- The US crude oil inventories fell for a sixth straight week last week, according to American Petroleum Institute data released on 27th May'26. Crude stocks decreased by 2.8 mln bbl, while gasoline inventories fell by 3.2 mln bbl and distillate inventories rose by 1.1 mln bbl compared to the previous week.

- On 27th May'26, the US military shot down four Iranian attack drones and struck a ground control station in Bandar Abbas, following an Iranian drone operation posing a threat to US forces and commercial shipping in the Strait of Hormuz.

- A cargo of US Strategic Petroleum Reserve oil headed to California for the first time ever, highlighting the redrawing of trade flows and shipping routes due to the Iran war. California, once a top oil-producing state, has become more dependent on crude imports, including from the Middle East.

- About 0.46 bbl of Bayou Choctaw Sweet crude went to Chevron's Richmond refinery and another 0.05 bbl to its El Segundo refinery, while a supertanker unloaded the cargo to two smaller ships that took it to the refineries in California.

- According to PPAC data, Indian refiners' crude throughput fell 8.9% month-on-month in April to 5.23 MBpd, Indian Oil Corp, Bharat Petroleum Corp Ltd, Hindustan Petroleum Corp Ltd, Mangalore Refinery and Petrochemicals Ltd, and Reliance Industries Ltd all experienced drops in production.

- CPCL's CBR refinery is decommissioned due to limitations in meeting product specifications with the existing configuration. .

- Iran accused the US of violating a ceasefire by striking targets near the Strait of Hormuz, complicating efforts to end the war. Israel continued to bomb Lebanon, further straining peace efforts.

- The war has caused an unprecedented oil supply shock, pushing up the costs of fuel, fertiliser, and food. Iran and the US have made progress on a memorandum of understanding that would lead to further negotiations over a final agreement, but key issues remain unresolved, including Iran's nuclear program and the conflict in Lebanon.

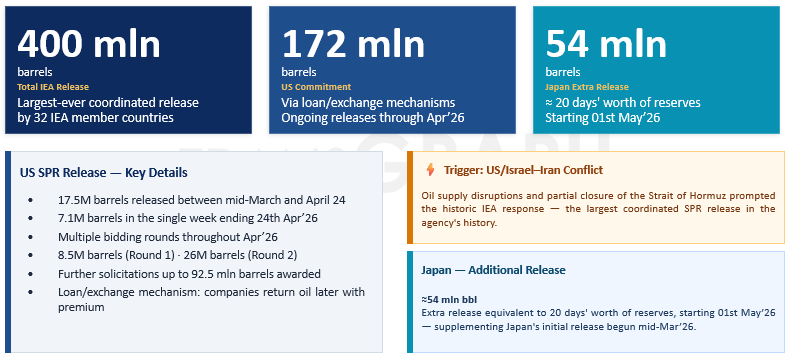

- A cargo of crude oil from the US Strategic Petroleum Reserve is heading to the Philippines, the first shipment to Asia since Nov'22. The shipment is part of a coordinated effort by the International Energy Agency to release 400 mln bbl of oil to quell rising prices, as the Iran war upends global supplies and the Strait of Hormuz remains largely closed.

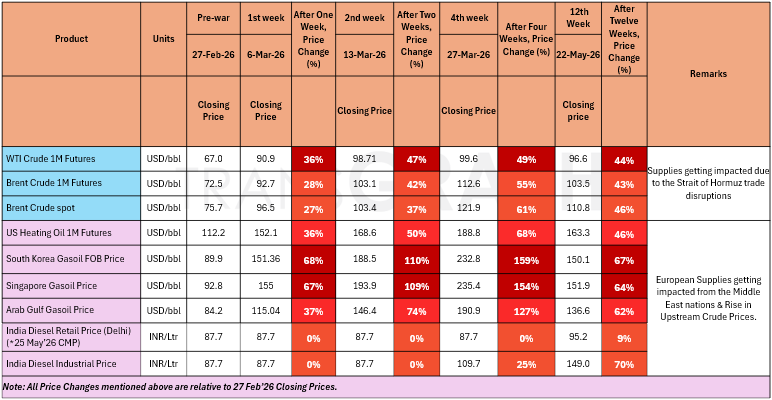

War Impact on Crude Oil & Gasoil/Diesel Prices

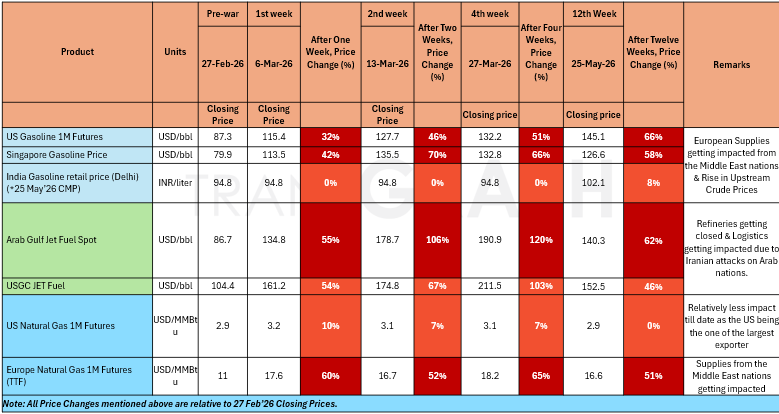

War Impact on Gasoline, ATF & Natural Gas Prices

GCC Bypass Pipelines Running Near Capacity — But Shah Gas Field Ablaze and Fujairah Zone Struck

- Saudi Arabia's East-West pipeline is pumping oil at its full capacity of 7 MBpd, bypassing the Strait of Hormuz. Crude oil exports from Yanbu port have reached 5 MBpd, and the country is also exporting 0.70 to 0.90 MBpd of oil products.

- Of approximately 15 MBpd of crude transiting the Strait of Hormuz in OND'25, combined SPR releases and bypass pipeline capacity can offset roughly two-thirds — or slightly more — for the next 20 to 30 days, providing the Trump administration a window to assess strategic direction.

- New strikes directly threaten this buffer — Iranian drones struck the UAE's Shah gas field (currently ablaze) and the Fujairah Oil Industry Zone on Mar 17. A tanker was also hit near the Strait of Hormuz. Saudi Arabia intercepted over a dozen drones; Kuwait and Bahrain sustained additional attacks. These represent the first direct strikes on GCC energy export infrastructure since the conflict began.

Supply & Demand Analysis

War Scenarios Point to Global Supply Deficit of 1.35–1.90 MBpd in 2026 and AMJ Quarter Most Severe with a deficit of 3.00 - 4.50 MBpd.

Pre-war, global supply and demand were near-balanced with a modest surplus of +0.55 MBpd projected for 2026. Both conflict scenarios introduce significant supply deficits driven by Strait of Hormuz disruptions and impacts on Iraq and Kuwait crude production.

- Scenario 1 (Preferred): Ceasefire talks to remain on a progressive note and flows through the Strait of Hormuz improving over the coming weeks; however crude oil production losses will be there due to further non-availability of storage on on-shore in Iraq, Kuwait and other small Middle East nations.

- Scenario 2 (Alternate): No major deal being achieved from ceasefire talks and post completion of ceasefire talks, tensions continuing to remain in the Middle East and flows through the Strait of Hormuz continuing to remain restrained. Crude Oil Production Facilities & Refining Centers in the Middle East region getting affected and trade disruptions in Strait of Hormuz will be there for medium to long term (4 to 7 months).

Brent Crude 1M Futures are expected to trade in a range of 100 USD/bbl to 125 USD/bbl over the coming 1 to 2 weeks. The coordinated SPR release and GCC bypass capacity provide a meaningful supply cushion that limits sustained upside beyond these levels.

Metals & Energy Market Update – Geopolitical Context (Iran Conflict)

Geopolitical backdrop:

The ongoing conflict in the Middle East, continues to weigh on global markets and keeping inflation expectations elevated as crude oil prices remained above USD 100/Barrel amid persistent supply disruption concerns. The war-driven rise in energy prices has heightened concerns about higher transportation and manufacturing costs globally, adding further pressure to already elevated inflation. At the same time, elevated crude prices continue to weigh on emerging markets and developing economies, particularly large energy-importing nations, as higher import bills and currency pressures weaken economic stability and complicate monetary policy decisions in the near term.

Steel:

- Domestic steel prices have moderated from recent highs.

- Steel supply chains remain largely insulated from the Middle East conflict.

- Since, the start of war steel HRC prices are up by 9.0%.

Base metals:

- Copper ended last week up by 1.1%, primarily due to widening CME-LME spread.

- Aluminum rose by 19% since start of war linked to Gulf region supply disruptions. However, demand softness now driving price action.

- IMF downgraded 2026 global growth to 3.1% (from 3.3% earlier and 3.4% in 2025), highlighting war-related downside risks.

Precious metals:

- Volatility has eased, but prices face upward pressure, due to improving market sentiment in peace talks.

- However, any esclation and halt in a resolution will pressure on Precious Metals.

- Stronger U.S. yields and weak industrial offtake—especially auto—are suppressing any upside momentum.

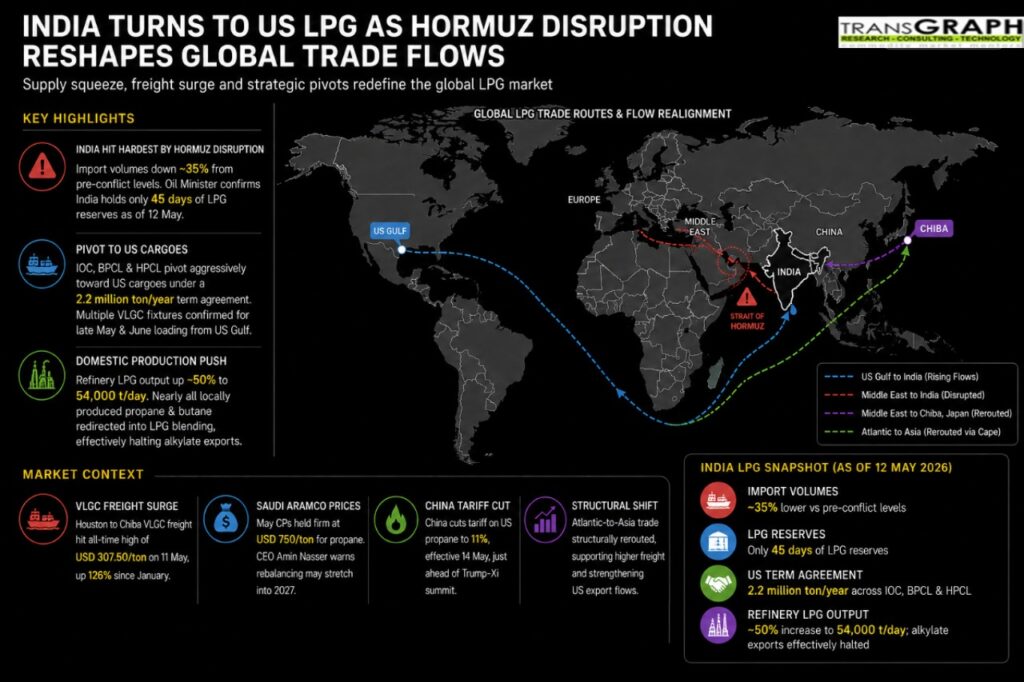

LPG Market Update - 26 May 2026

- Saudi Aramco increased its June 2026 CPs to USD 760/ton for propane and USD 820/ton for butane, compared to USD 750/ton and USD 800/ton in May, showing that the global LPG market remains tight. The rise mainly reflects ongoing geopolitical tensions in the Gulf, with disruptions around Hormuz and Saudi export infrastructure continuing to keep supply concerns elevated. Butane prices saw stronger support from steady Asian petrochemical demand and better gasoline blending margins. Even with softer crude prices, the latest CPs suggest that supply security remains the key factor driving LPG prices.

- On 25 May 2026, the Government of India introduced an amendment to LPG supply regulations that makes the shift from LPG to PNG more flexible for consumers. Households taking a PNG connection can either surrender their LPG connection within 30 days or retain future eligibility through a transfer voucher if they later move to a non PNG area.