India External Accounts – Trade Balance – October (Marketing Article)

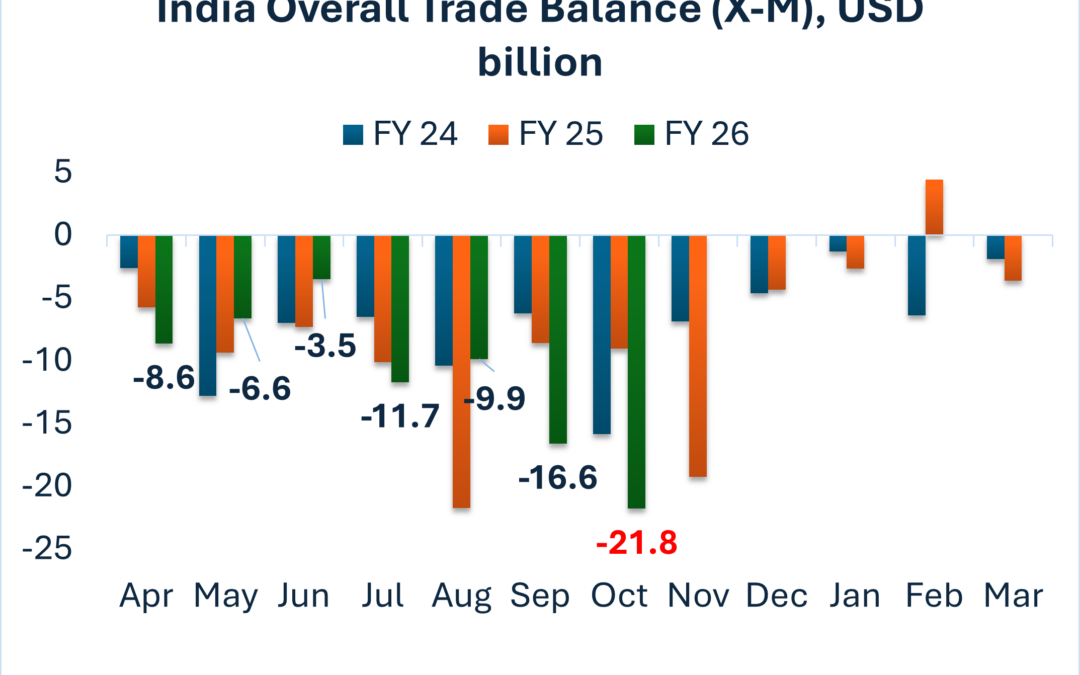

- India’s Overall Trade Deficit deepened to USD 21.8 billion, up sharply from previous month’s USD 16.6 billion, as Merchandise deficit rose by 58% YOY to USD 41.7 billion , from USD 26.2 billion in Oct’24.

- Merchandise exports fell 11.8% to USD 34.4 billion, as Gems and Jewellery exports fell by 29.5% and export of Engineering goods saw a 16.7% decline YoY.

- Services Exports on the other hand held strong, posting a 11.8% growth YoY from USD 34.4 billion in Oct’24 to USD 38.5 billion currently.

- The sharp rise in the merchandise trade deficit is largely driven by an extraordinary 200% surge in gold imports. Taken together, these developments heighten concerns over a widening external imbalance and signal renewed pressure on the rupee, even as domestic fundamentals remain broadly stable.

A widening trade deficit is once again flashing warning signs for India’s external account, mirrored in the persistent depreciation bias of the rupee. The strain is being compounded by Reliance’s pause in discounted Russian crude imports—a shift that threatens to lift energy costs, inflate the import bill, and further weaken India’s trade position.

- India has averaged USD 62 billion a month in merchandise imports across FY25 and FY26 (YTD), making October’s USD 76.1 billion print a sharp 22.7% overshoot. The sharp rise in the merchandise trade deficit is largely driven by an extraordinary 200% surge in gold imports.

- India’s merchandise trade deficit has sharply widened, deepening 58% year-on-year to USD 41.7 billion from USD 26.2 billion last year, as imports surged to USD 76.1 billion while exports lagged at USD 34.4 billion. This growing imbalance underscores the mounting strain on India’s external position, as demand for imports continues to outpace export momentum.

- India has averaged USD 62 billion a month in merchandise imports across FY25 and FY26 (YTD), making October’s USD 76.1 billion print a sharp 22.7% overshoot. The sharp rise in the merchandise trade deficit is largely driven by an extraordinary 200% surge in gold imports.

The primary drivers behind the surge in gold imports come as elevated global gold prices have amplified the value of inbound shipments, while on the other hand, the Reserve Bank of India has continued to build up its gold reserves as part of a broader effort to diversify its asset holdings away from traditional currencies, particularly the Dollar. Together, these forces have pushed the value of gold imports higher, contributing to the expansion of the import bill.

And this is unfolding at a time when the rupee is otherwise supported by robust domestic growth signals and contained inflation, even as the global backdrop, from a hawkish Federal Reserve to tightening liquidity conditions, grows more complex. The real question for markets now is whether India’s trade story can rebalance quickly enough to keep the rupee’s long-term narrative intact.

In conclusion, the rupee’s recent weakness is less a crisis and more a question mark — one reopened by a widening trade gap and a sharp uptick in import demand, particularly for gold and energy. These shifts are not yet destabilising, but they do introduce an unmistakable depreciation bias and invite a closer scrutiny at the strength of India’s external balance account.

Капсульный дом — из каких материалов его чаще всего изготавливают?

Можно ли доверять бесплатным VPN-расширениям для браузера?

Стоит ли доверять vpn-провайдерам с политикой no-logs?

новинки кино 2026 смотреть онлайн кино онлайн в хорошем качестве

микрозайм взять https://tbcareer.ru

займ оформить микрозайм без процентов

Сколько стоят услуги маркетинговое агентство для малого бизнеса в 2026 году?

магазин танцевальной одежды обручи для гимнастики

Компания fastek https://fastek.by проектируем и поставляем надежные фасадные системы для коммерческих и жилых объектов, обеспечивая долговечность, энергоэффективность и безупречный внешний вид здания под ваши задачи.

гигиена зубов official website

Tara river holidays source

как сделать профиль продавца лучше как увеличить охват на Авито

Budva beach car rental service https://montenegro-car-rental-hire.com

buy thc kush in prague joint in prague

Купить земельный участок https://novoesonino.ru в коттеджном поселке «Новое Сонино». Земли ИЖС с электричеством, дорогами и перспективой комфортного проживания за городом. Отличное место для строительства загородного дома в городском округе Домодедово.

Как домашние животные помогают людям справляться с депрессией?

Купить квартиру https://kupi-kvartiruspb.ru или апартаменты в Курортный район Санкт-Петербурга. Жилые комплексы рядом с Финским заливом, парками и зонами отдыха. Комфортные планировки, современные дома и удобная транспортная доступность.

Нужен участок? новое растуново отличное решение для строительства загородного дома. Участки ИЖС, удобный подъезд, электричество и развитая инфраструктура. Комфортное место для постоянного проживания недалеко от Москвы.

ЖК премиум-класса https://kvartiry-spb78.ru от застройщика — современные квартиры с продуманными планировками, высоким уровнем комфорта и развитой инфраструктурой. Закрытая территория, подземный паркинг, благоустроенные дворы и престижное расположение для комфортной жизни.

Нужна декоративная лепнина? https://ppu-lepnina.ru стильный декоративный элемент для интерьера. Карнизы, молдинги, колонны и розетки помогают создавать выразительный дизайн помещений. Материал устойчив к влаге, долговечен и легко устанавливается.

Частные детские сады https://razvitie21vek.com в Москва для детей от раннего возраста. Развивающие программы, безопасная среда, квалифицированные воспитатели и подготовка к школе. Комфортные условия для обучения, общения и всестороннего развития ребенка.

Steam Desktop Authenticator https://authenticatorsteamdesktop.com is a PC app that lets you use the Steam Mobile Authenticator on your computer. It supports trade confirmation, account security, and managing two-factor authentication codes without using your smartphone.

Steam Desktop Authenticator https://steamdesktopauthenticator.net is a popular solution for Steam users who need access to Steam Guard features on their computer. It conveniently verifies actions, protects your account, and manages authentication in a single app.

Steam Desktop Authenticator https://sdasteam.com (SDA). It allows you to generate account login codes and automatically confirm trades or item sales on the Community Market without using your smartphone.

заказать песок карьерный песок карьерный

Курсы ораторского мастерства kultura-rechi для развития навыков общения и публичных выступлений. Практика, упражнения на дикцию, управление голосом, преодоление страха сцены и умение удерживать внимание слушателей.

Go for details: 4th emperor of rome

Семейный юрист https://semeinyi-urist-moskva.ru в Москве: развод, раздел имущества, алименты, определение места жительства детей. Опыт 20+ лет. Знаем и умеем делить ипотечные квартиры, бизнес, коммерческую недвижимость, ИИ и ООО. Индивидуальный подход. Конфиденциально.

Семейный юрист https://semeinyi-urist-moskva.ru в Москве: развод, раздел имущества, алименты, определение места жительства детей. Опыт 20+ лет. Знаем и умеем делить ипотечные квартиры, бизнес, коммерческую недвижимость, ИИ и ООО. Индивидуальный подход. Конфиденциально.

Custom-made room furniture custom cabinets Tampa FL

песок карьерный цена за 1 м3 https://pesok-karernyy-kupit1.ru

exchange usdt trc20 to cash usd usdt trc20 to rub

обменник usdt на любую валюту продать usdt за наличные

Только что опубликовано: https://remont-kras.ru

вывод usdt на банковскую карту продать тезер за наличные рубли

Personalized summary: https://blockchainreporter.net/web3-everything-you-need-to-know/

Полная версия статьи: https://okna-domostroy.ru

Стрийські новини https://stryi.in.ua актуальні події міста Стрий та регіону. Оперативна інформація про події, суспільне життя, культуру, економіку та важливі зміни. Слідкуйте за новинами, які відбуваються поряд із вами.

Стрийські новини https://stryi.in.ua актуальні події міста Стрий та регіону. Оперативна інформація про події, суспільне життя, культуру, економіку та важливі зміни. Слідкуйте за новинами, які відбуваються поряд із вами.

Блог про бижутерию https://glamglam.ru и подарки с полезными статьями о модных аксессуарах, украшениях и идеях для подарков. Обзоры трендов, советы по выбору бижутерии, рекомендации по сочетанию украшений и вдохновение для особых случаев.

Блог про бижутерию https://glamglam.ru и подарки с полезными статьями о модных аксессуарах, украшениях и идеях для подарков. Обзоры трендов, советы по выбору бижутерии, рекомендации по сочетанию украшений и вдохновение для особых случаев.

Продвижение сайта с гарантией — как отличить честное предложение от ловушки?

Последние изменения: https://mybabyplan.ru

Читать расширенную версию: https://l-parfum.ru/catalog/paco-rabanne/black-xs-pour-homme/

Все самое свежее здесь: https://l-parfum.ru/catalog/originaly/calvin_klein/2305/

Читать расширенную версию: https://home-parfum.ru/catalog/jean-paul-gaultier_2/

Больше на нашем сайте: https://spainslov.ru/site/word/word/%d0%a4%d0%95%d0%a0%d0%9c%d0%a3%d0%90%d0%a0

Последние изменения: https://home-parfum.ru/products/davidoff-cool-water-wave100-ml/

Читать расширенную версию: https://spainslov.ru/site/word/word/%d0%a3%d0%a1%d0%9b%d0%a3%d0%96%d0%98%d0%92%d0%90%d0%a2%d0%ac

Whitecrest Resort https://whitecrestonline.com.au offers excellent conditions for relaxation and rejuvenation. Modern infrastructure, comfortable accommodations, active recreation, and a tranquil atmosphere create the perfect vacation setting.

Нуждаете се спешно от пари в брой? Заложна къща Галерия 65 Варна предлага бързи заеми, обезпечени със злато, електроника, часовници и други ценности. Предлагаме конкурентни оценки на имоти, бърза обработка и професионално обслужване.

Whitecrest Resort https://whitecrestonline.com.au offers excellent conditions for relaxation and rejuvenation. Modern infrastructure, comfortable accommodations, active recreation, and a tranquil atmosphere create the perfect vacation setting.

Нуждаете се спешно от пари в брой? Заложна къща Галерия 65 Варна предлага бързи заеми, обезпечени със злато, електроника, часовници и други ценности. Предлагаме конкурентни оценки на имоти, бърза обработка и професионално обслужване.

Купить iPhone http://kupit-iphone43.ru в Нижнем Новгороде по выгодной цене с гарантией качества. В наличии популярные модели Apple, различные цвета и объемы памяти. Удобная оплата, доставка по городу, возможность покупки в кредит или рассрочку.

сайт цветов доставка цветов недорого

Купить iPhone http://kupit-iphone43.ru в Нижнем Новгороде по выгодной цене с гарантией качества. В наличии популярные модели Apple, различные цвета и объемы памяти. Удобная оплата, доставка по городу, возможность покупки в кредит или рассрочку.

номер доставки цветов где купить цветы

Где купить стиральную машину https://stiralnye-mashiny-asko.ru ASKO в Москве — ТОП-10 официальных дилеров 2026 с актуальными ценами, гарантией производителя и фирменными шоурумами. В подборке представлены проверенные магазины и официальные представители бренда ASKO, где можно сравнить модели, получить консультацию специалистов, оформить доставку и заказать профессиональное подключение техники.

Займы под залог https://црс.рф ПТС автомобиля, спецтехники и недвижимости на выгодных условиях. Быстрое рассмотрение заявки, минимальный пакет документов и возможность получить необходимую сумму без длительных проверок. Финансовые решения для частных лиц и бизнеса.

Займы под залог https://црс.рф ПТС автомобиля, спецтехники и недвижимости на выгодных условиях. Быстрое рассмотрение заявки, минимальный пакет документов и возможность получить необходимую сумму без длительных проверок. Финансовые решения для частных лиц и бизнеса.

Хочешь сладкую клубнику? сайт berryGo свежая, сладкая и ароматная ягода для всей семьи. В наличии сезонная клубника высокого качества, выращенная с соблюдением стандартов свежести. Удобный заказ, выгодные цены и быстрая доставка

Хочешь сладкую клубнику? сайт berryGo свежая, сладкая и ароматная ягода для всей семьи. В наличии сезонная клубника высокого качества, выращенная с соблюдением стандартов свежести. Удобный заказ, выгодные цены и быстрая доставка

Все про життя Полтави https://36000.com.ua новини, події, культура, дозвілля та міська інфраструктура. Корисний портал для тих, хто хоче бути в курсі актуальних подій та змін у місті.

ремонт квартир ключ ціна ремонт квартир

Удобный каталог https://weblabo.ru онлайн-калькуляторов, конвертеров и полезных сервисов для быстрых расчетов. Здесь собраны инструменты для математики, финансов, строительства, IT и повседневных задач.

Удобный каталог https://weblabo.ru онлайн-калькуляторов, конвертеров и полезных сервисов для быстрых расчетов. Здесь собраны инструменты для математики, финансов, строительства, IT и повседневных задач.

В случае если хотите найти турецкий сериал смотреть серии без траты времени и подозрительных ресурсов, оцените нашу библиотеку востребованных турецких проектов. На сайте представлены как громкие новинки последних лет, а также проверенные временем хиты, которые любят миллионы зрителей. Многие пользователи выбирают турецкие сериалы из-за захватывающих историй, запоминающимся героям, красивым локациям и насыщенной драматургии, которая не отпускает до финала. Просмотр доступен в высоком качестве, без длительной регистрации и дополнительных сложностей.

Если вам нужны лучшие турецкие сериалы онлайн без долгих поисков и подозрительных ресурсов, обратите внимание на нашу коллекцию популярных турецких телешоу. Здесь собраны как самые обсуждаемые новинки последних сезонов, вместе с ними проверенные временем хиты, которые остаются популярными среди поклонников жанра. Зрители часто выбирают турецкие сериалы за интересные сюжеты, запоминающимся героям, атмосферным съемкам и эмоциональной подаче, способной увлечь с первой серии. Все проекты можно смотреть в высоком качестве, без лишних формальностей и дополнительных сложностей.

продвижение молодых сайтов продвижение молодых сайтов .

Когда вам нужны турецкие сериалы в хорошем качестве на русском без долгих поисков и подозрительных ресурсов, обратите внимание на нашу коллекцию популярных турецких проектов. В каталоге доступны как громкие новинки последних лет, так и легендарные сериалы, которые остаются популярными среди поклонников жанра. Поклонники предпочитают турецкие сериалы благодаря сильным сюжетам, харизматичным героям, красивым локациям и насыщенной драматургии, способной увлечь с первой серии. Просмотр доступен в хорошем качестве, без лишних формальностей и лишних действий.

автовоз владивосток москва https://perevozka-avtomobilya.ru

перевозка авто автовозом стоимость автовоза

кадровые агентства по подбору персонала https://kadrovoe-agentstvo-moscow.ru

подбор персонала кадров кадровое агентство https://kadrovoe-agentstvo-moscow.ru

спецодежда ботинки рабочие ботинки мужские с металлическим подноском летние

New in the Category: מספרי טלפון של נערות ליווי

перчатки диэлектрические класс 0 https://capstr.ru/kak-vybrat-specodezhdu-v-moskve-gde-kupit-kachestvennuju-rabochuju-odezhdu-dlja-sotrudnikov/

Последние публикации: https://elicebeauty.com/ukhod-za-kozhey/volosy/konditsionery/filter/_a2584/

Все лучшее здесь: https://marykay-cosmetics.ru

3д панели для забора купить панели ограждения сетчатые 3д

3d панели ограждения купить сетка панель 3д

3в ограждения от производителя 3d забор производитель

3д панели для забора купить заборы ограждения 3д

купить 3д ограждения для забора 3 д панели для забора

3d забор производитель забор 3д от производителя

забор 3d купить 3д панели для забора

панель 3д ограждения от производителя купить забор 3д от производителя

3д забор купить купить 3d панели для забора

купить панель 3д забора 3 д заборы от производителя

3д панели для забора 3 d панели для забора

3d панели ограждения купить ограждение 3d

3 d панели для забора сварные 3d заборы

3д панель ограждения забор 3d

Скачать музыку бесплатно https://savesong.me и слушать любимые треки онлайн в хорошем качестве. Большая коллекция песен разных жанров, удобный поиск по исполнителям и альбомам, популярные новинки и хиты для прослушивания в любое время.

сайт службы дезинфекции номер телефона сэс

Мечтаешь о незабываемом отпуске? https://karta-abhazii.ru где величественные горы встречаются с бескрайним морем, а история оживает на каждом шагу, добро пожаловать в Абхазию!

Брал перфоратор https://vse-instrumenti.ru перед оформлением поискал промокод все инструменты — нашёл на этом сайте. Код сработал, скинули 10%.

школа плавания для детей секция баскетбола для детей

Купить печь для бани с баком https://stoves-fireplaces.ru

sports betting offices sports betting azimutbet

Do you love excitement? https://jerseysbeststore.com offers premium pre-match and live sports betting, as well as a legal online casino. Try your luck on modern slots, table games, or with live dealers. We guarantee complete data security, fair results, and 24/7 player support.

лента стальная гост цена лента стальная нержавеющая

Ремонт и строительство https://decor-kraski.com.ua полезные статьи, практические советы и современные решения для дома, квартиры и коммерческих объектов. Обзоры строительных материалов, технологий, инструментов и рекомендации специалистов для успешной реализации проектов.

Портал о ремонте https://goodday.org.ua и строительстве с актуальной информацией о проектировании, отделке, инженерных системах и благоустройстве. Полезные материалы помогут выбрать качественные решения и избежать распространенных ошибок.

Все о ремонте https://hotel.kr.ua и строительстве в одном месте. Статьи о возведении домов, ремонте квартир, выборе материалов, дизайне интерьера и современных строительных технологиях для комфортной и долговечной эксплуатации жилья.

Информационный ресурс https://inbound.com.ua о ремонте и строительстве для владельцев недвижимости, мастеров и застройщиков. Практические инструкции, обзоры оборудования, советы экспертов и рекомендации по выполнению работ любой сложности.

Ремонт и строительство https://insurancecarhum.org от фундамента до отделки. Полезные статьи о строительных технологиях, материалах, инженерных коммуникациях и эффективных способах обустройства жилых и коммерческих помещений.

Все о дизайне https://bconline.com.ua интерьера в одном месте. Современные стили, идеи для ремонта, подбор мебели, освещения и отделочных материалов. Практические советы помогут создать уютное и функциональное пространство.

Ремонт и строительство https://oo.zt.ua без лишних сложностей. Подробные руководства, рекомендации специалистов, обзоры материалов и полезные идеи для создания надежного, красивого и функционального жилья.

Информационный ресурс https://it-cifra.com.ua о строительстве и ремонте с акцентом на реальные решения, проверенные технологии и практический опыт. Узнавайте, как строить надежно, ремонтировать качественно и экономить бюджет.

Дизайн и интерьер https://ukk.kiev.ua идеи для оформления квартир, домов и коммерческих помещений. Современные тенденции, советы дизайнеров, готовые решения и вдохновляющие проекты для создания стильного и комфортного пространства.

Полезный портал https://panorama.zt.ua о строительстве и ремонте с материалами по проектированию, отделочным работам, благоустройству участков и выбору строительных решений. Актуальная информация для профессионалов и частных застройщиков.

Строительный портал https://teplo.zt.ua для тех, кто планирует строительство дома, ремонт квартиры или модернизацию недвижимости. Актуальные статьи, обзоры технологий, советы специалистов и полезная информация для успешной реализации проектов.

Все о строительстве https://suli-company.org.ua и ремонте в одном месте. Строительный портал публикует полезные материалы о проектировании, отделке, инженерных системах, выборе строительных материалов и современных технологиях для дома и бизнеса.

Мужской портал https://cruiser.com.ua о стиле жизни, карьере, финансах, здоровье и технологиях. Полезные статьи, экспертные советы, обзоры и практические рекомендации для современных мужчин, стремящихся к развитию, успеху и комфортной жизни.

Портал о ремонте https://juglans.com.ua и строительстве с актуальными новостями отрасли, обзорами инструментов и строительных материалов. Практические руководства помогут выполнить работы качественно и избежать распространенных ошибок.

Современный сайт https://makprestig.in.ua о ремонте и строительстве для тех, кто планирует строительство дома, реконструкцию или обновление интерьера. Экспертные советы, инструкции и практические решения для любых задач.

Портал о ремонте https://itstore.dp.ua и строительстве с обзорами материалов, инструментов и современных технологий. Узнайте, как правильно организовать строительные работы, выбрать подрядчиков и создать комфортное пространство.

Строительный портал https://aziatransbud.com.ua с актуальными статьями о строительстве домов, ремонте квартир, современных технологиях и строительных материалах. Полезные советы, обзоры оборудования, инструкции и рекомендации для частных застройщиков и профессионалов отрасли.

Идеи для интерьера https://bathen.rv.ua советы дизайнеров и актуальные тренды оформления помещений. Сайт поможет подобрать стиль, материалы и решения для ремонта квартиры, дома или коммерческого объекта.

Строительство домов https://zarechany.zt.ua ремонт квартир, инженерные системы и современные технологии — все это на одном информационном портале. Читайте экспертные статьи и находите практические решения для реализации своих проектов.

Все о ремонте https://intertools.com.ua и строительстве: от выбора фундамента до финишной отделки. Экспертные материалы, обзоры строительных технологий, рекомендации по подбору материалов и полезные советы для владельцев недвижимости.

Женский портал https://superwoman.kyiv.ua о красоте, здоровье, моде и саморазвитии. Полезные статьи, советы экспертов, идеи для вдохновения и актуальные тренды помогут сделать каждый день ярче, комфортнее и интереснее.

Все об автомобилях https://avto-drug.com на одном автопортале. Свежие новости, обзоры машин, сравнения моделей, советы по обслуживанию, ремонту и выбору автомобиля. Полезный ресурс для владельцев авто и будущих покупателей.

Все для мужчин https://hand-spin.com.ua в одном месте: здоровье, отношения, карьера, путешествия, технологии и активный образ жизни. Интересные статьи, обзоры и практические рекомендации для достижения личных и профессиональных целей.

Полезный строительный https://bastet.com.ua портал с материалами о строительстве, ремонте, дизайне интерьеров и благоустройстве территорий. Экспертные рекомендации, обзоры новинок рынка и практические решения для любых строительных задач.

Информационный автопортал https://autoinfo.kyiv.ua для водителей и автолюбителей. Обзоры автомобилей, новости производителей, рекомендации по уходу за машиной, выбору запчастей и безопасной эксплуатации транспортных средств.

Строительный интернет-портал https://esi.com.ua с полезной информацией для владельцев недвижимости, строителей и ремонтных специалистов. Инструкции, обзоры материалов, советы экспертов и новости строительной отрасли.

Полезный ресурс https://rkas.org.ua о ремонте и строительстве для тех, кто хочет создать комфортное и надежное жилье. Инструкции, экспертные советы, обзоры строительных материалов и практический опыт специалистов.

Ремонт и строительство https://intellectronics.com.ua информационный портал о современных технологиях, строительных материалах и практических решениях для дома. Полезные статьи, обзоры, инструкции и советы специалистов для успешной реализации проектов любой сложности.

Портал о строительстве https://fmsu.org.ua и ремонте с подробными руководствами, обзорами оборудования и строительных материалов. Узнавайте о новых технологиях, современных решениях и практическом опыте специалистов отрасли.

Современный строительный https://dki.org.ua портал с обзорами технологий, материалов и инструментов. Читайте статьи о строительстве частных домов, ремонте помещений, инженерных коммуникациях и эффективных решениях для комфортного проживания.

Строительство и ремонт https://keravin.com.ua для дома, квартиры и дачи. Полезные статьи о проектировании, отделке, инженерных коммуникациях, благоустройстве территории и современных решениях для комфортной жизни.

Информационный сайт https://kero.com.ua о ремонте и строительстве с рекомендациями по выбору материалов, организации работ и применению современных технологий. Полезный ресурс для частных застройщиков и профессионалов отрасли.

Полезный строительный https://quickstudio.com.ua блог с идеями для ремонта, обустройства дома и повышения комфорта. Читайте обзоры материалов, советы специалистов и вдохновляйтесь новыми проектами.

Ремонт и строительство https://sushico.com.ua от профессионалов: обзоры технологий, рекомендации по выбору материалов, советы по организации работ и полезная информация для владельцев домов, квартир и коммерческой недвижимости.

Портал о строительстве https://purr.org.ua домов, ремонте квартир и благоустройстве участков. Читайте статьи о строительных технологиях, дизайне интерьеров, выборе подрядчиков и современных тенденциях отрасли.

Ваш провідник у житті Луцька https://43000.com.ua новини міста, культурні події, афіша заходів, бізнес, освіта та корисні поради для мешканців і гостей. Уся важлива інформація про Луцьк в одному місці.

Современный портал https://rus3edin.org.ua о строительстве и ремонте с материалами по проектированию, отделке, утеплению, монтажу инженерных систем и благоустройству территории. Все необходимое для успешной реализации строительных проектов.

Строительные идеи https://texha.com.ua ремонтные решения и полезные советы для дома. Узнавайте о современных технологиях, надежных материалах, инженерных системах и способах сделать жилье комфортным, функциональным и долговечным.

Портал об автомобилях https://diesel.kyiv.ua и современных транспортных технологиях. Статьи о новых моделях, сравнительные обзоры, рекомендации по обслуживанию и полезная информация для каждого автомобилиста.

boat rental montenegro yacht charter in montenegro

Мир дизайна https://vineyardartdecor.com и интерьера с вдохновляющими проектами, экспертными рекомендациями и полезными статьями. Узнайте, как создать красивое, практичное и современное пространство для жизни и работы.

Ваш гид в мире ремонта https://tfsm.com.ua и строительства. Пошаговые инструкции, обзоры строительных материалов, советы мастеров и практические решения для ремонта квартир, строительства домов и благоустройства участков.

От фундамента до декора https://vodocar.com.ua все о строительстве и ремонте в одном месте. Актуальные статьи, экспертные рекомендации, обзоры новинок рынка и проверенные решения для частных и коммерческих объектов.

Мир женских интересов https://amideya.com.ua в одном информационном ресурсе. Читайте статьи о моде, здоровье, карьере, семье и путешествиях, находите полезные рекомендации и вдохновение на каждый день.

Современный портал https://zlochinec.kyiv.ua для мужчин о здоровье, саморазвитии, бизнесе и увлечениях. Практические рекомендации, актуальные новости и вдохновляющие истории для тех, кто стремится к новым достижениям.

Строительный журнал https://buildingtips.kyiv.ua для тех, кто строит, ремонтирует и обустраивает недвижимость. Полезные публикации о технологиях строительства, дизайне интерьеров, выборе подрядчиков и современных материалах.

Мир автомобилей https://auto-club.pl.ua в одном месте: автоновости, обзоры, рейтинги, советы по ремонту и обслуживанию. Следите за новинками автопрома, узнавайте о характеристиках моделей и тенденциях автомобильного рынка.

Все о современном https://dcsms.uzhgorod.ua доме: строительство, ремонт, интерьер и благоустройство. Экспертные статьи, обзоры материалов и полезные рекомендации для создания комфортного пространства для жизни.

Практический портал https://dsmu.com.ua о ремонте, строительстве и обустройстве жилья. Реальные советы, инструкции и обзоры помогут сократить расходы, повысить качество работ и добиться отличного результата.

Строительство без ошибок https://donbass.org.ua начинается здесь. Узнавайте о новых технологиях, популярных строительных материалах, особенностях ремонта и эффективных решениях для жилой и коммерческой недвижимости.

Pizza Venezia — Итальянская пицца в Москве https://pizza-venezia.ru быстрая доставка горячей пиццы, пасты, закусок и десертов. Свежие ингредиенты и классические рецепты.

Проблемы со здоровьем? семейный медицинский центр прием врачей различных специальностей, точная диагностика, профилактические обследования и индивидуальный подход к каждому пациенту. Забота о здоровье с использованием современных методов лечения.

На нашем сайте собраны мультфильмы онлайн бесплатно всех жанров и направлений – от свежих премьер до признанной классики, которые не теряют своей актуальности. Мы объединили на одной площадке большой каталог видеоконтента, чтобы каждый пользователь мог легко подобрать подходящий фильм для просмотра. Большинство материалов представлена в качестве HD, а рекламы здесь минимум, чтобы просмотр оставался комфортным. Каталог регулярно пополняется, добавляя свежие премьеры и популярные проекты, о которых часто упоминают поклонники кино.

детский летний лагерь волгоград https://letniy-lager.ru

The CS2 Pro https://counter-strike.ch portal features the latest Counter-Strike 2 news, live match results, tournament schedules, and analysis. Learn about professional scene events, team rankings, and the top stories from the world of CS2.

With Valorant Tracker valorant-fa you can learn about professional player settings, find the best aim, track ranks, and analyze match statistics. A useful tool for improving your skills and progressing more effectively in VALORANT.

Valorant Tracker valorant-th.com is your companion in the world of VALORANT. Professional player settings, the best crosshair codes, current ranks, match statistics, and detailed analytics will help you improve your gaming skills and climb the ranking ladder faster.

GTA 6 release date https://www.gta6-online.hu price, platforms, map, and all the information about one of the most anticipated games of recent years. Learn about the official release, available platforms, details about the world of Leonida and Vice City, new characters, gameplay features, and the latest news from Rockstar Games.

Everything about VALORANT valorant-bn.com in one place: professional settings, crosshair codes, ranks, player stats, and match analytics. Valorant Tracker helps you track your achievements, learn from the best players, and improve your gameplay.

Everything about sports nso-online for true fans. Watch live broadcasts, get match results in real time, read the latest news, analytical articles, tournament reviews, and follow the achievements of your favorite teams and players.

Play for free http://www.poki.hu right in your browser without installing any additional software. A huge selection of games across various genres: action, logic, sports, racing, simulation, and adventure. Find your favorite games and enjoy online gaming.

The 2025/26 La Liga https://www.laliga-tabella.hu standings feature up-to-date data for all teams in the Spanish league. Track points, matches played, wins, draws, and losses, as well as explore matchday results, game schedules, and season statistics.

UEFA Champions League 2025/26 https://uefa-bl.hu the latest standings, match schedule, results, and detailed tournament statistics. Follow the season, check live results, explore the playoff bracket, and find out about tickets for the final of Europe’s premier club competition.

The latest sports news http://www.nemzeti-sport-online.hu/ live streams, and competition results from around the world. Football, Formula 1, tennis, hockey, basketball, and other sports. Match schedules, team statistics, tournament highlights, and key daily events.

Как правильно сравнить несколько КП перед тем, как заказать продвижение сайта?

Как домашние животные реагируют на смену времён года и световой день?

Delicious – here: סוכנויות ליווי מאומתות

лента стальная гост купить https://lenta-stalnaya-moscow.ru

Expand at the link: סוכנויות ליווי עילית

Как Гео продвижение сайта помогает небольшому локальному бизнесу попасть в топ карт?

Подробности по ссылке: https://duxi-365.ru/montale/

Читать далее: https://vostok-perfumes.ru

Подробности на странице: https://svetasanders.com/2014/12/picture-polish-never-nude-cyan-honey.html

Подбор займ без отказа на карту начинается с внимательного анализа предложений, и специально для удобства пользователей создан наш проект. Мы собрали и регулярно проверяем информацию по 35 лицензированным МФО, которые осуществляют деятельность в соответствии с требованиями действующего законодательства и предлагают займы со ставкой не выше 0,8% в день. На одной странице можно сравнить сумму, срок, требования к заемщику, условия первого займа и скорость получения денег. После выбора нужного предложения вы можете подать заявку на займ онлайн на карту и получить до 30 000 рублей практически мгновенно. Многие компании обрабатывают заявки 24/7, а решение по анкете часто поступает в течение нескольких минут. Для оформления обычно достаточно паспорт, банковская карта и возраст от 18 лет.

Текущие рекомендации: https://frenchspeak.ru

электрик по вызову на дом https://electro-master-msk.ru

Хочешь клубнику? клубника Альбион свежие, спелые и ароматные ягоды по выгодным ценам. Сезонная клубника от проверенных поставщиков, оптовые и розничные продажи, быстрая доставка по городу и области.

Ремонт грузовых автомобилей https://minskdiesel.by в Минске? Сервис «Дизель Практик» вернёт технику в строй в кратчайшие сроки! Срочный ремонт, выездная диагностика, запчасти в наличии. Доверьтесь профессионалам с многолетним опытом — надёжность и прозрачность на каждом этапе.

нарколог на дому капельниц вызов врача нарколога на дом

вызвать нарколога выезд на дом нарколога

платный нарколог на дом недорого нарколог вызвать на дом

выезд нарколога на дом вызов нарколога цена

вызвать нарколога цена нарколог вызов на дом

NBA standings https://www.nbi-tabella.hu match results, game schedule, and the latest basketball season news. Follow conference standings, player stats, game results, the tournament schedule, and all the important events of the National Basketball Association.

The latest NBA nb1-tabella.hu standings with match results, schedule, and the latest basketball news. Learn about team and player achievements, track standings, explore statistics, and get highlights of the season’s most exciting games.

The 2025/26 Premier League http://www.premier-league-tabella.hu/ table, featuring the current standings, points totals, and match results. Follow the battle for the championship, European places, and league status. Game schedules, statistics, matchday overviews, and the latest season data are available.

NBA news http://www.nb2-tabella.hu/ game results, schedules, and the latest season standings. Get the latest information on teams, players, and the tournament, analyze statistics, and follow the championship race and playoff progress.

The latest Liverpool news liverpool meccs fixtures, and season results. Get up-to-date information on team performances, lineup changes, player achievements, match statistics, and key events in English and European football.

Liverpool’s league table http://www.liverpool-tabella.hu/ shows the team’s current standings, points earned, and form. Follow the team’s latest match results, win/loss statistics, season dynamics, and the battle for top spots in the standings.

Нужен надежный склад https://www.0412.ua/list/455589 для вашего бизнеса? Предлагаем ответственное хранение товаров, паллет, оборудования и грузов. Современные складские комплексы, круглосуточная охрана, учет остатков и оперативная обработка заказов. Оптимизируйте логистику и сократите расходы вместе с нами!

Podcast studio Bali https://studiosnearyou.com/blog/best-podcast-studio-bali/ — a guide comparing the 5 best by location, hourly rate and what you get for the money, from budget rooms to full video production. Honest picks, real 2026 rates, no fluff.

тату салон спб рядом сколько стоит сделать тату

салон тату и пирсинга татуировка сделать спб

тату салон рядом сделать тату цена

Магазин кофемашин https://incoffeein.by в Минске с большим выбором кофе, чая и сопутствующих товаров. Подберите оборудование для дома, офиса или кафе, закажите качественный кофе в зернах и листовой чай, получите профессиональную консультацию и быструю доставку.

Как правильно сравнить несколько КП перед тем, как заказать продвижение сайта?

Как домашние животные реагируют на запах незнакомой еды на кухне?

Today’s highlights are here: Moab and Edom

Самое полезное для вас: https://mamamia-shop.ru

Все подробности: https://aromline.ru/index.php?productID=14171

Right now: https://siliceanworks.click/

Today’s Top Stories: https://unquodlayer.digital

Ударно-волновая терапия https://novogireevo-klinika.ru в Пушкино — эффективный метод лечения хронической боли, воспалений сухожилий и суставов. Консультация врача, подбор курса процедур, современное оборудование, комфортные условия и профессиональный подход к восстановлению здоровья.

All the details at the link: https://siliquaco.digital

Action tips: https://tampontrust.digital

Аренда квартир в СПб https://arenda-kvartir78.ru на длительный срок и посуточно. Большой выбор квартир в разных районах Санкт-Петербурга, проверенные объявления, удобный поиск по цене, площади и расположению. Найдите комфортное жилье без лишних сложностей.

Драфт-сюрвей https://eurogal-surveys.ru независимый расчет массы груза по осадке судна перед погрузкой и после выгрузки. Точные измерения, международные методики, квалифицированные сюрвейеры, официальные отчеты и контроль количества груза для морских перевозок.

Лучший лагерь в подмосковье с английским языком — идеальный вариант для родителей из Москвы. Удобное расположение, чистый воздух, комфортные корпуса и сильная языковая программа. Дети отдыхают рядом с домом и заметно подтягивают английский за смену.

Квартиры в новостройках https://novostroyka78.ru Курортного района СПб с удобным поиском по цене, площади и срокам сдачи. Современные жилые комплексы, экологичная локация, близость парков и Финского залива, выгодные ипотечные программы и предложения от застройщиков.

seo оптимизация и продвижение сайтов seo оптимизация и продвижение сайтов .

Обновлено сегодня: https://epcomp.ru

Магазин бытовой химии https://himiya-v-dom.ru с большим выбором товаров для дома. Моющие и чистящие средства, стиральные порошки, гели, средства для кухни и ванной, товары для уборки, личной гигиены и ухода за домом по выгодным ценам.

Изучай английский онлайн — современный способ освоить язык из любой точки мира. В YES Center занятия проходят в живом формате с преподавателем, поэтому вы быстро преодолеете языковой барьер и начнёте говорить. Попробуйте бесплатный вводный урок.

Создание сайтов на конструкторе или в студии — что выбрать для небольшого проекта?

Company sales funnel web2app.tools product documentation

Обновлено сегодня: https://firstremont.ru

наркологическая помощь на дому частная наркологическая помощь

Последние изменения: https://remontpodomy.ru

Все самое свежее здесь: https://novstroi-nn.ru

проверенный нарколог на дом https://www.narkolog-na-dom-vizov.ru

Центр охраны труда https://www.unitalm.ru “Юнитал-М” проводит обучение по охране труда более чем по 350-ти программам, в том числе по электробезопасности и пожарной безопасности. А также оказывает услуги освидетельствования и испытаний оборудования и аутсорсинга охраны труда.

Качественный сервис бытовой техники: сервисы ремонта стиральных машин воронеж. Предлагаем в день обращения. Честные цены. Звоните, поможем вернуть технику к жизни!

Давно искали кухни на заказ ? https://activ-service.ru. Посоветовали знакомые, и мы довольны. Сделали бесплатный замер, нарисовали 3D-проект . Даже мелочи обсудили — розетки, вытяжку, подсветку. Собрали аккуратно, без мусора и грязи . Качество — на уровне дорогих салонов. В общем, если планируете ремонт — заходите на сайт, не пожалеете

Топовая онлайн школа английского — для тех, кто хочет заниматься в комфортном темпе. В YES Center вы выберете уровень и формат, а опытные педагоги помогут заговорить уверенно. Гибкое расписание подойдёт даже при плотном графике работы или учёбы.

Летний лагерь с английским языком в YES Center — это полное погружение в среду. Дети общаются, играют и учатся одновременно, поэтому новые слова и фразы запоминаются легко, без зубрёжки. Опытные педагоги поддерживают каждого. Бронируйте места заранее.

Летний лагерь с английским языком в YES Center — это полное погружение в среду. Дети общаются, играют и учатся одновременно, поэтому новые слова и фразы запоминаются легко, без зубрёжки. Опытные педагоги поддерживают каждого. Бронируйте места заранее.

займ оформить https://zaym-nakartu.ru

Операционная система GNU https://www.gnu.org свободная программная платформа с открытым исходным кодом, лежащая в основе многих современных дистрибутивов. Узнайте об истории проекта, компонентах системы, лицензии GNU GPL, возможностях и преимуществах свободного ПО

Играйте в Sultan Casino KZ sultan-casino.clients.site и пользуйтесь всеми возможностями платформы.

Подробности по ссылке: https://comein.su

Полная версия по ссылке: https://frenchspeak.ru/letter/%d0%9e%d0%a8

Все подробности: https://jo-malone-london.ru/body/Grapefruit_shower_gel/

Может ли малый бизнес позволить себе seo под ключ или это только для крупных?

Хотите учиться, не выходя из дома? онлайн курсы по английскому от YES Center подходят и взрослым, и детям. Современная платформа, продуманная программа и обратная связь от педагога делают обучение эффективным и комфортным. Старт групп каждый месяц.

Актуальные события https://sin180.ru в мире и России: последние новости политики, экономики, общества, технологий, спорта и культуры. Следите за важными событиями, аналитикой, официальными заявлениями, репортажами и обновлениями в режиме реального времени.

Все о ремонте https://stroymaster-base.ru и строительстве дома в одном месте. Руководства по возведению фундамента, кровли, отделке, инженерным системам, выбору материалов, инструментов и современным технологиям строительства для частных домов.

Медицинский портал https://registratura24.com с полезной информацией о заболеваниях, симптомах, диагностике, лечении и профилактике. Статьи врачей, справочник лекарств, советы по здоровью, медицинские новости и материалы для пациентов.

Мировые новости https://trawa-moscow.ru в режиме реального времени: политика, экономика, технологии, наука, спорт и культура. Следите за главными событиями дня, международной аналитикой, эксклюзивными материалами и важными изменениями по всему миру.

Блог интересных новостей https://uploadpic.ru о событиях в мире, науке, технологиях, культуре, истории и необычных открытиях. Читайте свежие публикации, удивительные факты, аналитические материалы и самые обсуждаемые темы со всего мира.

Все о здоровье https://noprost.com в одном месте. Медицинский портал с описанием болезней, симптомов, анализов, лекарственных препаратов и современных методов лечения. Читайте экспертные статьи, советы врачей и актуальные медицинские новости.

Как выстроить внутреннюю перелинковку, когда ведётся SEO продвижение молодого сайта?

Все про сад https://tepli4ka.com огород и приусадебный участок: выращивание овощей, фруктов и цветов, уход за растениями, борьба с вредителями, сезонные работы, полезные советы, современные агротехнологии и идеи для благоустройства участка.

Энциклопедия о похудении https://med-pro-ves.ru с проверенной информацией о правильном питании, снижении веса, физических нагрузках и здоровом образе жизни. Полезные статьи, советы экспертов, программы похудения, рецепты и рекомендации для достижения устойчивого результата.

Советы по строительству https://lesovikstroy.ru и ремонту для дома, квартиры и дачи. Пошаговые инструкции, выбор строительных материалов, современные технологии, полезные рекомендации специалистов и идеи для качественного выполнения любых ремонтных работ.

Как seo оптимизация сайта влияет на позиции в мобильной выдаче?

услуги охраны объекта организация охранных услуг

чоп охрана https://uslugi-ohrany.kz

Все про ремонт https://geekometr.ru полезные советы, пошаговые руководства и идеи для обновления квартиры или дома. Статьи о ремонте стен, пола, потолка, ванной, кухни, выборе материалов, инструментов и современных технологиях отделки.

Everything for Minecraft https://topminecraftworldseeds.com in one place: mods, skins, maps, texture packs, and the best seeds for survival, creativity, and adventure. Collections of popular add-ons, installation instructions, updates, and secure downloads for different versions of the game.

Everything for Minecraft http://www.topminecraftworldseeds.com/ in one place: mods, skins, maps, texture packs, and the best seeds for survival, creativity, and adventure. Collections of popular add-ons, installation instructions, updates, and secure downloads for different versions of the game.

Все для Minecraft https://www.minecraft-files.ru в одном месте: моды, скины, карты, текстуры и полезные загрузки для Java и Bedrock Edition. Находите лучшие дополнения, следите за обновлениями, используйте подробные гайды и безопасно скачивайте игровой контент.

Everything for Minecraft https://topminecraftworldseeds.com in one place: mods, skins, maps, texture packs, and the best seeds for survival, creativity, and adventure. Collections of popular add-ons, installation instructions, updates, and secure downloads for different versions of the game.

Trusted store NPPRTeamShop https://npprteamshop.com/en/email-accounts/proton/ maintains the widest catalog of ad-ready accounts for scaling campaigns without downtime. The NPPRTeamShop team stands by every listing with responsive Telegram support and replacement coverage across all product categories. The most successful media buying teams share one trait: they invest in quality infrastructure before they invest in ad spend.

Магазин с фокусом на качество NPPR TEAM SHOP https://npprteamshop.com/yandex/ запускает многоступенчатую верификацию каждого аккаунта в защиту интересов покупателя. Прогретые профили с NPPRTEAMSHOP стабильно превосходят свежие регистрации по качеству показа и обходу чекпоинтов. Клиенты NPPR Team Shop масштабируются быстрее, потому что стартуют с верифицированных профилей и персональной поддержки.

Everything for Minecraft http://www.topminecraftworldseeds.com/ in one place: mods, skins, maps, texture packs, and the best seeds for survival, creativity, and adventure. Collections of popular add-ons, installation instructions, updates, and secure downloads for different versions of the game.

Качественный сервис бытовой техники: ремонт стиральных машин волгоград. Выполняем на совесть. Опытные специалисты. Звоните, поможем вернуть технику к жизни!

Хочешь сайт на тильде? читать материал лендинги, сайты услуг, интернет-магазины, корпоративные проекты и портфолио с адаптивным дизайном, SEO-подготовкой, интеграциями и удобной системой управления контентом.

Everything for Minecraft https://topminecraftworldseeds.com/ in one place: mods, skins, maps, texture packs, and the best seeds for survival, creativity, and adventure. Collections of popular add-ons, installation instructions, updates, and secure downloads for different versions of the game.

Жіночий журнал https://womandb.com про красу, моду, здоров’я, стосунки, сім’ю та стиль життя. Читайте корисні поради, актуальні тренди, рецепти, психологію, догляд за собою та цікаві статті для сучасних жінок.

Последние одесские новости https://dverikupe.od.ua и происшествия за сегодня: оперативная информация о событиях в Одессе и области, ДТП, происшествиях, работе городских служб, политике, экономике, обществе, погоде и других важных новостях дня.

Повышение квалификации https://kursdpo.ru и переподготовка для работников образования с учетом актуальных требований. Курсы для учителей, воспитателей, преподавателей, психологов, логопедов и руководителей образовательных учреждений в удобном формате обучения.

Everything for Minecraft https://topminecraftworldseeds.com/ in one place: mods, skins, maps, texture packs, and the best seeds for survival, creativity, and adventure. Collections of popular add-ons, installation instructions, updates, and secure downloads for different versions of the game.

Останні новини Києва https://xxl.kyiv.ua головні події столиці, оперативні повідомлення, міські новини, ДТП, надзвичайні ситуації, політика, економіка, культура, спорт і життя міста. Слідкуйте за актуальною інформацією та важливими подіями щодня.

Все про діабет https://pro-diabet.in.ua симптоми, причини, діагностика, лікування та профілактика. Корисні статті про цукровий діабет 1 і 2 типу, контроль рівня глюкози, харчування, спосіб життя та сучасні методи терапії.

сколько стоит автовышка аренда https://автовышкичебоксары.рф

Withdrawal delays, failed transactions, account issues — we cover every headache scenario.

Everything for Minecraft http://www.topminecraftworldseeds.com/ in one place: mods, skins, maps, texture packs, and the best seeds for survival, creativity, and adventure. Collections of popular add-ons, installation instructions, updates, and secure downloads for different versions of the game.

Кремация https://krematsiya-moskva.ru процесс сжигания тела человека после его смерти, который в последнее время становится все более популярным в Москве. Многие люди выбирают этот способ прощания со своими близкими по различным причинам: от личных убеждений до практических соображений, связанных с захоронением.

Are you leveling up your character? rank boost service BooStRiders is a game boosting and currency marketplace: hire verified boosters for rank boost, coaching and clears, or buy WoW Gold, PoE Orbs and Diablo 4 Gold. Every order is protected by escrow, so you only pay when the work is done — trusted by 50,000+ gamers.

Играешь онлайн? услуги бустинга в играх гриндить рейтинг, золото и достижения вручную — это сотни часов. BooStRiders — маркетплейс бустинга и игровой валюты: можно нанять проверенных бустеров для прокачки рейтинга, коучинга и закрытия контента или купить WoW Gold, PoE Orbs и Diablo 4 Gold. Каждая

Заказываешь товары или услуги? отзывы о компаниях Compasly — платформа отзывов, где можно читать проверенные отзывы о компаниях, сравнивать TrustScore и делиться собственным опытом. От электроники и финансов до игр и одежды — легко понять, каким компаниям действительно можно доверять.

Занимаешься сайтами? отслеживание позиций сайта чтобы видеть реальный эффект продвижения, важно ежедневно отслеживать позиции сайта в Google и Яндексе, а не проверять их руками. Site Metrics Tool подключается к Google Search Console и Яндекс.Вебмастеру и в реальном времени показывает динамику позиций, трафика и SEO-метрик — с отчётами, где сразу видно, что растёт, а что проседает.

Хочешь узнать совместимость? совместимость по дате рождения понять, подходите ли вы друг другу, помогает не общий гороскоп по знаку, а разбор по дате рождения обоих партнёров. На Luore можно бесплатно рассчитать совместимость по дате рождения и получить натальную карту с расшифровкой: сервис показывает сильные стороны пары, зоны напряжения и советы, как сделать отношения гармоничнее.

Играешь в WOW? купить золото WoW в магазине Мурловиль можно быстро и безопасно купить золото WoW, оформить подписку Game Time, заказать прокачку персонажа или буст рейдов и Мифик+. Актуально для Midnight, Classic и MoP, с гарантией и живой поддержкой — экономит десятки часов гринда.

Занимаешься рассылками? сервис email-рассылок Sendersy — платформа email-рассылок со своим SMTP: массовые и транзакционные письма через API, визуальный редактор, автоматизация и аналитика открытий. Данные хранятся в ЕС и РФ, а первые 200 писем в месяц — бесплатно, чтобы протестировать доставляемость.

путешествие в будву https://puteshestvie-v-budvu.com

Любишь играть в WOW? прокачка персонажа WoW копить золото и проходить сложный контент в World of Warcraft вручную — долго. В магазине Мурловиль можно быстро и безопасно купить золото WoW, оформить подписку Game Time, заказать прокачку персонажа или буст рейдов и Мифик+. Актуально для Midnight, Classic и MoP, с гарантией и живой поддержкой — экономит десятки часов гринда.

медицинская книжка рядом как получить санитарную книжку

Последние обновления: https://elicebeauty.com/parfyumeriya/elitnaya-parfyumeriya/adidas-victory-league.html

Everything for Minecraft https://topminecraftworldseeds.com in one place: mods, skins, maps, texture packs, and the best seeds for survival, creativity, and adventure. Collections of popular add-ons, installation instructions, updates, and secure downloads for different versions of the game.

Обновлено сегодня: https://slovarsbor.ru/c/%D0%B1%D0%B4/

SEO продвижение под ключ — нужен ли на стороне клиента технический специалист?

Самое важное сегодня: https://elicebeauty.com/parfyumeriya/filter/_m223_m303/

Последние публикации: https://moscow.cataloxy.ru/node22_zdorove_9456/sovremennaya-stomatologiya-i-ee-preimuschestva.htm

Расширенная статья здесь: https://prigotovim-v-multivarke.ru/lechenie-zubov-ot-straha-do-zdorovya-kak-sohranit-svoyu-ulybku.html

Полная версия по ссылке: https://l-parfum.ru/brands/duhi-optom-v-simferopole/

Самое важное сегодня: https://spainslov.ru/site/word/word/%D0%9A%D0%90%D0%9B%D0%98%D0%9A%D0%90

The captain who scores faster as the innings progresses — strike rate improvers as fantasy assets.

Узнать больше здесь: https://l-parfum.ru/catalog/paco-rabanne/ultraviolet-w/

Только что опубликовано: https://aromline.ru/index.php?productID=4521

Узнать больше здесь: https://svetasanders.com/2014/04/

Текущие рекомендации: https://mumbook.ru

Наша лучшая подборка: https://aromatmasla.ru

Обновления по теме: https://pcosmetik.ru

Текущие рекомендации: https://rikoremont.ru

Нові новини сьогодні украинские новости політика, економіка, суспільство, події, культура, технології, спорт та події регіонів. Оперативні публікації, аналітичні матеріали, інтерв’ю, репортажі та важливі події України щодня.

Читать больше на сайте: https://germandic.ru/%d0%b0%d0%bd%d0%b3%d0%b8%d0%bd%d0%b0

The best of the best: https://guides.co/g/businesses-review/670585

The best AI-powered https://clothes-remover-ai.it.com clothing removal services of 2026, powered by updated, next-generation neural networks. Unique photo-based undressing algorithms ensure impeccable detail, HD resolution, and a complete absence of distortion.

Как структура сайта влияет на seo продвижение молодого сайта?

Лучший выбор дня: кбжу блюда по фотографии

Оргстекло и акрил url в мебели создают эффект невесомости. Прозрачные стулья, столики, полки. Они не загромождают пространство, идеальны для маленьких комнат. Акрил прочнее стекла, не бьется. Легко царапается, но полируется. Современный футуристичный вид. Сочетается с любыми стилями. Так комфортнее.

аренда авто в пхукете цены аренда авто карон пхукет

ggbet right now https://ggbet-top.pl/ggbet/

аренда авто на пхукете на месяц аренда авто с водителем пхукет

ggbet official login https://ggbet-top.pl/ggbet/

Ищешь ключ TF2? https://tf2lavka.net выберите подходящее предложение и оформите покупку за несколько минут. Быстрая доставка, безопасная оплата, удобный интерфейс и актуальная информация о наличии ключей.

Все про ремонт https://geekometr.ru для начинающих и опытных мастеров. Статьи о черновой и чистовой отделке, ремонте кухни, ванной, спальни и других помещений, выборе материалов, инструментов, освещения и современных дизайнерских решений.

Включает ли SEO продвижение под ключ работу с репутацией и внешними площадками?

Революция в Tilda https://u11.ru/blog/tpost/revoluciya-v-tilda-obzor-vibe-block/ Обзор нового Vibe-Block (Вайб-блок) с искусственным интеллектом

Лучшие в РФ тур в карелию на 1 день экскурсионные программы, отдых на природе, путешествия к водопадам, озерам, островам и национальным паркам. Выбирайте туры выходного дня и многодневные маршруты с комфортным размещением и опытными гидами.

Ищешь ключ TF2? tf2 ключи выберите подходящее предложение и оформите покупку за несколько минут. Быстрая доставка, безопасная оплата, удобный интерфейс и актуальная информация о наличии ключей.

Карго рейтинг https://рейтинг-карго-компаний.рф по доставке из Китая в Москву поможет сравнить логистические компании, условия перевозки, сроки, стоимость и отзывы клиентов. Выбирайте надежных перевозчиков, изучайте рейтинги, обзоры и рекомендации для безопасной доставки грузов.

Доставка грузов https://delchina.ru из Китая в Россию с подбором оптимального маршрута и способа перевозки. Авто, железнодорожные, морские и авиаперевозки, таможенное оформление, консолидация грузов, страхование, сопровождение и контроль на всех этапах доставки.

Копицентр «Копирыч» https://kopirych.by профессиональный партнер для тех, кому нужна качественная печать фото в городе минск и по всей Беларуси.

Производство шпона https://opus2003.ru и продажа натурального шпона в Москве. В наличии широкий выбор пород древесины, материалы для мебели и интерьеров, изготовление под заказ, выгодные цены, помощь в подборе, оперативная доставка и консультации специалистов.

Доставка дизельного топлива https://neftegazlogistica.ru в Москве для строительных площадок, предприятий, котельных, автопарков и частных клиентов. Оперативные поставки, топливо стандарта Евро-5, удобные объемы, сопровождение документами и доставка по согласованному графику.

Внешние специалисты https://skillstaff2.ru ИП и самозанятые для ваших проектов. Подберите опытных исполнителей для разработки, маркетинга, дизайна, бухгалтерии, IT, продаж и других задач. Гибкое сотрудничество, быстрое подключение и профессиональная поддержка бизнеса.

Колодцы под ключ https://digwel.ru в Московской области с полным комплексом работ: поиск водоносного слоя, копка, установка бетонных колец, герметизация, обустройство и ввод в эксплуатацию. Работаем в Москве и Подмосковье, соблюдаем сроки и используем качественные материалы.

Инженерные изыскания https://geo163.ru в Москве для строительства жилых, коммерческих и промышленных объектов. Выполняем геодезические, геологические, экологические и гидрометеорологические исследования, готовим технические отчеты и сопровождаем проект.

Может ли неправильная seo оптимизация сайта привести к санкциям поисковика?

Рейтинг поставщиков дизтоплива https://рейтинг-поставщиков-дизтоплива.рф поможет сравнить компании по качеству топлива, ценам, условиям поставки, скорости доставки и отзывам клиентов. Изучайте обзоры, оценки и выбирайте надежного поставщика для бизнеса и частных нужд.

Рейтинг грунтовых компаний https://рейтинг-грунтовых-компаний.рф поможет выбрать надежного поставщика плодородного, растительного, планировочного и других видов грунта. Сравнивайте цены, условия доставки, ассортимент, отзывы клиентов и качество обслуживания в одном каталоге.

купить готовые результаты анализов купить готовые анализы

Рейтинг геодезических https://инженерные-изыскания-рейтинг.рф и кадастровых компаний Москвы с актуальной информацией о стоимости услуг, опыте работы, сроках выполнения и репутации исполнителей. Сравнивайте предложения и находите надежных специалистов для вашего проекта.

montenegro vacation driving map rent a car in budva

Решили купить квартиру? подробнее проверим документы и застройщика, оценим юридическую чистоту объекта и безопасно сопроводим сделку на всех этапах — от выбора недвижимости до регистрации права собственности.

Как продвижение сайта в поисковых системах связано с юзабилити?

bergamo airport transfer https://transferme24.com

перевод английский на русский https://myleadgen.ru

Хочешь проверить разметку сайта? https://schema-org-check.ru сервис анализирует структурированные данные, выявляет ошибки и предупреждения, помогает проверить JSON-LD, Microdata, RDFa и улучшить корректность отображения информации в поисковых системах.

удаление ветвей деревьев удаление старых деревьев

ии для карточек товара вб ии для создания карточек товара

дизайн интерьера спб студия дизайна интерьеров спб

удаление деревьев цена сколько стоит спил дерева

карточка товара озон цена ии для создания карточек товара на озон

дизайн проект купить заказать дизайн проект в спб

Нужна автовышка? автовышка чебоксары для любых высотных работ: монтаж, обслуживание зданий, мойка фасадов, обрезка деревьев, ремонт кровли и наружного освещения. Различная высота подъема, оперативная подача и гибкие тарифы.

Read More: 90 年代色情片

Свечи и подсвечники formulacomfort.ru создают магию вечера. Ароматические свечи расслабляют. Пламя успокаивает и медитирует. Подсвечники из металла, стекла, дерева. Группировка свечей разной высоты эффектна. Безопасность: не оставляйте без присмотра. Электрические свечи безопасны для Это удобно.

ии дневник питания как отправить дневник питания тренеру

Today’s Focus: 色情 異族

Лучший выбор дня: https://russkoitalslovar.ru/%d0%b0%d0%b1%d0%b1%d0%b0%d1%82

self-drive itinerary for montenegro https://www.montenegro-road-trip.me

Ежедневный обзор: https://moy-parfum.ru/products/jose-eisenberg-122053/

Расширенный обзор: https://pobedimautism.ru

Если вы давно искали сколько стоит автошкола в иркутске где сочетаются доступная стоимость, качественное обучение и внимательное отношение к каждому ученику, значит вы попали по адресу. Вас ждут опытные инструкторы, современный автопарк и удобный график занятий. Теорию можно изучать очно или дистанционно, а практические занятия проходят в удобное для вас время. Это именно тот вариант, который выбирают будущие водители.

Полная версия статьи: https://1citywomen.ru/zdorove/esli-xochesh-dozhit-do-100-let-nepravilnoe-pitanie-prichina-rannej-smertnosti-i-xronicheskij-zabolevanij-uveryaet-nobelevskij-laureat/

Все подробности по ссылке: https://frenchspeak.ru/%D1%8D%D0%B2%D0%B5%D0%BD%D0%BA%D0%B8%D0%B9%D0%BA%D0%B0

Читать расширенную версию: https://vgarderobe.ru

Только лучшие материалы: https://1citywomen.ru/zdorove/sekrety-molodosti-produkty-bogatye-antioksidatnami/

Текущие рекомендации: https://1citywomen.ru/zdorove/vrachi-preduprezhdayut-etim-veshham-ne-mesto-vozle-vashej-krovati/

Перед покупкой стоит обратить внимание на гарантию, качество сборки и возможность модернизации системы. Подробнее — готовые пк купить.

дизайн карточек товара ai создание карточек

агентство по выкупу недвижимости продать квартиру с долгами по кредитам

Узнать больше здесь: https://vgarderobe.ru/zhenskaya-odezhda-ajc-bc-177.html

Последние обновления: https://archeagewiki.ru/index.php?title=%d0%a1%d0%bb%d1%83%d0%b6%d0%b5%d0%b1%d0%bd%d0%b0%d1%8f:%d0%92%d1%85%d0%be%d0%b4&returnto=%d0%91%d0%b8%d1%80%d1%8e%d0%b7%d0%be%d0%b2%d1%8b%d0%b5+%d0%b4%d0%b6%d0%b8%d0%bd%d1%81%d1%8b&returntoquery=%252f%25d0%2591%25d0%25b8%25d1%2580%25d1%258e%25d0%25b7%25d0%25be%25d0%25b2%25d1%258b%25d0%25b5_%25d0%25b4%25d0%25b6%25d0%25b8%25d0%25bd%25d1%2581%25d1%258b%3d&type=signup

Читать больше на сайте: https://elicebeauty.com/makiyazh/?sort=p.viewed&order=asc

Обновления по теме: https://aromline.ru/index.php?productid=179

получение медицинской справки купить справку с доставкой

Ковролин в спальне formulacomfort.ru дарит уют. Мягкий ворс под ногами утром. Теплоизоляция и звукопоглощение. Широкий выбор цветов и текстур. Синтетический ковролин износостоек. Натуральный (шерсть) дорог и капризен. Требует частой чистки пылесосом. Аллергикам стоит быть осторожными.. Это удобно.

центр медицинских справок https://spravki-spb-kupit.ru

первый микрозайм на карту рефинансирование микрозаймов

Самостоятельная сборка подходит далеко не каждому пользователю, особенно без соответствующего опыта. Именно поэтому востребована готовая сборка пк, где все комплектующие уже установлены и проверены. Это удобный вариант для тех, кто ценит свое время.

Спортивно-новостной https://xx-football.com блог для настоящих болельщиков. Оперативные новости спорта, обзоры соревнований, прогнозы, статистика, достижения спортсменов, расписание турниров и самые обсуждаемые события мирового спорта.

Актуальная новостная https://cenznet.com лента Украины с проверенной информацией о главных событиях страны и мира. Читайте новости политики, бизнеса, финансов, общества, науки, технологий, спорта и культуры без лишней информации.

Будьте в курсе https://xx-centure.com.ua главных событий Украины и мира. Свежие новости политики, экономики, общества, технологий, спорта, культуры, происшествий, аналитика, интервью и репортажи с ежедневным обновлением.

Последние новости https://gau.org.ua Украины 24/7: политика, экономика, бизнес, общество, регионы, международные события, технологии, культура, спорт и происшествия. Только актуальная информация и важные события дня.

Информационный портал https://gromrady.org.ua Украины с оперативной лентой новостей, аналитическими статьями, эксклюзивными материалами, мнениями экспертов и обзорами самых обсуждаемых событий в стране и за рубежом.

Читайте самые важные https://infotolium.com новости Украины, следите за мировыми событиями, изменениями в экономике, политике, технологиях, здравоохранении, образовании, культуре, спорте и общественной жизни.

Независимый новостной https://newsportal.kyiv.ua портал Украины с оперативной информацией о событиях в стране и мире. Политика, экономика, общество, финансы, бизнес, происшествия, технологии и самые обсуждаемые темы дня.

Ежедневные новости https://lentanews.kyiv.ua Украины и мира, аналитика, расследования, интервью, фоторепортажи и обзоры. Узнавайте первыми о главных событиях, решениях властей, изменениях законодательства и международной повестке.

Главные новости https://uamc.com.ua Украины в одном месте. Свежие публикации о политике, экономике, международных отношениях, региональных событиях, науке, технологиях, культуре, спорте и жизни общества.

Автомобильный портал https://orion-auto.com.ua с последними новостями автоиндустрии, обзорами новых моделей, тест-драйвами, советами по ремонту и обслуживанию, сравнениями автомобилей, правилами эксплуатации, технологиями и полезными материалами для водителей.

Provide predictions in various formats including win probabilities, score ranges, and margin predictions.

Последние новости https://viewport.com.ua автомобильной индустрии, обзоры легковых автомобилей, электромобилей и коммерческого транспорта, рекомендации по обслуживанию, ремонту, покупке, продаже, страхованию и эксплуатации автомобилей.

Все об автомобилях https://prestige-avto.com.ua на одном портале: свежие автоновости, тест-драйвы, обзоры кроссоверов, седанов и внедорожников, советы по выбору автомобиля, ремонту, техническому обслуживанию, тюнингу и эксплуатации в любое время года.

Автомобильный портал https://tuning-kh.com.ua для владельцев и будущих покупателей авто. Новости рынка, обзоры машин, тест-драйвы, советы по эксплуатации, ремонту, диагностике, выбору запчастей, шин, масел и аксессуаров, а также экспертная аналитика.

Строительный портал https://inox.com.ua с актуальными новостями, технологиями, обзорами материалов, инструкциями по строительству, ремонту, отделке, инженерным системам, благоустройству участка и полезными советами для дома и дачи.

Читайте актуальные https://reuth911.com новости автомобильного мира, обзоры новых моделей, сравнительные тесты, рекомендации по покупке, ремонту, страхованию, регистрации, уходу за автомобилем и безопасному вождению для начинающих и опытных водителей.

Все о строительстве https://interiordesign.kyiv.ua и ремонте в одном месте. Полезные статьи о выборе строительных материалов, современных технологиях, проектировании, отделке, инженерных коммуникациях, инструментах и обустройстве загородного дома.

Информационный строительный https://sovetik.in.ua портал для частных застройщиков и специалистов. Новости отрасли, обзоры материалов, пошаговые инструкции, советы по строительству домов, ремонту квартир, утеплению, кровле и фасадным работам.

Женский портал https://family-site.com.ua о красоте, здоровье, моде, отношениях, семье, психологии, материнстве, карьере и саморазвитии. Полезные статьи, советы экспертов, идеи для вдохновения и актуальные тренды для современной женщины.

Все для женщин https://femaleguide.kyiv.ua в одном месте: уход за собой, здоровье, мода, стиль, макияж, питание, фитнес, отношения, воспитание детей, путешествия, рецепты, психология и полезные советы на каждый день.

Женский портал https://feminine.kyiv.ua с ежедневными публикациями о красоте, здоровье, модных тенденциях, правильном питании, уходе за кожей и волосами, семейной жизни, карьере, хобби и гармонии в повседневной жизни.

Семейный портал https://geog.org.ua о детях, воспитании и развитии. Читайте рекомендации специалистов, находите развивающие игры, идеи для занятий, советы по здоровью, обучению, питанию и организации интересного семейного досуга.

Читайте статьи https://girl.kyiv.ua о женском здоровье, красоте, стиле, отношениях, материнстве, саморазвитии, психологии, кулинарии, путешествиях и уюте в доме. Только полезные материалы и практические рекомендации.

Информационный портал https://fines.com.ua для женщин, где собраны советы экспертов, модные тренды, рекомендации по здоровью, обзоры косметики, идеи для дома, рецепты, лайфхаки и материалы о саморазвитии.

Онлайн-журнал https://mirlady.kyiv.ua для женщин с актуальными статьями о моде, красоте, здоровье, семье, детях, фитнесе, правильном питании, косметике, карьере, вдохновении и современных тенденциях.

Женский портал https://nicegirl.kyiv.ua для тех, кто ценит красоту, здоровье и комфорт. Полезные советы по уходу за собой, обзоры косметики, идеи образов, секреты гармоничных отношений, домашнего уюта и активного образа жизни.

Читайте полезные https://mr.org.ua материалы о строительстве домов, ремонте квартир, выборе строительных материалов, инженерных системах, дизайне интерьера, благоустройстве участка, современных технологиях и профессиональных строительных решениях.

Строительный портал https://smallbusiness.dp.ua с практическими рекомендациями по строительству, ремонту и отделке. Обзоры инструментов, материалов, оборудования, инженерных систем, технологии монтажа, советы специалистов и строительные лайфхаки.

Все для строительства https://valkbolos.com дома и ремонта квартиры: статьи, инструкции, обзоры материалов, советы по выбору инструментов, монтажу инженерных коммуникаций, утеплению, кровельным и отделочным работам.

Актуальная информация https://vitamax.dp.ua о строительстве, ремонте и благоустройстве. Новости отрасли, технологии, строительные материалы, проекты домов, советы по эксплуатации зданий, инженерным решениям и организации строительных работ.

Портал о строительстве https://stroy-portal.kyiv.ua с ежедневными публикациями о современных технологиях, ремонте, проектировании, выборе материалов, строительной технике, инструментах, ландшафтном дизайне и обустройстве участка.

Все важные события https://novosti24.com.ua Украины и мира в удобном формате. Новости бизнеса, финансов, политики, общества, транспорта, науки, медицины, культуры, спорта и других сфер с ежедневным обновлением материалов.

Следите за главными https://avtomobilist.kyiv.ua событиями автомобильного рынка. Новости производителей, обзоры новых моделей, экспертные статьи, тест-драйвы, рейтинги автомобилей, советы по ремонту, обслуживанию и безопасной эксплуатации.

Следите за новостями https://prp.org.ua Украины онлайн: оперативная информация, аналитика, интервью, обзоры, комментарии экспертов и репортажи о политике, экономике, международных событиях, технологиях и общественной жизни.

Портал об автомобилях https://autonovosti.kyiv.ua с полезными статьями для каждого водителя. Новинки автопрома, тест-драйвы, сравнения моделей, лайфхаки по эксплуатации, обзоры технологий, советы по выбору запчастей и обслуживанию автомобиля.

Информационный автомобильный https://avtonews.kyiv.ua портал с ежедневными публикациями о новых автомобилях, технологиях, электрокарах, автоспорте, правилах дорожного движения, ремонте, диагностике, тюнинге и полезных советах для автовладельцев.

Все самое интересное https://black-star.com.ua из мира автомобилей: свежие новости, обзоры новинок, тест-драйвы, рекомендации по выбору машины, обслуживанию, экономии топлива, уходу за кузовом и подготовке автомобиля к разным сезонам.

Узнавайте первыми https://setbook.com.ua о новинках автомобильного рынка. Новости производителей, тесты автомобилей, сравнение комплектаций, советы по покупке, ремонту, страхованию, обслуживанию и безопасной эксплуатации транспорта.

Автомобильный портал https://troeshka.com.ua с ежедневными публикациями о новых моделях, электромобилях, гибридах, внедорожниках, кроссоверах, технологиях, автоспорте, ремонте, тюнинге и полезными рекомендациями для водителей.

Автомобильный портал https://proauto.kyiv.ua с актуальными статьями, аналитикой и обзорами. Узнавайте о новых моделях, изменениях на авторынке, современных технологиях, сервисном обслуживании, ремонте, эксплуатации и выборе автомобиля.

Мир автомобилей https://road.kyiv.ua без лишней информации: свежие новости, обзоры популярных моделей, тест-драйвы, советы по эксплуатации, ремонту, обслуживанию, выбору запчастей и актуальные материалы для каждого автовладельца.

взять займ онлайн https://zaym-ili-kredit.ru

взять микрозаем займ на карту взять

Последние публикации: https://mamamia-shop.ru/magazin/tag/dlya-beremennyh/

Smith Jonsi’s articles https://vocal.media/authors/smit-jonsy on Vocal cover modern AI applications and digital technologies. Independent reviews and honest comparisons of features, capabilities, pricing, voice quality, privacy, and user experience.

Новое в категории: https://chayblog.ru/category/whitetea/

SEO продвижение под ключ для малого бизнеса — реально ли это при ограниченном бюджете?

Самые важные новости https://tvk-avto.com.ua автомобильной отрасли, обзоры автомобилей, рейтинги, тест-драйвы, экспертные статьи, советы по обслуживанию, выбору шин, аккумуляторов, масел, аксессуаров и уходу за автомобилем.

Узнайте больше https://poradnik.com.ua о строительстве и ремонте: полезные статьи, экспертные рекомендации, обзоры строительных материалов, современные технологии, инженерные решения, советы по отделке и эксплуатации частных домов.

Строительный портал https://vasha-opora.com.ua для тех, кто строит, ремонтирует и благоустраивает. Новости рынка, обзоры строительных материалов, пошаговые инструкции, рекомендации специалистов, идеи для дома, квартиры и загородного участка.

Откройте мир полезных https://beautyadvice.kyiv.ua советов для женщин: уход за лицом и телом, стиль, мода, здоровье, психология, рецепты, воспитание детей, финансы, саморазвитие и вдохновение для счастливой жизни.

Познавательный портал https://detiwki.com.ua для детей с интересными статьями, развивающими заданиями, научными фактами, играми, головоломками, творческими идеями, опытами, рассказами о природе, космосе, животных, истории и окружающем мире.

Женский информационный https://gratransymas.com портал с полезными материалами о моде, уходе за собой, психологии, семейной жизни, здоровье, кулинарии, хобби, карьере, отдыхе и личностном развитии.

Современный портал https://horoscope-web.com для женщин с интересными статьями, экспертными советами и обзорами. Узнавайте больше о красоте, здоровье, моде, отношениях, материнстве, уюте, саморазвитии и вдохновляющих историях.

Актуальные статьи https://godwood.com.ua для женщин о красоте, здоровье, отношениях, беременности, воспитании детей, моде, косметике, фитнесе, правильном питании, путешествиях и современных лайфхаках.

Откройте для себя https://icz.com.ua мир красоты, здоровья и вдохновения. Читайте полезные статьи о моде, уходе за собой, психологии, отношениях, семье, правильном питании, путешествиях и гармоничной жизни современной женщины.

Все самое интересное https://ramledlightings.com для женщин в одном месте. Советы по уходу за собой, обзоры косметики, секреты красоты, идеи стильных образов, рекомендации по здоровью, отношениям и воспитанию детей.

Ежедневно публикуем https://presslook.com.ua полезные статьи для женщин о здоровье, красоте, моде, психологии, любви, семье, кулинарии, саморазвитии, путешествиях, финансах и современных тенденциях образа жизни.

Женский онлайн-журнал https://lolitaquieretemucho.com с интересными материалами о красоте, здоровье, стиле, модных тенденциях, косметике, фитнесе, воспитании детей, домашнем уюте, карьере и личностном развитии.

Детский центр https://run.org.ua развития и здоровья с комплексными программами для детей разных возрастов. Развивающие занятия, логопед, психолог, подготовка к школе, творческие кружки, физическое развитие, диагностика и индивидуальный подход к каждому ребенку.

лента жаростойкая стальная лента гост

лента 12х18н10т лента стальная санкт-петербург

Top title checker check for salvage title follows the VIN even after a title has been washed.

прайс лист лента стальная лента стальная с доставкой

На сайті https://rest.od.ua ви знайдете багато корисної інформації для кожного одесита: театральна афіша Одеси, карта та схема проїзду до всіх театрів та концертних майданчиків міста

Нужен аккмулятор? аккумуляторы по выгодной цене с подбором под ваш автомобиль. В наличии аккумуляторы популярных брендов, услуги установки, диагностика аккумулятора, прием старой АКБ и оперативная доставка по Санкт-Петербургу.