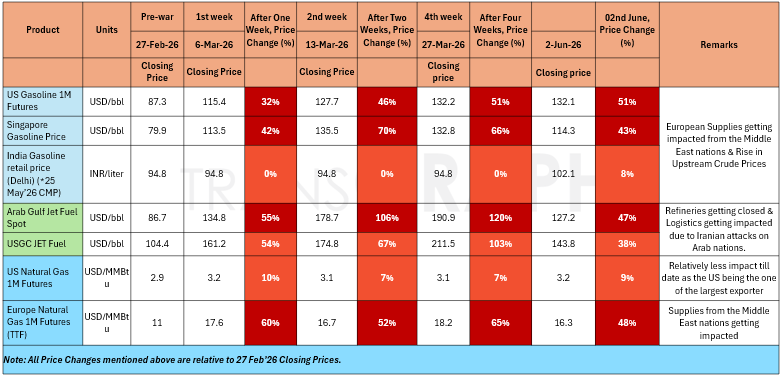

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

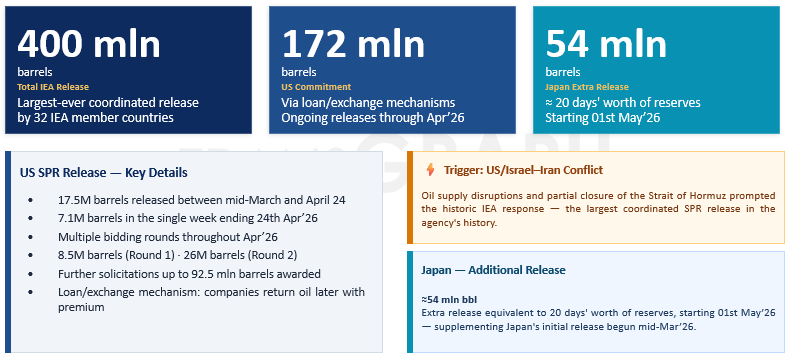

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks to remain on a progressive note and flows through the Strait of Hormuz improving over the coming weeks; however crude oil production losses will be there due to further non-availability of storage on on-shore in Iraq, Kuwait and other small Middle East nations.

- Scenario 2 (Alternate): No major deal being achieved from ceasefire talks and post completion of ceasefire talks, tensions continuing to remain in the Middle East and flows through the Strait of Hormuz continuing to remain restrained. Crude Oil Production Facilities & Refining Centers in the Middle East region getting affected and trade disruptions in Strait of Hormuz will be there for medium to long term (4 to 7 months).

Brent Crude 1M Futures are expected to trade in a range of 100 USD/bbl to 125 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

Metals & Energy Market Update – Geopolitical Context (Iran Conflict)

Geopolitical backdrop:

The ongoing conflict in the Middle East, continues to weigh on global markets and keeping inflation expectations elevated. The war-driven rise in energy prices has heightened concerns about higher transportation and manufacturing costs globally, adding further pressure to already elevated inflation. At the same time, elevated crude prices continue to weigh on emerging markets and developing economies, particularly large energy-importing nations, as higher import bills and currency pressures weaken economic stability and complicate monetary policy decisions in the nearterm.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 9.0%.

Base metals:

- Copper ended last week up by 0.5%, primarily due to widening LME-CME spread.

- Aluminum rose by 19.4% since start of war linked to Gulf region supply disruptions. However, demand softness now driving price action.

- IMF downgraded 2026 global growth to 3.1% (from 3.3% earlier and 3.4% in 2025), highlighting war-related downside risks.

Precious metals:

- Volatility has eased, but prices face upward pressure, due to improving market sentiment in peace talks.

- However, any esclation and halt in a resolution will pressure on Precious Metals.

- Stronger U.S. yields and weak industrial offtake—especially auto—are suppressing any upside momentum.

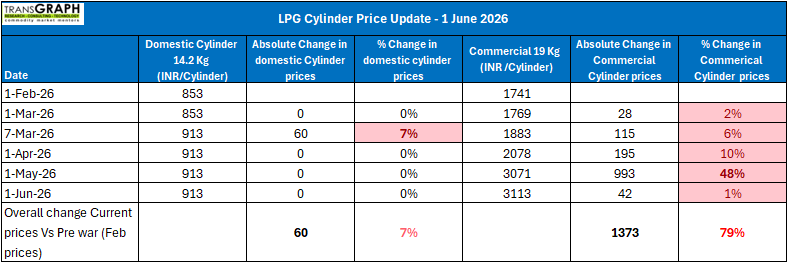

LPG Market Update - 02 June 2026

- India's LPG market saw another upward revision on 1st June 2026 , with oil marketing companies increasing commercial cylinder prices Commercial LPG prices were raised across major cities, with the 19 kg cylinder in Delhi increasing by Rs 42 to Rs 3,113.50. Similar hikes were reported nationwide, ranging from Rs 42 to Rs 53.50 per cylinder. Kolkata recorded the sharpest increase of Rs 53.50, taking prices to Rs 3,255.50, while Hyderabad and Bhubaneswar saw hikes of Rs 52 each. Mumbai's commercial LPG price rose by Rs 43.50 to Rs 3,067.50, and Chennai's rate increased by Rs 46 to Rs 3,283.00.

- In addition to commercial cylinders, oil marketing companies also increased the price of 5 kg Free Trade LPG (FTL) cylinders by Rs 11. Following the revision, the retail price of a 5 kg FTL cylinder in Delhi now stands at Rs 821.50. FTL cylinders are sold outside the subsidized domestic LPG system and are commonly used by migrant workers, temporary households, street vendors, and consumers requiring smaller LPG packs.

- For June, Saudi Aramco CPs increased further to USD 760/ton for propane and USD 820/ton for butane, reflecting continued market tightness and persistent concerns over Middle East supply security.

In contrast, Algeria's Sonatrach moved in the opposite direction, implementing substantial reductions in its June LPG benchmarks. Propane prices were cut by USD 125/ton to USD 575/ton, representing an 18% decline from May levels. Butane experienced an even sharper correction, falling by USD 270/ton to USD 610/ton, a drop of approximately 31%.